Car

tax Transport tax on a car is calculated using a standard formula. The amount of horsepower (hp or kW) indicated in the car's title is multiplied by the current tax rate in the region of registration of the vehicle. The resulting number is multiplied by a coefficient calculated as the ratio of the number of complete months of car ownership to the number “12”.

Example. Let's say you own a Lada Vesta vehicle, the engine power is 82 horsepower and you live in the Central region - Moscow. The transport tax rate in 2019 (indicated in the table below) is 12 rubles. When calculating the transport tax on a car for 1 year it will be: 12 rubles x 82 horsepower = 984 rubles.

If the PTS does not indicate the horsepower of the car, then the power in kW must be indicated. This requires converting kilowatts of car power into horsepower. Don’t be alarmed, the conversion is very simple: 1 kW = 1.35962 hp. The resulting amount of vehicle transport tax is rounded to the nearest hundredth.

Transport tax rate for cars in Moscow for 2020

| Name of taxable object | Rate (RUB) |

| Passenger cars with engine power (transport tax is calculated for each horsepower of the vehicle): | |

| up to 100 l. With. (up to 73.55 kW) inclusive | 12 |

| over 100 hp up to 125 hp (over 73.55 kW to 91.94 kW) inclusive | 25 |

| over 125 hp up to 150 hp (over 91.94 kW to 110.33 kW) inclusive | 35 |

| over 150 hp up to 175 hp (over 110.33 kW to 128.7 kW) inclusive | 45 |

| over 175 hp up to 200 hp (over 128.7 kW to 147.1 kW) inclusive | 50 |

| over 200 hp up to 225 hp (over 147.1 kW to 165.5 kW) inclusive | 65 |

| over 225 hp up to 250 hp (over 165.5 kW to 183.9 kW) inclusive | 75 |

| over 250 hp (over 183.9 kW) | 150 |

| Motorcycles and scooters with engine power (transport tax is calculated for each horsepower): | |

| up to 20 l. With. (up to 14.7 kW) inclusive | 7 |

| over 20 l. With. up to 35 l. With. (over 14.7 kW to 25.74 kW) inclusive | 15 |

| over 35 l. With. (over 25.74 kW) | 50 |

| Buses with engine power (per horsepower): | |

| up to 110 hp (up to 80.9 kW) inclusive | 15 |

| over 110 hp up to 200 hp (over 80.9 kW to 147.1 kW) inclusive | 26 |

| over 200 l. With. (over 147.1 kW) | 55 |

| Trucks with engine power (per horsepower): | |

| up to 100 l. With. (up to 73.55 kW) inclusive | 15 |

| over 100 l. With. up to 150 l. With. (over 73.55 kW to 110.33 kW) inclusive | 26 |

| over 150 l. With. up to 200 l. With. (over 110.33 kW to 147.1 kW) inclusive | 38 |

| over 200 l. With. up to 250 l. With. (over 147.1 kW to 183.9 kW) inclusive | 55 |

| over 250 l. With. (over 183.9 kW) | 70 |

| Other self-propelled vehicles, pneumatic and tracked machines and mechanisms (per horsepower) | 25 |

| Snowmobiles, motor sleighs with engine power (per horsepower): | |

| up to 50 l. With. (up to 36.77 kW) inclusive | 25 |

| over 50 l. With. (over 36.77 kW) | 50 |

| Boats, motor boats and other water vehicles with engine power (per horsepower): | |

| up to 100 l. With. (up to 73.55 kW) inclusive | 100 |

| over 100 l. With. (over 73.55 kW) | 200 |

| Yachts and other sailing-motor vessels with engine power (per horsepower): | |

| up to 100 l. With. (up to 73.55 kW) inclusive | 200 |

| over 100 l. With. (over 73.55 kW) | 400 |

| Jet skis with engine power (per horsepower): | |

| up to 100 l. With. (up to 73.55 kW) inclusive | 250 |

| over 100 l. With. (over 73.55 kW) | 500 |

| Non-self-propelled (towed) vessels for which gross tonnage is determined (transport tax is calculated for each registered ton of gross tonnage) | 200 |

| Airplanes, helicopters and other aircraft with engines (per horsepower) | 250 |

| Airplanes with jet engines (per kilogram of thrust) | 200 |

| Other water and air vehicles without engines (per vehicle unit) | 2000 |

Transport tax calculator for a 250 hp car in the Kaluga region

Transport tax is calculated on the basis of: Tax base established depending on the type of vehicle; Tax rate; Taxpayer's shares in property rights; The period for which the tax is calculated; Increasing factor (luxury tax).

