Deadline for payment of transport tax

The organization pays transport tax for each car registered to it. This obligation remains until the car is deregistered with the traffic police, even if you do not use it (clause 1 of article 358 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of the Russian Federation dated February 18, 2016 No. 03-05-06-04/9050).

The tax on a car registered for a separate subdivision is paid at the location of the OP (clause 1 of Article 363 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of the Russian Federation dated October 29, 2013 No. 03-05-04-04/45850).

The tax is transferred at the end of the year, and in some regions there are quarterly advances.

KBK - 182 1 0600 110.

Transport tax is regional, therefore:

- tax rate within the limits established by Ch. 28 Tax Code of the Russian Federation;

- procedure and deadlines for tax payment;

- tax benefits and the grounds for their use are determined by the laws of the constituent entities of the Russian Federation in whose territory the car is registered.

Organizational property tax

The property tax declaration form was approved by order of the Federal Tax Service of Russia dated August 14, 2019 No. SA-7-21/ [email protected]

In section 2, in the first part of line 230, indicate one of the tax benefit codes (2010501, 2010502, 2010503, 2010504). In the second part, enter zeros.

On line 240, enter the amount of the advance tax payment for the period from April 1 to June 30. For property whose cadastral value is taxed, fill out lines 110 and 120 of section 3 of the declaration in a similar manner.

If you are also eligible for other property tax benefits, in the first part of line 230, enter one of the following codes (2010505, 2010506, 2010507, 2010508). In its second half, sequentially indicate the number or letter designation of the article, part, paragraph, etc. law of the subject of the Russian Federation, which establishes the benefit. In line 240, enter the amount of the advance for the second quarter and the tax benefit. Fill out lines 110 and 120 of section 3 in the same way.

Procedure for calculating transport tax

According to Art. 362 of the Tax Code of the Russian Federation, organizations calculate the tax amount independently.

The tax period is a calendar year.

The tax is calculated for the year for each car registered to the organization (clause 1, clause 1, article 359 of the Tax Code of the Russian Federation).

Car tax = engine power in hp. x tax rate.

Engine power is taken from the title or registration certificate. If the power is indicated in kW, it should be converted to horsepower by multiplying by 1.35962. The result is rounded to the second decimal place. For example, 150 kW is 203.94 hp. (150 kW x 1.35962) (clause 19 of the Methodological recommendations for the application of Chapter 28 of the Tax Code of the Russian Federation).

Rates are established by the law of the subject of the Russian Federation in which the car is registered (clause 1 of Article 361 of the Tax Code of the Russian Federation).

If the rate depends on the age of the car, then it must be calculated from the year following the year of manufacture (clause 3 of Article 361 of the Tax Code of the Russian Federation). For example, the year of manufacture of a car is 2021. Then in 2021 it is 0 years old, in 2017 it is 1 year old, etc.

If the car was not used for a whole year, the tax should be adjusted by the coefficient Kv. The value of the coefficient is determined accurate to the 4th decimal place using the formula (clause 5.15 of the Procedure for filling out the declaration):

Kv coefficient = number of full months of vehicle operation / 12.

The month of purchase is included in the calculation if the car is registered before the 15th day inclusive. And the month of disposal of the car - if it is deregistered after the 15th (clause 3 of Article 362 of the Tax Code of the Russian Federation).

Having calculated the tax for each car, the results are summarized. Thus, the calculated tax for the year is obtained. If there are no advance payments in your region, this amount must be paid to the budget. If you paid advance payments, at the end of the year you will pay the difference between the calculated tax for the year and the advances.

Submitting a declaration and paying tax

Payers of transport tax are those organizations in which, in accordance with the legislation of the Russian Federation, transport is registered, recognized as an object of taxation, in accordance with Article 357 of the Tax Code of the Russian Federation.

Transport tax must be calculated for each registered transport in the organization.

The tax base for the tax is the engine power of the vehicle in horsepower. The engine power is indicated in line 10 of the PTS, in accordance with subparagraph 1 of paragraph 1 of Article 359 of the Tax Code of the Russian Federation.

