Cost calculation

The cost of an MTPL insurance policy is calculated based on the level of the base tariff rate, which is approved by the government of the country, and correction factors.

The base rate is calculated depending on the category of the vehicle. The following indicators are considered as correction factors:

- vehicle engine power;

- term of use;

- duration of the relevant agreement;

- driver's age and experience;

- the number of persons who may be allowed to drive a vehicle;

- area of use of the car;

- the presence of past fines received as a result of traffic accidents;

- the presence or absence of insurance payments from a specific organization.

The MTPL agreement does not provide for payment of the policy in installments, but the client can achieve significant savings. When concluding an appropriate agreement, you can pay for the policy only for 3 months, and then extend it for a similar period. After this, the client of the insurance organization will need to pay only 0.3 of the total cost for the remaining period.

How much does OSAGO cost for 6 months?

Parking signs for even and odd days of the month in Russia in 2018

In order to calculate the cost of insurance, it is necessary to use the following indicators:

- Current tariff plans.

- Increased or decreased indicators (coefficients).

- Duration of insurance.

Tariff plans are determined by the Central Bank of the Russian Federation and change every year for both individuals and legal entities. For example, for the winter of 2021, tariffs for an individual for passenger cars will be a little more than four thousand rubles, and for a legal entity at the same time, a little more than two and a half thousand Russian rubles.

- Kn - an indicator of violations that were noticed during the validity of previous insurances.

- Kc – seasonality indicator. That is, at what time of year (or all year round) the vehicle will be used.

- Km is an indicator that characterizes the engine power of a vehicle.

- Ko is an indicator of either a limited OSAGO policy or an unlimited one.

- Kvs is an indicator of the driver’s age and how long he has been using the car.

- KBM is a bonus-malus indicator that can provide significant discounts to the policyholder.

- Kt is an indicator of the territory, which depends on the region of location and use of the insured vehicle.

- TB is the basic tariff (tariff plan), which is determined by the Central Bank of Russia.

Indicators can be in the following numerical ranges:

- CT is determined in the range from 0.7 to 2.

- KBM – from 0.4 to 2.40.

- FAC – 1-2.

- KO – 1-1.8.

- KM – 0.5 – 1.5.

- KS – 0.5 – 1.1.

- KN – 1 – 1.6.

The cost of the insurance policy will also depend on the duration of use of insurance services. More precisely, it is precisely this that will determine the final price of a six-month insurance policy. From the calculation formula it is clear that prices are not at all stable, since the number of indicators in the formula is impressive and all of them can change over even a short period of time.

Most insurers believe that the cost of a six-month policy is equal to half the cost of an OSAGO policy for a year, which is a completely erroneous statement. As already mentioned, the payment will not be 50% of the annual policy, but 70%, but it can be paid in installments.

As you know, there is a basic tariff (price) for compulsory motor liability insurance. Various coefficients are applied to this tariff, which depend on the driving experience, age of the driver, and region of registration. To calculate the cost of compulsory motor liability insurance for six months, there is a reduction factor, which for compulsory motor liability insurance for 6 months is 0.7.

Owner registration region:

MoscowMoscow regionSt. PetersburgLeningrad regionKaluga - Obninsk - other cities Kal. Tula region - Aleksin, Efremov, Novomoskovsk - Uzlovaya, Shchekino - other cities of Tula. region Astrakhan - Astrakhan region Belgorod - Belgorod region Vladimir - Vladimir region Volgograd - Volzhsky - Kamyshin, Mikhailovka - other cities Vol. Voronezh region - Voronezh region Krasnoyarsk - Norilsk, Zheleznogorsk - Minusinsk, Kansk - Krasnoyarsk region Kursk - Kursk region Nizhny Novgorod - Nizhny Novgorod region Novosibirsk - Novosibirsk region Orel - Oryol region Penza - Penza region Perm - Perm region Ryazan - Ryazan region Samara - Togliatti - Samara region Saratov - Engels – Saratov region Smolensk – Smolensk regionKhanty-Mansiysk – Nefteyugansk, Nyagan – Nizhnevartovsk – Surgut – Khanty-Mansi Autonomous Okrug Yamal-Nenets Autonomous Okrug (Novy Urengoy) – Yamalo-Nenets Autonomous Okrug Yaroslavl – Yaroslavl region

It should be taken into account that when applying for a period of six months for using compulsory motor liability insurance, you can choose any one and even break it into parts, for example, three months in the spring and then another three months in the fall.