Based on these components, the tax is calculated and a notification is sent to the vehicle owner at least 30 days before the payment is due.

The tax is not paid in the following cases: 1. Passenger cars specially equipped for use by disabled people, as well as cars with an engine power of up to 100 horsepower (up to 73.55 kilowatts), received (purchased) through social security authorities;

2. Tractors, self-propelled combines of all brands, special vehicles (milk tankers, livestock trucks, special vehicles for transporting poultry, machines for transporting and applying mineral fertilizers, veterinary care, maintenance), registered to agricultural producers and used in agricultural work;

3. Vehicles that are wanted, subject to confirmation of the fact of their theft (theft) by a document issued by the authorized body;

4. Vehicles owned by the right of operational management to federal executive authorities and federal state bodies in which the legislation of the Russian Federation provides for military and (or) equivalent service;

5. Passenger and cargo sea, river and aircraft owned (by the right of economic management or operational management) of organizations and individual entrepreneurs whose main activity is passenger and (or) cargo transportation;

6. Rowing boats, as well as motor boats with an engine power of no more than 5 horsepower;

7. Offshore fixed and floating platforms, offshore mobile drilling rigs and drilling ships.

8. Air ambulance and medical service airplanes and helicopters;

9. Vessels registered in the Russian International Register of Ships;

10. Fishing sea and river vessels.

Transport tax is a regional tax

, which is regulated by Chapter 28 of the Tax Code of the Russian Federation. The Tax Code of the Russian Federation spells out the basic rules governing the object of taxation, tax payers, calculation and payment rules.

That is, the basic conditions are prescribed at the federal level, but regional authorities have the right to make their own adjustments. Important: regional authorities cannot worsen the rights of taxpayers. In addition, regions set tax rates and preferential categories of payers.

Object

taxation are:

- cars;

- motorcycles;

- self-propelled machines and vehicles on pneumatic and caterpillar tracks;

- snowmobiles and motor sleighs;

- air transport (planes and helicopters);

- marine vehicles (motor ships, boats, yachts and jet skis).

But there are exceptions

, which include:

- passenger cars with engine power up to 100 horsepower (purchased through the social security department);

- cars equipped for disabled people;

- tractors, self-propelled combines and special vehicles for transporting milk, poultry, which are used for agriculture (for individual entrepreneurs);

- fishing vessels (for individual entrepreneurs).

Tax is not calculated for these vehicles

.

Transport tax rates are set by regional authorities

. However, Article 361 of the Tax Code of the Russian Federation indicates approximate values of transport tax, which regions have the right to reduce or increase by no more than 10 times, with the exception of cars with an engine power of up to 150 hp.

The main criterion for determining the tax rate is engine power. In addition, regional authorities have the right to set additional tax rates depending on the environmental class of the vehicle and the number of years of use.

Benefits provided for payment of transport tax

Adhering to the rules of regional laws, the following are exempt from paying transport tax:

- Veterans and disabled people of the Great Patriotic War, Heroes of the Soviet Union, Heroes of Russia and other groups of taxpayers.

- For Moscow - representatives (one of two parents) of large families.

- For St. Petersburg - only one of the parents of a family with at least four minor children.

- A certain number of citizens are provided with a transport tax benefit, provided that their vehicle is domestically produced and has an engine with a capacity of up to 150 hp.

| Category of taxpayers for whom the benefit is established | The corresponding article (clause) of the law of the subject of the Russian Federation | Grounds for granting benefits | Size | Unit change | Conditions for providing benefits | FL, LE, IP |

| organizations providing services for the transportation of passengers by public urban passenger transport | subparagraph 1 of paragraph 1 of article 4 | provisions of the constituent documents (charter, regulations) defining passenger transportation as the main type of activity, the purpose of creating the organization; availability of a valid license for passenger transportation | 100 | % | Calculation of transport tax on vehicles transporting passengers by public urban passenger transport (except taxis) (subclause 1 of clause 1, article 4). Vehicles exempt from taxation include vehicles that use uniform conditions for the transportation of passengers at uniform fares established by the executive authorities of the city of Moscow. Calculate transport tax taking into account the provision of all travel benefits approved in the prescribed manner; benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | Legal entity |