Also, in accordance with paragraph 1 of Article 361 of the Tax Code of the Russian Federation, regional law establishes differentiated rates, which depend on the environmental class and age of the vehicle and tax benefits.

Advance payments and taxes are paid by the organization at the place of registration of vehicles (clause 1 of Article 363 of the Tax Code of the Russian Federation).

In what cases is it not necessary to pay transport tax?

There is no need to pay transport tax if the vehicle is registered and deregistered:

- in the period from the 1st to the 15th of the month;

- from the 16th to the 30th of the month;

- when registering after the 15th of one month and deregistering before the 15th of the next month;

- one day.

Such clarifications are given in the letter of the Federal Tax Service of the Russian Federation dated June 19, 2017 No. BS-4-21/ [email protected]

In addition, no tax is paid in case of car theft (letter of the Ministry of Finance of the Russian Federation dated October 3, 2017 No. 03-05-06-04/64192).

The agency explained which documents can exempt the owner of a car from paying transport tax if it is stolen.

According to paragraphs. 7 paragraph 2 art. 358 of the Tax Code of the Russian Federation, a vehicle will not be taxed provided that supporting documents from law enforcement agencies are provided to the Federal Tax Service. They may be:

- certificate of theft;

- resolution to initiate a criminal case.

In addition, the department reminded that a lost car can be deregistered with the State Traffic Safety Inspectorate (Order of the Ministry of Internal Affairs of the Russian Federation dated November 24, 2008 No. 1001). To do this, the owner will need to send an application to the appropriate traffic police department.

Let us note that Art. 85 of the Tax Code of the Russian Federation obliges the traffic police to independently, without the participation of the owner of the vehicle, report to the Federal Tax Service the fact of deregistration of a stolen car. This is done within 10 days. If a stolen car is found, it can be registered again.

Registration

Other taxes

Order of the Federal Tax Service No. ММВ-7-21/ [email protected] dated 12/05/2016

01/16/2017 Print

The following have been approved for reporting for 2021: a new form of transport tax declaration, the procedure for filling it out and the electronic submission form. At the same time, the previous declaration form, approved by order of the Federal Tax Service of Russia dated February 20, 2012 N ММВ-7-11/ [email protected]

Who will submit the declaration

Transport tax is levied on, among other things, cars, motorcycles, scooters, buses, other self-propelled machines and mechanisms on pneumatic and caterpillar tracks (Clause 1, Article 358 of the Tax Code of the Russian Federation). Legal entities and individuals to whom the above-mentioned vehicles are registered must pay transport tax (Article 357 of the Tax Code of the Russian Federation).

Organizations that pay transport tax will have to report using the new form.

How to fill out a declaration

The declaration should be completed:

- title page;

- Section 1 “Amount of tax to be paid to the budget”;

- Section 2 “Calculation of the tax amount for each vehicle.”

When filling out the declaration, code reference books are used:

- codes that determine the tax period, codes for the place of submission of the declaration, codes that determine the method of submission of the declaration - when filling out the title page of the declaration;

- codes of reorganization forms and code of liquidation of the organization - when the legal successor organization submits a declaration for the last tax period and updated declarations for the reorganized organization;

- codes of types of vehicles, codes of units of measurement of the tax base, codes of tax benefits and deductions - when filling out section 2 of the declaration.

Cost indicators must be rounded to the nearest ruble. Indicator values less than 50 kopecks are discarded, and 50 kopecks or more are rounded to the full ruble.

When filling out the declaration, it is important to take into account innovations compared to the previous edition. In particular, the title page, section 2 of the declaration to section V of the procedure for filling it out have changed.

As you know, from 04/07/2015 the obligation of business companies to have and use a round seal was abolished (clause 7, article 2 of the Federal Law of December 26, 1995 No. 208-FZ “On Joint Stock Companies”, clause 5 of article 2 of the Federal Law dated 02/08/1998 No. 14-FZ “On Limited Liability Companies”). Now a joint stock company or limited liability company may not have or use a seal, but only if federal law does not provide otherwise, and if the company’s charter does not contain information about the presence of a seal. In this regard, the new declaration form eliminates the obligation to certify it with the seal of a legal entity.