Considering that all other coefficients (both increasing and decreasing) are applied to the base rate, it turns out that in some insurance companies the insurance policy may cost more, and in others less.

When buying compulsory motor liability insurance for six months, the price for which in 2021 is 70% of the full policy, many ask questions about how much it will cost to extend compulsory motor liability insurance to 9 (nine) or 12 months.

If you want to extend your MTPL insurance policy for six months, then don’t worry, because... You will not overpay. You will simply pay the difference between a MTPL policy for six months and a policy for 9 (nine) or 12 (twelve) months.

The calculation of the MTPL policy for six months, the cost, price and discount can be found in the calculator on our website. To do this, click on the “Compulsory Motor Liability Insurance” button.

How to calculate compulsory motor liability insurance for a minimum period of time?

When calculating a contract for a short period of time, so-called term coefficients are applied. To find out the price of a document, for example, for 90 days, you need to multiply the cost of the annual contract by the coefficient of the desired term.

The value of the coefficient depends on the required time.

| Number of months | Coefficient |

| 3 | 0,5 |

| 4 | 0,6 |

| 5 | 0,65 |

| 6 | 0,7 |

| 7 | 0,8 |

| 8 | 0,9 |

| 9 | 0,95 |

| 10 | 1 |

| 11 | 1 |

It turns out that when buying insurance for the shortest period (three months), the driver will pay half of the cost of the annual policy, if purchasing for six months - 70% of the total amount, and for 10, 11 months - it will cost the same as the full one.

Paper and electronic versions

Increase in gasoline prices in 2021 in Russia, latest news

When applying for a civil liability policy, or OSAGO online, you can choose one of two options:

- The traditional, paper version is printed on a special form for strict reporting. Despite the typographical protection, there have been cases of forgery and theft of forms. The consequences of using fraudulent insurance are equally unpleasant for both the culprit and the injured party.

- The electronic version is protected from counterfeiting. All data on the car, the car owner and drivers are stored in the company’s database. A file is sent to the policyholder's email, which must be printed on a regular A4 sheet and presented at the request of the traffic police inspector when checking documents or in the event of an accident.

How much does it cost to renew OSAGO

money-trans.ruHow to change data in compulsory insurance online. How to make changes to your compulsory insurance policy

In order to calculate the cost of insurance, it is necessary to use the following indicators:

- Current tariff plans.

- Increased or decreased indicators (coefficients).

- Duration of insurance.

Tariff plans are determined by the Central Bank of the Russian Federation and change every year for both individuals and legal entities. For example, for the winter of 2021, tariffs for an individual for passenger cars will be a little more than four thousand rubles, and for a legal entity at the same time, a little more than two and a half thousand Russian rubles.

- Kn - an indicator of violations that were noticed during the validity of previous insurances.

- Kc – seasonality indicator. That is, at what time of year (or all year round) the vehicle will be used.

- Km is an indicator that characterizes the engine power of a vehicle.

- Ko is an indicator of either a limited OSAGO policy or an unlimited one.

- Kvs is an indicator of the driver’s age and how long he has been using the car.

- KBM is a bonus-malus indicator that can provide significant discounts to the policyholder.

- Kt is an indicator of the territory, which depends on the region of location and use of the insured vehicle.

- TB is the basic tariff (tariff plan), which is determined by the Central Bank of Russia.

Indicators can be in the following numerical ranges:

- CT is determined in the range from 0.7 to 2.

- KBM – from 0.4 to 2.40.

- FAC – 1-2.

- KO – 1-1.8.

- KM – 0.5 – 1.5.

- KS – 0.5 – 1.1.

- KN – 1 – 1.6.

The cost of the insurance policy will also depend on the duration of use of insurance services. More precisely, it is precisely this that will determine the final price of a six-month insurance policy. From the calculation formula it is clear that prices are not at all stable, since the number of indicators in the formula is impressive and all of them can change over even a short period of time.