| residents of the special economic zone of technology-innovation type "Zelenograd" | subparagraph 2 of paragraph 1 of article 4 | extract from the register of residents of the special economic zone, issued by the management body of the special economic zone | 100 | % | for vehicles registered to residents from the moment they were included in the register of residents of the special economic zone. The benefit is provided for a period of five years, starting from the month of registration of the vehicle (subparagraph 2 of paragraph 1 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | Legal entity |

| Heroes of the Soviet Union, Heroes of the Russian Federation, citizens awarded the Order of Glory of three degrees, | subparagraph 3 of paragraph 1 of article 4 | statement; Hero's book or order book | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 3 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4), benefits do not apply to water and air vehicles , snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| veterans of the Great Patriotic War, disabled people of the Great Patriotic War; | subparagraph 4 of paragraph 1 of article 4 | statement; standard certificate | 100 | % | Calculation of transport tax for one vehicle with an engine power of up to 200 hp. (inclusive) (subclause 4 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| combat veterans, disabled combat veterans | subparagraph 5 of paragraph 1 of article 4 | statement; certificate or certificate of entitlement to benefits of the established form | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 5 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| disabled people of groups I and II | subparagraph 6 of paragraph 1 of article 4 | statement; a certificate from a medical institution of the established form confirming the fact that disability group I or II has been established. | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 6 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| former minor prisoners of concentration camps, ghettos, and other places of forced detention created by the Nazis and their allies during the Second World War | subparagraph 7 of paragraph 1 of article 4 | statement; certificate of entitlement to benefits in the established form | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 7 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| one of the parents (adoptive parents), guardian, trustee of a disabled child | subparagraph 8 of paragraph 1 of article 4 | statement; passport of a citizen of the Russian Federation issued in the name of the taxpayer; birth certificate of the child specified in the application; a copy of the act (extract from the act) of the guardianship and trusteeship authorities on the establishment of guardianship (trusteeship) over the child; a certificate of the established form confirming the fact that this child has been assigned the category of disability “disabled child”; information about the second parent (adoptive parent), guardian, trustee (full name and address of residence) | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subparagraph 8 of paragraph 1 of Article 4, paragraph 5 of Article 4) and only one of the parents (adoptive parents), guardian, trustee of a disabled child (subparagraph 8 of paragraph 1 of Article 4), if there is a right to receive benefits on several grounds, benefit provided on one basis at the taxpayer’s choice (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of Article 4); | FL IP |

| calculate transport tax for a person who owns passenger cars with an engine power of up to 70 horsepower (up to 51.49 kW) inclusive | subparagraph 9 of paragraph 1 of article 4 | statement; copy of vehicle passport | 100 | % | for one vehicle (subclause 9 of clause 1 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL LE IP |

| one of the parents (adoptive parents) in a large family | subparagraph 10 of paragraph 1 of article 4 | statement; certificate of a large family of the city of Moscow; information about the second parent (adoptive parent) (full name and address of residence) | 100 | % | one vehicle and only one of the parents (adoptive parents) (subclause 10 of clause 1 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| individuals entitled to receive social support in accordance with the Law of the Russian Federation of May 15, 1991 N 1244-1 “On the social protection of citizens exposed to radiation as a result of the disaster at the Chernobyl nuclear power plant”, Federal laws of November 26, 1998 N 175- Federal Law “On social protection of citizens of the Russian Federation exposed to radiation as a result of the accident in 1957 at the Mayak production association and the discharge of radioactive waste into the Techa River” and dated January 10, 2002 N 2-FZ “On social guarantees to citizens exposed to radiation due to nuclear tests at the Semipalatinsk test site" | subparagraph 11 of paragraph 1 of article 4 | statement; standard certificate | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 11 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| individuals who, as part of special risk units, took direct part in testing nuclear and thermonuclear weapons, eliminating accidents of nuclear installations at weapons and military facilities | subparagraph 12 of paragraph 1 of article 4 | statement; standard certificate | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 12 of clause 1 of Article 4, clause 5 of Article 4), calculate the transport tax if there is a right to receive benefits on several grounds; the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| individuals who received or suffered radiation sickness or became disabled as a result of tests, exercises and other work related to any types of nuclear installations, including nuclear weapons and space technology | subparagraph 13 of paragraph 1 of article 4 | statement; standard certificate | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 13 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

| one of the guardians of a disabled person since childhood, recognized by the court as incompetent for one vehicle registered to citizens of the specified categories | subparagraph 14 of paragraph 1 of article 4 | statement; standard certificate | 100 | % | one vehicle each with an engine power of up to 200 hp. (inclusive) (subclause 14 of clause 1 of Article 4, clause 5 of Article 4), if there is a right to receive benefits on several grounds, the benefit is provided on one basis at the choice of the taxpayer (clause 2 of Article 4); benefits do not apply to water, air vehicles, snowmobiles and motor sleighs (clause 3 of article 4) | FL IP |