Added lines to section 2:

- date of registration of the vehicle (line 070) and date of alienation of the vehicle (line 080);

- tax deduction code (line 280) and tax deduction amount (line 300). They are needed by organizations that in 2021 paid a fee for damage to roads in relation to heavy vehicles registered to them from 01/01/2016. Such organizations reduce transport tax by the amount of the specified fee when calculating transport tax based on the results of the tax period - calendar 2021 (clause 1 of Article 360, clause 2 of Article 362 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of Russia dated 08/25/2016 No. 03-05- 06-04/49670 Federal Tax Service of Russia dated 08/12/2016 No. GD-4-11/ [email protected] ).

And in paragraph 5.1 of Section V of the procedure for filling out the declaration it now says: if, according to the law of a subject of the Russian Federation, transport tax is credited to the regional budget without sending the tax according to the standards to the budgets of municipalities, then one declaration can be drawn up for the total amount of tax for all vehicles located in the territory subject of the Russian Federation - in agreement with the tax inspectorate for this subject of the Russian Federation. Such approval must be obtained before the start of the calendar year for which the declaration is being submitted. For example, in order to submit a single declaration for 2021, this issue must be agreed upon by December 31, 2017. In this case, when filling out the declaration, indicate the OKTMO code corresponding to the territory of the municipality subordinate to the tax inspectorate at the place where the declaration was submitted.

When and how to submit a declaration

The new declaration form is applied starting with transport tax reporting for 2021. The declaration can also be submitted using the new form in case of liquidation (reorganization) of the organization before 02/28/2017.

And the declaration for 2021 should be filled out using a new form, if during this period the taxpayer paid a fee for damage to roads (letter of the Federal Tax Service of Russia dated December 29, 2016 No. PA-4-21 / [email protected] ). Transport tax reporting for 2021 must be reported no later than 02/01/2017.

It is allowed to send a declaration to the inspection:

- by the taxpayer personally or through his representative;

- by mail with a description of the attachment. In this case, the day of submission of the declaration is considered to be the date of sending the postal item with an inventory of the contents;

- in electronic form via TKS. In this case, the date of submission of the declaration is considered to be the date of its dispatch. Upon receipt of a declaration under the TCS, the tax office is obliged to provide the taxpayer with a receipt of its acceptance in electronic form;

- on paper - or with the attachment of removable media containing data in electronic form in an established format, or using a two-dimensional barcode.

Please note: if the initial declarations for 2021-2021 were submitted using a new form, then the updated declaration for these periods will also need to be submitted using a new form.

Transport tax when using the Platon system

Organizations can reduce the transport tax calculated at the end of the year in relation to each 12-ton truck registered in Platon by the amount paid for such a truck to compensate for damage to highways during the year (clause 2 of Article 362 of the Tax Code of the Russian Federation). Preferences apply to legal relations arising from January 1, 2021.

In addition, transport tax is a regional tax. When introducing it into effect in the territory of their region, legislative (representative) bodies of a constituent entity of the Russian Federation can establish differentiated tax rates for each category of vehicles, as well as taking into account the number of years that have passed since the year of production of vehicles and (or) their environmental class. Additional tax benefits may also be provided to owners of heavy trucks.

Letter of the Ministry of Finance of the Russian Federation dated 05/03/2017 No. 03-05-06-04/27086

Editor's note:

To confirm the right to deduct transport tax on heavy vehicles, you can use a special report that the owner of the car receives by accessing his personalized record in the Platon system (letter of the Federal Tax Service of the Russian Federation dated August 26, 2016 No. BS-4-11/15777).

Step-by-step instructions on how to fill out

Despite the fact that in the declaration form, after the title page, Section 1 follows, and then Section 2, in practice it is much more convenient to start filling out with the title page, and then move on to the second section, where the calculation is made for each car. At the end, fill out the first section, where the total amount is indicated.