As you know, there is a basic tariff (price) for compulsory motor liability insurance. Various coefficients are applied to this tariff, which depend on the driving experience, age of the driver, and region of registration. To calculate the cost of compulsory motor liability insurance for six months, there is a reduction factor, which for compulsory motor liability insurance for 6 months is 0.7.

Owner registration region:

MoscowMoscow region St. PetersburgLeningrad regionKaluga - Obninsk - other cities Kal. Tula region - Aleksin, Efremov, Novomoskovsk - Uzlovaya, Shchekino - other cities of Tula. region Astrakhan - Astrakhan region Belgorod - Belgorod region Vladimir - Vladimir region Volgograd - Volzhsky - Kamyshin, Mikhailovka - other cities Vol. Voronezh region - Voronezh region Krasnoyarsk - Norilsk, Zheleznogorsk - Minusinsk, Kansk - Krasnoyarsk region Kursk - Kursk region Nizhny Novgorod - Nizhny Novgorod region Novosibirsk - Novosibirsk region Orel - Oryol region Penza - Penza region Perm - Perm region Ryazan - Ryazan region Samara - Tolyatti - Samara region Saratov - Engels — Saratov region Smolensk — Smolensk regionKhanty-Mansiysk - Nefteyugansk, Nyagan - Nizhnevartovsk - Surgut - Khanty-Mansi Autonomous Okrug Yamal-Nenets Autonomous Okrug (Novy Urengoy) - Yamalo-Nenets Autonomous Okrug Yaroslavl - Yaroslavl region

It should be taken into account that when applying for a period of six months for using compulsory motor liability insurance, you can choose any one and even break it into parts, for example, three months in the spring and then another three months in the fall.

When insuring a vehicle for six months, you can buy a policy cheaper if you choose the right insurance company. Despite the fact that the basic tariffs are set by the Central Bank, there is a gap in which the insurers themselves set their tariff.

Considering that all other coefficients (both increasing and decreasing) are applied to the base rate, it turns out that in some insurance companies the insurance policy may cost more, and in others less.

When buying compulsory motor liability insurance for six months, the price for which in 2021 is 70% of the full policy, many ask questions about how much it will cost to extend compulsory motor liability insurance to 9 (nine) or 12 months.

If you want to extend your MTPL insurance policy for six months, then don’t worry, because... You will not overpay. You will simply pay the difference between a MTPL policy for six months and a policy for 9 (nine) or 12 (twelve) months.

The calculation of the MTPL policy for six months, the cost, price and discount can be found in the calculator on our website. To do this, click on the “Compulsory Motor Liability Insurance” button.

Is it possible to extend the policy?

Let’s say if you insured your car for three months with the aim of selling it later, but you were unable to do so. Then you can come to the insurance company where you signed the contract and renew the policy for a year, paying half the cost of the annual insurance for the remaining nine months. After all, you have already paid for three months as for six months.

If you paid for the policy for six months, then when you renew it you will need to pay accordingly, as for three months.

Payment in installments for compulsory motor liability insurance is not provided, but you can still break the entire amount into several parts to pay throughout the year. For example, take out insurance first for three months, then extend it for another three months and for six months. Then you get the following: first 0.5 of the annual cost of insurance, then 0.2 and 0.3 at the end.

Of course, this method will require a lot of time and filling out additional paperwork, but it is quite acceptable for those who have some financial difficulties and cannot pay for all the insurance for the year at once.

Yes, three-month insurance can be extended for a period of three to nine months or up to a year at once. But please note that in order to renew the policy, you will need to contact the insurance company before the expiration of the insurance period specified in your MTPL agreement.

Example Let's take the same VAZ 2105 car. If you entered into an MTPL agreement on September 2, 2012 for a period of 1 year and indicated that you will drive the car for exactly three months, that is, until December 1, 2012, then in order to extend the period of use of the car up to a year, you will need to contact the insurance company before December 1 and pay the second half of the amount. Otherwise, the insurance company has the right to refuse to extend the period of use of the vehicle.

The annual cost of the insurance in question is constant. Generally accepted rules determine that a compulsory insurance contract is always concluded for one year. This rule is indicated in the upper right corner of the policy.