About transport tax benefits

In accordance with Article 3 of the Law of the Republic of Bashkortostan dated November 27, 2002 No. 365 -z “On Transport Tax”, disabled people of all categories and veterans of the Great Patriotic War are exempt from paying transport tax by choice for one vehicle of each type if two or more vehicles are registered. , veterans of combat operations on the territory of the USSR, on the territory of the Russian Federation and the territories of other states, veterans of military service, veterans of labor, categories of citizens exposed to radiation as a result of the Chernobyl disaster, for motorcycles, scooters and passenger cars with engine power up to 150 horsepower inclusive , as well as for trucks, from the date of production of which more than 10 years have passed, with an engine power of up to 250 horsepower inclusive, for other self-propelled vehicles, pneumatic and tracked machines and mechanisms (registered with the State Inspectorate for Supervision of the Technical Condition of Self-propelled Vehicles and other types of equipment of the Republic of Bashkortostan), from the date of release of which more than 10 years have passed.

In addition, the Law of the Republic of Bashkortostan dated December 24, 2018 No. 27-z “On Amendments to the Law of the Republic of Bashkortostan “On Transport Tax”” (hereinafter referred to as Law No. 27-z), which came into force after one month from the date of official publication , are exempt from paying transport tax:

- one of the parents (adoptive parent) or guardian (trustee) in a family that is recognized as having many children in accordance with the Law of the Republic of Bashkortostan dated July 24, 2000 No. 87-z “On state support for large families in the Republic of Bashkortostan”, for passenger cars with engine power up to 150 horsepower inclusive, as well as for buses with engine power up to 125 horsepower inclusive - optionally for one vehicle of each type;

- one of the parents (adoptive parent) or guardian (trustee) of a disabled child for passenger cars with an engine power of up to 150 horsepower inclusive (for owners of two or more vehicles - optionally for one vehicle).

The benefits established by Law No. 27-z are valid until December 31, 2024 and apply to legal relations that arose from January 1, 2021.

Thus, taxpayers - individuals belonging to the above categories of taxpayers, have at the same time the right to receive transport tax benefits on each basis .

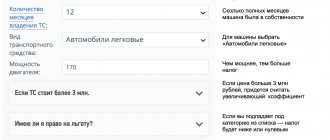

Luxury car transport tax in 2021

Formula for calculating transport tax on a car whose cost exceeds 3 million rubles. and owning the car for more than 1 year:

Transport tax amount = (Tax rate) x (L. s) x (Increasing coefficient)

Calculation of tax on a car, the cost of which is more than 3 million rubles. and if you own it for less than 1 year:

Transport tax amount = (Tax rate) x (L. s) x (Number of months of ownership / 12) x (Increasing factor)

Calculation of the transport tax increasing coefficient (Article 362 of the Tax Code of the Russian Federation)

The increasing coefficient according to Article 362 of the Tax Code of the Russian Federation, Chapter 28:

- 1,1 - for passenger cars worth from 3 million to 5 million rubles inclusive, from the year of manufacture of which 2 to 3 years have passed;

- 1,3 - for passenger cars worth from 3 million to 5 million rubles inclusive, from the year of manufacture of which 1 to 2 years have passed;

- 1,5 - for passenger cars worth from 3 million to 5 million rubles inclusive, no more than 1 year has passed since the year of manufacture;

- 2 - for passenger cars worth from 5 million to 10 million rubles inclusive, no more than 5 years have passed since the year of manufacture;

- 3 - in relation to passenger cars worth from 10 million to 15 million rubles inclusive, no more than 10 years have passed since the year of manufacture;

- 3 - for passenger cars costing over 15 million rubles, no more than 20 years have passed since the year of manufacture.