Title page

So, filling begins with the title page:

- The TIN and KPP of the organization are indicated in the top field of the page. This data must be displayed on each page of the declaration.

- If information is transmitted initially, the correction number is indicated in the format “0—“.

- In the tax period column, put “34” - this value applies to the calendar year.

- The reporting year is the past year for which the tax will be transferred.

- The inspection code is 4 digits, the first two of which reflect the region, and the second - the specific department of the authority. You can find out about them in the inspection itself.

- The vehicle registration code is indicated in the following form: 213 – for the largest taxpayers, 216 – at the place of registration of the legal successor of such payers, 260 – at the location of the car.

- In a large field after the codes, the name of the enterprise is indicated; one cell is skipped between the words.

- The organization's activity code is indicated by the classifier.

- Be sure to include a contact phone number.

- It is better to indicate the number of pages in the document after all sections are completely filled out, especially if you own several vehicles.

- At the end, the full name of the taxpayer or his representative, the date of completion and signature are indicated.

The right side of the second block of the title page, where information about the submission of the declaration is entered, is filled out by an authorized inspector.

Section 2 for each car separately

At the second stage of filling out information is entered into Section 2:

- The meaning of the OKTMO code depends on the place of registration of the car; you can find it on the official website of the tax office (line 020).

- The next field indicates the vehicle type code (line 030). All of them are divided into three groups:

- aircraft;

water vehicles;

- ground vehicles.

The taxpayer needs to select a value in accordance with the vehicle he has. For example:

- code 510 00 – for passenger cars;

- 520 01 – trucks;

- 530 01 – agricultural tractors;

- 530 03 – combines;

- 411 13 – cargo aircraft;

- 420 10 – vessels for transporting passengers and goods by river and sea.

The full list of codes is specified in Appendix No. 5 to Order No. ММВ-7-21/ [email protected]

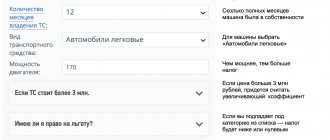

- if the vehicle is equipped with an engine, the power size in hp is indicated;

TN = Vehicle Power * rate * Kkv * Kp.

- 20210(220)(230) – complete exemption or reduction in the amount of payment under Art. 356 Tax Code of the Russian Federation;

Depending on the type of vehicle, the code values will change; you should refer to the Appendices to the Order.

Section 1

The last section to be completed is the first section of the declaration . It contains the following information:

- KBK for tax payment;

- OKTMO code by which payment is made;

- total amount of transport tax;

- amounts of advance payments, if provided for by regional legislation;

- the amount of tax to be transferred to the budget, taking into account advances.

If the amount to be paid, after taking into account advance payments, turns out to be negative, then the value is indicated without the minus sign (how to calculate advance payments?). In this case, the tax is not transferred, but the declaration is still provided.

How to apply an increasing coefficient for transport tax

The list of passenger cars with an average cost of 3 million rubles, subject to use in the next tax period, is posted no later than March 1 of the next tax period on the official website of the Ministry of Industry and Trade of the Russian Federation on the Internet. This follows from paragraph 2 of Art. 362 Tax Code of the Russian Federation. The cost of the car and the moment of its registration do not play a role.

Particular attention should be paid to the last column of the list, which indicates the age of the car, which is calculated from the year of manufacture. For example, a car that was released in 2021 is 1 year old in 2016, 2 years old in 2021, etc. (letter of the Ministry of Finance of the Russian Federation dated May 18, 2017 No. 03-05-04/30334, Federal Tax Service of the Russian Federation dated March 2, 2015 No. BS-4-11 / [email protected] ).

If there is a car on the list, but its age is different, the increasing factor is not applied (letter of the Federal Tax Service of the Russian Federation dated January 11, 2017 No. BS-4-21/149).