However, if the vehicle needs to be sold in the near future, then it is insured for a minimum period. This change in the rules can significantly reduce the costs of the vehicle owner. If plans related to the sale do not materialize, then the opportunity is given to extend the insurance until the end of the policy year.

An example is the following information: if insurance was concluded on September 2, 2021 for 1 year, subject to the vehicle being used for 3 months (expiration date December 1, 2021), then you should apply for an insurance renewal before December 1. Otherwise, the insurance company may refuse to provide such a service.

- You can extend your insurance for another 3 months and so on until 9.

- Only the renewal must be carried out through the company’s office.

- A mandatory condition is to extend the contract before the expiration of the previous policy. The date and month are specified in the MTPL agreement.

- If it happens that the deadlines are missed, then a new contract is drawn up.

- In this case, there will be an overpayment when compared with the price of an annual policy.

To renew, follow these steps:

- you need to visit the branch of the company where the policy was purchased for three months;

- the necessary documents are prepared, which initially include the current diagnostic card;

- the contract period is extended.

Often, company employees offer to conclude a new agreement, but this is unprofitable for the car owner.

It has the same capabilities and nuances as a standard motor vehicle policy, but at the same time its cost is 50% less than a yearly policy. If necessary, you can extend its validity, but such a solution is considered unprofitable in financial terms.

If the vehicle is to be sold, it is insured for a minimum period. This step allows the car owner to significantly save money.

If for certain reasons the sale does not take place, the insurance can be extended until the end of the policy year. For the remaining 9 months you will need to pay half the annual cost of compulsory motor insurance (the same as for the first 3 months). Thus, having paid 0.7 annual compulsory motor insurance for the first 6 months, for the next you will pay 0.3 annual insurance.

How to renew the policy and the amount of the fine for late document

According to the provisions of the Code of Administrative Offenses, every driver who gets behind the wheel of a vehicle is required to have a valid auto liability policy. An expired document automatically loses its validity, and a driver with such a policy is subject to administrative punishment. Therefore, the car owner must take care in advance to renew the policy if the MTPL insurance period is coming to an end.

Extension of a previously concluded contract is not difficult. To do this, the owner of the car must pay the required amount for the months remaining before the standard annual period. So, if the contract was concluded for six months, then the policyholder will need to pay money for the remaining 6 months.

There are two ways to extend an already concluded contract:

- During a personal visit to the auto insurer's office.

- Through the official website of the insurance company.

To renew your insurance, you will need to provide company employees with the following documents:

- Personal passport of the policyholder.

- Driver's licenses of all persons included in the policy.

- Registration certificate of the vehicle for which insurance is issued.

- Diagnostic inspection card (for cars over 3 years old).

For driving a vehicle without a valid MTPL policy, an administrative fine is imposed. The amount of the penalty is 800 rubles , according to Art. No. 12.37 Code of Administrative Offences. The driver should take into account that an expired contract, from a legal point of view, is equivalent to a completely absent one. Therefore, from the day following the expiration of the insurance period, the driver may be subject to administrative penalties. In addition, if he gets into an accident, he will have to compensate himself for all the damage he caused.

Calculation of tariffs by insurance period

Do not confuse the period of use of the car with the period for which the contract was concluded. As a general rule, a compulsory insurance contract is concluded for a period of one year, with the exception of compulsory motor liability insurance for cars registered in foreign countries and temporarily used in Russia, as well as transit insurance used to travel to the place of registration of the vehicle.

An MTPL policy is a guaranteed paid liability of a vehicle driver to other road users. The guarantee is that if the insured person participates in any road accident, his liability to the victims will be compensated not by him personally, but by the funds of the insurance company that has assumed such an obligation according to the contract.

Legislatively, insurance standards are enshrined in the Civil Code of the Russian Federation and Law 4015-1. The rules for the provision of MTPL insurance services are established by Law No. 40-FZ, as last amended on May 23, 2016.

Minimum

The minimum period for which it is allowed to issue a civil liability insurance policy is fixed at three months. The procedure for concluding an agreement is not particularly different from the standard one, except for indicating the term and tariff.

When contacting an insurance company to purchase a policy for three months, the applicant will be asked for the following package of documents:

- personal identification document;

- special digital code received from the State Tax Inspectorate;

- driving license of the driver and all other drivers if they will drive this vehicle;

- title document for the vehicle;

- application in the prescribed form for insurance.