Deadlines for paying transport tax on a car

Transport tax on a car is paid at the place of registration of the car, and in the absence of such, at the place of residence of the owner of the vehicle.

Individuals pay transport tax on cars no later than December 1 of each year (Article 363 of the Tax Code of the Russian Federation), based on a tax notice received from the Federal Tax Service along with a payment receipt. If the transport tax is not paid within the required period, a penalty is charged, and the tax amount increases by a certain percentage monthly.

Calculation of transport tax for legal entities

Legal entities are required to calculate the transport tax for each car independently and make quarterly advance payments (payments of 1/4 to the Federal Tax Service of the total amount of all vehicles of the department). If the organization owns an expensive car included in the special. list of the Ministry of Industry and Trade of the Russian Federation, then advance payments by a legal entity are paid immediately taking into account the established increasing coefficient (coefficient for a luxury car).

At the end of the calendar year, the remaining tax must be paid by February 1 of the year following the reporting year. The calculated transport tax must be paid within the deadlines established by law for submitting tax returns.

Transport tax calculator

Transport tax benefits are established by regional regulations. In most cases, the following are exempt from paying transport tax:

- disabled people of groups I and II;

- WWII veterans;

- Heroes of the Soviet Union, Heroes of the Russian Federation, Russians awarded the Order of Glory of three degrees;

- combat veterans;

- one of the parents of a disabled child.

Some regions provide benefits

and other categories of people:

- one of the parents of a large family;

- Chernobyl victims;

- people who participated in the liquidation of nuclear accidents or in testing nuclear weapons.

However, each region has its own preferential categories of taxpayers

. More detailed information about all the benefits provided can be found at the local Federal Tax Service inspectorate.

It is worth noting that benefits for the above categories of people are provided only for 1 car, which is chosen by the payer himself. To provide a benefit, you must write to the Federal Tax Service an application about the selected preferential object of taxation and attach a document confirming the benefit.

If the beneficiary belongs to several categories

payers who are exempt from transport tax, he has the right to take advantage of only one benefit in relation to one vehicle.

Some regions establish criteria not only for the tax payer, but also for the vehicle

. For example, in Moscow, a transport tax benefit can only be issued for a car with an engine power of no more than 200 horsepower. The only exception is a car that belongs to one of the parents of a large family (but there are no restrictions on the power of the car).

Legal entities, in accordance with the requirements of Art. 4 of this law, are required to make advance payments during the year based on the results of each quarter, calculated as 25% of the total estimated tax amount for the year. These funds must be transferred within one month and five days after the end of the reporting period.

The organization must transfer the last payment to the accounts of the tax authority no later than March 1.

To calculate a legal entity, a formula with three multipliers is used: the holding period (the number of months divided by 12), the rate accepted in the region and the tax base.

Deadline for payment of transport tax for legal entities in 2021:

- for 2021 - no later than March 1, 2020

- for the 1st quarter of 2021 - no later than May 5, 2020

- for the 2nd quarter of 2021 (6 months) - no later than August 5, 2021

- for the 3rd quarter of 2021 (9 months) - no later than November 5, 2021

- for the 4th quarter and the whole of 2021 - no later than March 1, 2021

The following organizations have the right to apply for a reduction in the tax rate (subject to the provision of supporting documents):

- authorities and local self-government;

- religious organizations;

- SEZ residents;

- owners of vehicles classified as general aviation;

- Legal entities and individual entrepreneurs operating trucks, buses, tracked vehicles, provided that the vehicle is equipped with gas equipment.

Technical means on which it is necessary to pay transport tax can be divided into several categories, and the form of ownership does not matter:

- Land self-propelled vehicles (cars and trucks, agricultural and construction equipment, motorcycles and ATVs).

- River and sea transport (motor boats, yachts, cutters, motor ships, barges and floating docks).

- Air transport (helicopters, airplanes, drones weighing more than 30 kg).

Trailers for cars and agricultural machinery are not subject to tax.

Legal entities also have benefits for paying transport tax; for example, in Moscow, companies engaged in transporting passengers in the city are exempt from it. The zero rate also applies to agents of special economic zones.

In addition, the category of beneficiaries includes:

- Companies that own commercial and fishing vessels or water transport, the main activity of which is cargo and passenger transportation.

- Entrepreneurs working in agriculture (the share of sales of agricultural products must exceed 50% of the company's total revenue) are also exempt from tax on combines, tractors, vehicles for transporting fertilizers and finished products.