If your car is on the list, then for 2021 you will pay tax with an increasing coefficient.

| Group of cars according to the list | Year of car manufacture | Kp coefficient |

| From 3 to 5 million rubles. | 2017 | 1,5 |

| 2016 | 1,3 | |

| 2015 | 1,1 | |

| Over 5 to 10 million rubles. | 2013 and later | 2 |

| Over 10 to 15 million rubles. | 2008 and later | 3 |

| Over 15 million rubles. | 1998 and later |

The process of filling out sections 1 and 2 of the transport declaration

First, you need to calculate the amount of tax that needs to be paid into the budget. To do this, we will skip the subtleties of filling out the first section and go straight to the second, where these calculations are performed. It will be clearer this way. So, instructions for filling out section No. 2:

- Enter the TIN and KPP of the organization at the top of the page (as was done on the title page);

- In lines 020 and 030, enter the code of the vehicle type and its place of registration. The Federal Tax Service website will help you find the code you are looking for. To do this, go to the resource, find electronic services there and the “Learn OKTMO” tab. For example, for a simple passenger car the code may be 510,000;

- Line 040 is intended for the VIN code of cars, serial number for aircraft and for watercraft;

- Next, we accurately copy the vehicle brand from the registration certificate, then in lines 060 and 070 – its registration plate number and registration date, respectively;

- Line 080 is filled in if the car has been deregistered. In this case, the date when this happened is written here, otherwise we put a dash;

- Next, write the tax base code and the unit of measurement of the tax base (OKEY).

- For all land vehicles, the country's Tax Code has established that the base is calculated in horsepower, so in line 100 we enter code 251;

- Then it remains to indicate the environmental class of the machine and the period of its operation (in months);

- Next, write the year of manufacture of the vehicle and the number of years that have passed since that moment (lines 120 and 130);

- Now comes the important point about car ownership shares. If it has only one owner, make a record in the format 1 dash/1 dash.

Line 160 implies the need to calculate how many months the vehicle has been owned relative to the number of months in this year. Line 170 indicates the tax rate, which may vary depending on the place of registration of the vehicle. Local authorities of each subject of the Russian Federation have the right to set the value of this coefficient themselves, so you need to find out the data regarding your region. Now, in more detail about line 180 , in which you need to note the increasing Kp coefficients (if any will be applied). They may vary depending on the type of car. Here are the current rates for passenger vehicles:

- 1.1 for cars whose average price does not exceed 5 million rubles and no more than 3 years have passed since the date of issue;

- 1.3 – if the price of the car is up to 5 million, but one to two years have passed since the release date;

- 1.5 for cars that were produced less than a year ago and cost up to 5 million rubles.

Rates increase for cars whose price reaches 10 million rubles and more than 5 years have passed since the date of their release - the coefficient is 2. With an average cost of a car up to 15 million, if it was produced no more than 10 years ago, a coefficient of 3 is applied. A similar one will be applied, if the car is more expensive than 15 million and was produced no more than 20 years ago. Lines 200 to 290 are filled in provided that the taxpayer is entitled to benefits. If the company owns several cars at once, calculations using a similar principle must be performed independently for each of them. The resulting tax amount to be paid is entered in the appropriate lines of the first section.

Section #1:

The transport tax return for 2021 must be submitted using a new form

Order of the Federal Tax Service of the Russian Federation dated December 5, 2016 No. ММВ-7-21/ [email protected] approved a new form, format for submitting a transport tax declaration in electronic form, as well as the procedure for filling it out.

Starting with the report for the tax period 2021, the already updated version of the declaration must be used.

What has changed in the declaration:

- Section 2 “Calculation of the tax amount for each vehicle”: new lines have appeared (070, 080, 130) to reflect the date of registration of the vehicle, the date of termination of registration and the year of manufacture of the vehicle;

- for owners of heavy trucks who pay a fee for damage to roads, the updated declaration provides special lines (280 and 290) to reflect the tax deduction code and the amount of the deduction calculated in rubles;

In connection with these innovations, the Federal Tax Service of the Russian Federation has developed control ratios with which you can check the correctness of filling out reports. In particular, a new control link has appeared between the tax deduction (p. 290) and data obtained from the register of the toll collection system to compensate for the damage caused by heavy trucks to highways (letter of the Federal Tax Service of the Russian Federation dated March 3, 2017 No. BS-4-21 / [email protected ] ).