For half a year

The option of car insurance for six months is used mainly by large enterprises that use special equipment. These vehicles are not always used in everyday life all year round, therefore the state at the legislative level allows issuing policies for such devices as needed.

The package of documents for legal entities is slightly different from the physical one and is supplemented with the following documents:

- a notarized power of attorney allowing you to represent the interests of the organization;

- document on state registration of the company;

- car diagnostic card;

- Have a wet seal with you to certify documents.

Of course, individuals are also allowed to take out a policy for six months, but the cost of insurance significantly hits the owner’s pocket.

For a year

By concluding an insurance contract for the whole year, you don’t have to monitor the terms, as in other types of policies.

To understand what the savings will be if you take out MTPL for a minimum period, you can independently calculate the amount of insurance.

Now let's talk in more detail about each coefficient:

- Kt – coefficient of territorial affiliation of the vehicle. Its value is determined depending on the place of residence of the car owner.

- Kbm – bonus-malus coefficient. Accrued depending on the period of accident-free driving.

- Kvs – coefficient of the policyholder’s age category.

- Ko – the number of people included in the policy;

- Km – coefficient depending on vehicle power

As is clear, the higher the vehicle’s power rating, the more expensive the MTPL insurance policy will cost, be it for one month or for a longer period.

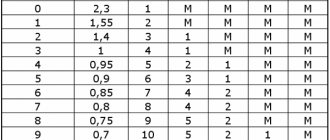

In addition, one more point is worth noting. There is a plate containing data on the fractional cost of the insurance contract.

From these data it is clear that when purchasing compulsory motor insurance for a minimum period of 3 months, the motorist must pay exactly half of the finished cost of insurance. A 6-month auto license will cost 2/3 of the base price of an annual contract.

Read on, is it possible to take out a compulsory motor liability insurance policy and then change the insurance period?

A more detailed period of use of the insurance policy is indicated in the lines below in the form. Therefore, the form itself takes into account both the general insurance period provided for by Law No. 40-FZ “On Compulsory Motor Liability Liability Liability Insurance” and clarification of the terms of use of the motor vehicle license - for a different number of months.

When breaking down the policy, its periods of use, by month of the year, each driver must understand that during other periods of time the car insurance contract will be considered invalid.

As is clear, companies insure for any period. And which design option is the most profitable, everyone decides for himself, because everything depends solely on the specific case.

Minimum insurance period under compulsory motor liability insurance

Car insurance rules apply to all insurance companies and are the same for motorists in the Russian Federation.

Moreover, the conditions are somewhat different for individuals and organizations. For what minimum period can you insure your car for these cases?

For individuals

Ordinary citizens use cars for personal purposes. They can buy a policy that insures for a period of three months. Tariffs for those registered as an individual entrepreneur apply exactly the same, and accordingly, the terms for them will be the same.

It should be noted that the minimum insurance period, although established by law, may depend on the specific company. Some do not adhere to the minimum period, but prefer to enter into an agreement only for 6 or 12 months, no less.

Car owners from other countries are allowed to purchase a policy from 5 days to 6 months. If a week is not enough for a car owner, then you can sign an agreement for a longer period, for example, 30 days. This practice occurs quite often, because the circumstances of a foreigner’s stay in Russia may change, and he will have to stay longer. In order not to worry about the safety of the car once again, it is insured for a longer period.

Based on the permit, foreign citizens are required to renew their policies in order to move freely on Russian roads.

Cars that travel under their own power from the place of purchase to the place of residence of the owner are usually insured for a period of 20 days. This time is just enough for the haul.

Let's summarize what kind of policies individuals are allowed to take out. persons:

- Primary (up to 15 days) - for foreigners.

- Transit (20 days) - for transported cars.

- Public (from three months) - for all motorists.

There are different situations in life, so sometimes purchasing compulsory motor liability insurance with a shortened validity period turns out to be very useful. If you plan to put the car up for sale, it is advisable to insure it for a shorter period of time. In the future, it will be possible to extend this period. This operation costs less than purchasing a full-fledged MTPL policy.