- Vehicles and equipment of military and law enforcement agencies (MoD, Civil Defense, FSB, Ministry of Emergency Situations, Foreign Intelligence Service).

- Medical planes and helicopters, with the image of the Red Cross or Crescent on board.

A car that is wanted after being stolen is also exempt from paying transport tax; for this, a supporting document from the police must be submitted to the fiscal authorities.

If an organization falls under the above categories of beneficiaries, it is obliged to notify the tax authorities about this. Accrual of a zero rate is possible only after submitting the appropriate form to the Federal Tax Service. This is due to the fact that previously this information was reflected in tax returns, which is no longer needed for transport tax. Individuals and individual entrepreneurs do not have to submit information; tax officials will do this for them.

To pay the tax and sleep peacefully, the car owner can use two methods:

- Wait for a postal notification from the tax office, where the data on the vehicle will be entered and the tax amount will be indicated.

- Register on the website of the Federal Tax Service and receive information about taxes through your personal account. You can pay the tax immediately using a credit card from any bank.

The deadline for payment of transport tax for last year expires on December 1 of the current year , after this date the fiscal authorities have the right to apply penalties to the defaulter.

Until 2021, regions themselves set the deadline for payment of transport tax for enterprises and organizations, but not earlier than February 1 of the year following the reporting period. In 2021, the situation will change - legal entities across the country will pay for transport until March 1 next year.

This law will not apply to individual entrepreneurs; for this category, everything will remain the same - the TN must be paid before December 1, just like individuals, based on a notification received by mail.

As for enterprises making advance payments for transport tax, the federal center decided to streamline everything here too - now, according to rules common to the whole country, the advance payment will be made before the end of the month following the reporting period.

The Tax Service did not remain aloof from events related to quarantine restrictions during the coronavirus pandemic. The most affected enterprises and small businesses during this period, included in the register no later than 2021, will not have to pay transport tax for the second quarter of 2021 at all, and younger companies in the affected sectors of the economy were given a deferment for the advance payment for the first quarter until the end October 2020.

Taxes, including transport taxes, must be paid. This is the responsibility of all citizens and organizations of the country. Current information on changes in legislation can always be found on the official website of the tax service. There you will also find information about regional rates, on the basis of which you can make the final calculation of the transport tax.

- for cars

- for motorcycles

- for buses

- for truck

- for snowmobiles

- for boats

- for yachts

- for jet skis

- for aircraft

- for jet aircraft

The table shows transport tax rates in the Kaluga region.

| from 20 to 35 hp inclusive | 10 |

| more than 35 hp | 50 |

| Snowmobiles, motor sleighs with engine power (per horsepower): | |

| up to 50 hp inclusive | 25 |

| more than 50 hp | 50 |

| Passenger cars with engine power (per horsepower): | |

| up to 100 hp inclusive | 25 |

| from 100 to 150 hp inclusive | 35 |

| from 150 to 200 hp inclusive | 50 |

| from 200 to 250 hp inclusive | 75 |

| more than 250 hp | 150 |

| Jet skis with engine power (per horsepower): | |

| up to 100 hp inclusive | 125 |

| more than 100 hp | 250 |

| Yachts and other sailing-motor vessels with engine power (per horsepower): | |

| up to 100 hp inclusive | 100 |

| more than 100 hp | 200 |

| Boats, motor boats and other water vehicles with engine power (per horsepower): | |

| up to 100 hp inclusive | 30 |

| more than 100 hp | 100 |

| Trucks with engine power (per horsepower): | |

| up to 100 hp inclusive | 25 |

| from 100 to 150 hp inclusive | 40 |

| from 150 to 200 hp inclusive | 50 |

| from 200 to 250 hp inclusive | 65 |

| more than 250 hp | 85 |

| Buses with engine power (per horsepower): | |

| up to 200 hp inclusive | 30 |

| more than 200 hp | 92 |

| more than 0 hp | 15 |

| Airplanes, helicopters and other aircraft with engines (per horsepower) 10 | |

| more than 0 hp | 125 |

| Airplanes with jet engines (per kilogram of thrust) | |

| more than 0 hp | 100 |

Payment deadline (for 2021) for organizations: Upon expiration of the tax period, the tax is paid no later than 03/01/2021. Payment of advance payments at the end of each reporting period is made no later than the 5th day of the second month following the reporting tax period.