Previously, taxpayers reported on transport tax in the form approved by Order of the Federal Tax Service of the Russian Federation dated February 20, 2012 No. ММВ-7-11/ [email protected]

Criteria for filling out the form

Order No. ММВ-7-21/668 provides the procedure for generating a document and describes how to correctly fill out a transport tax return. It is recommended that all taxpayers adhere to this algorithm, which will greatly simplify the process and spend less time submitting reports.

General filling requirements:

- The document must be generated based on the results of the reporting year (tax period); All indicators must be rounded according to the rules of mathematics (values over 50 kopecks are rounded up, less than 50 kopecks are not taken into account);

- It is necessary to enter continuous page numbering, starting from 0001 – the title page. The number is indicated from left to right; on the title page it is necessary to note the total number of completed declaration sheets;

- The use of duplex printing or correction tools to correct inaccuracies or errors is not permitted;

- If the document is filled out manually, you can use a pen with blue, purple or black ink. The font chosen is capital, printed;

- Each indicator has its own field. If any of them is missing, a dash is added;

- If the declaration is filled out on a computer, Courier New font size 16-18 is used.

There are several formats for submitting a document: in paper form or in electronic format. The document can be submitted to the tax authority personally by the taxpayer, through his official representative acting on the basis of a power of attorney, or sent by Russian Post.

Procedure for filling out the declaration

First, section 2 of the declaration is completed for each vehicle. The vehicle type code (line 030) is indicated in the appendix to the procedure for filling out the declaration. Data about the car - identification number (VIN), make, registration number, registration date, year of manufacture are taken from the title or registration certificate. The registration termination date (line 080) is indicated only for vehicles that were deregistered in the reporting year.

The tax base (line 090) is the engine power in horsepower. Line 100 indicates the horsepower code - 251.

The environmental class (line 110) is reflected in the PTS. If it is not there, a dash is placed in line 110.

Line 120 is filled in only if the tax rate depends on the number of years from the year of manufacture of the car.

Line 140 indicates the number of full months of car ownership during the reporting year, and line 160 indicates the Kv coefficient. If you owned the car all year, put 12 in line 140, and 1 in line 160.

Line 150 places 1/1.

The Kp coefficient (line 180) is indicated only for expensive cars.

Lines 190 and 300 reflect the calculated tax.

Lines 200–290 are filled in if benefits are used.

After filling out section 2 for all cars, you can move on to section 1.

Lines 021 and 030 display the total tax amount for all cars if advances are not paid.

If advances are paid, they should be indicated in lines 023–027, and in line 030 - the tax payable at the end of the year.

Step-by-step instructions for filling out the declaration

The document includes three sections:

- Title page;

- Section 1;

- Section 2.

Let's look at the sample filling in 2021 in more detail. A correctly designed title page includes the following elements: TIN and KPP of your organization (written at the top of the sheet), they are also duplicated at the top of each page of the transport declaration.

You can find out the treasured numbers by opening the certificate of registration of the organization with the tax authorities. If the declaration is submitted initially, code 0 is entered; in a situation where changes have already been made to the document, code 1 or 2 is written (if a second adjustment was made). Next, the year for which the declaration is submitted and the tax period are written down. The name of the legal entity-taxpayer is written in exactly the same format as it is written in the constituent documents. Next, indicate the code of the type of economic activity assigned on the basis of the all-Russian classifier. On the title page you also need to indicate the mobile taxpayer number without extra spaces or characters, but with the country and city code. If additional documents are attached to the declaration, they must be identified with a number (for example, 3 or 4). Further on the title page there is a section in which you need to confirm the accuracy of the entered information. If the declaration is filled out by the manager himself, code 1 is entered, but if his authorized representative is filled out, code 2. All that remains is to sign and date. There is no need to fill out anything else on the title page; the data in the section on the right is entered by the tax authority employee.