Transport tax (TN) is a tax designed to compensate for the harmful effects of vehicles on road surfaces and the environment. It is regulated both by Chapter 28 of the Tax Code of the Russian Federation (for federal calculations) and by legislative acts adopted in each individual region (for regional calculations). Legislative acts adopted by regions affect the tax rate, the procedure and terms of payment, and so on.

It is also worth noting that if the owner of the vehicle did not own it for a full year after purchase or sale, then the transport tax rate also includes a special coefficient of vehicle ownership, equal to the ratio of the number of months of ownership to 12 months. Let's give an example. If the owner owned the vehicle for 5 months, then the special coefficient will be equal to: 5: 12 = 0.42.

When calculating the transport fee, the engine power of the vehicle is taken as the basis for the calculation. Let's give an example. If a car engine has 100 hp. and a rate of 2.5 rubles is applied to it, then the owner of this vehicle will have to pay: 100 hp. * 2.5 rubles = 2500 rubles.

Absence of arrears to budgets of all levels and state extra-budgetary funds at the end of the tax period for which the taxpayer declared an exemption from payment of transport tax. The benefit is provided for one vehicle with an engine power of up to 150 horsepower

The provisions of the constituent documents (memorandum of association, charter, regulations and other documents) defining passenger and (or) freight transportation as the main type of activity, the purpose of creating the organization; availability of a valid license for cargo transportation and (or) passenger transportation; receipt of revenue from passenger and cargo transportation; systematic performance of passenger and (or) cargo transportation during navigation (for water vehicles); availability of reporting (including statistical) established by law on completed transportation of passengers and (or) cargo.

Absence of arrears to budgets of all levels and state extra-budgetary funds at the end of the tax period for which the taxpayer declared an exemption from payment of transport tax. The benefit is provided for one vehicle with an engine power of up to 200 horsepower

The Kaluga region, part of the Central Federal District of Russia, will be the topic for our next article. Following the article about the values of transport tax in Tver, we will talk about transport tax in Kaluga. In the middle of this year, there were suggestions in the Kaluga media that from the beginning of 2021, municipal authorities would reconsider the issue of transport tax rates for the 40th region, but no official statements were made. Today, transport tax is collected from Kaluga motorists at relatively low rates. This is especially noticeable for car owners who own cars with engines of less than 100 horsepower.

1. Taxpayers who are organizations, upon expiration of the tax period, pay tax no later than March 1 of the year following the expired tax period. During the tax period, at the end of each reporting period, advance payments are made no later than the 5th day of the second month following the reporting period.

Tax Code of the Russian Federation: “Payment of tax and advance payments of tax is made by taxpayers at the location of vehicles in the manner and within the time limits established by the laws of the constituent entities of the Russian Federation.”

one of the members of a large family registered in the Kaluga region as a large family in the manner established by the Law of the Kaluga Region N 8-OZ “On the status of a large family in the Kaluga region and measures of its social support” (05/28/2021), per vehicle engine power not exceeding 200 horsepower

.

7) one of the members of a large family registered on the territory of the Kaluga Region as a large family in the manner established by the Law of the Kaluga Region “On the status of a large family in the Kaluga Region and measures of its social support” (the benefit of this category of taxpayers is provided for one vehicle with engine power no more than 200 horsepower on the basis of a document confirming the status of a large family, issued by the authorized local government body of the Kaluga region in the field of social protection of the population);

Transport tax is levied on owners of various vehicles, who, in essence, pay the cost of each horsepower of their vehicle. Also, the tax rate includes the age of the vehicle. For owners of expensive vehicles, there are also additional fees “for luxury”, due to the fact that the engine power exceeds the minimum required for this class of vehicle.

Absence of arrears to budgets of all levels and state extra-budgetary funds at the end of the tax period for which the taxpayer declared an exemption from payment of transport tax. The benefit is provided for one vehicle with an engine power of up to 150 horsepower

Transport tax rates in 2021 are established by the laws of the constituent entities of the Russian Federation (Article 361 of the Tax Code of the Russian Federation). In the Tax Code of the Russian Federation, transport tax rates are established depending on the category of the vehicle and engine power (clause 1 of Article 361 of the Tax Code of the Russian Federation). Regions have the right to determine other tax rates, increased or decreased, but not more than 10 times (clause 2 of Article 361 of the Tax Code of the Russian Federation).