OSAGO is not sold in installments, but the car owner can distribute the costs of paying for the insurer’s services with full right and certain benefit. Main stages of payment:

- 90 days, in which case the cost of 0.5% of the insurance is charged;

- contract extension (coefficient applies from 0.2%);

As a result, it turns out that the annual cost of the policy is still paid, but only in parts.

This method can be convenient under different circumstances, since you don’t have to overpay when renewing. If you take out insurance anew each time, then a certain coefficient is calculated, which increases the price of the car insurance. You must strictly adhere to the terms of prolongation (extension) of insurance, otherwise you will have to re-issue it.

For legal entities

By law, legal entities (organizations, enterprises, companies) are required to purchase car insurance for a period of 6 months. But issuance for 20 days is also possible if the vehicles have transit plates. Many organizations buy vehicles in other regions, so in practice this type of agreement is often used. It is not profitable for companies to insure the transport of legal entities for a short period of time, but they make concessions to satisfy the needs of their clients.

Ten-month or annual insurance is approximately the same. Only in rare cases are organizations and vehicle fleets allowed to insure equipment for a shorter period if it is used seasonally (for clearing snow in winter).

Registration of a policy

It is important to distinguish between two criteria when obtaining an MTPL policy:

- insurance period;

- service life of the vehicle.

These two factors may not coincide in timing. For example, you bought insurance for six months, and the period of use of the vehicle will be 7 months. Then, after the expiration of the insurance policy, you will need to renew it additionally, since it will no longer be valid.

According to the legislation of the Russian Federation, the standard period for concluding an agreement between an insurance company and a citizen is a year. Usually in the upper right corner they indicate the start date of its validity, from which the actual year begins.

It should not be confused with the calendar calendar, which begins on January 1. This does not prohibit citizens from purchasing a policy for a shorter period.

It can be obtained for a shorter period, but in very specific cases:

- when driving a vehicle to the place of registration (for example, the car owner bought it in one subject of the Russian Federation, but will use it in another);

- if the vehicle is traveling to another inspection location.

In these cases, the driver is issued temporary transit insurance for 20 days. This is not prohibited by law, according to Federal Law No. 40, Article 10, Clause 3. Its calculation is determined by various factors: engine power, car brand, etc.

For a period of 5-15 days, you can get insurance for cars that are registered in another country, but are temporarily located in Russia. The policy registration process undergoes minor changes.

OSAGO insurance for a month is possible only if you need to use the vehicle for a period of 4 or 7 months. Then insurance is issued for 3 months or six months and additional insurance for the remaining period. This is the only way to get car insurance for a month.

Is it possible to apply for compulsory motor liability insurance for six months? This is not prohibited by law, since the shortest insurance period is 3 months, and for legal entities this is exactly this period.

Insurance for 3 and 6 months has other features:

- they cost more than a simple annual one (insurance for 3 months will cost 50% more than a year; for 6 months - 70% more, and a policy for 10-11 months will cost the same as for 12);

- The cost of insurance for a year does not change during the year, whereas if a driver purchases temporary insurance and then decides to renew it, he may have to pay an additional amount. Therefore, just in case, it is recommended to immediately find out the price of the policy for a year;

- if the driver operates the car from time to time, then he can immediately write down the year with the insurance company (three months in summer, one in winter, etc.), since the total number of months in a year is calculated.

The most common cases of using insurance for 3 or 6 months:

- when operating the vehicle only in the summer (for example, for trips to the country);

- when selling a car, when it takes time to find a buyer and prepare documents;

- for drivers going on temporary business trips.

In order to obtain insurance, you must contact the insurance company with the following list of required documents:

- A statement indicating some of your own data.

- Passport of a citizen of the Russian Federation for whom insurance will be issued.

- Documentation for the vehicle whose operation there is a desire to protect.

- A document confirming the ownership of the vehicle by the applicant.

- Driver's licenses of those persons who will use the vehicle in the future.

The short term of the policy does not mean that it will be quite cheap. Often, the longer the policy period, the less significant the amount of financial resources you need to pay for it.

How much insurance should I take out to register my car?

Car insurance is always necessary, since without it, vehicles are prohibited from driving on the roads. After purchasing a vehicle, it is better to choose the most profitable option for a car title, since its cost is constantly growing. It is most advisable to take out a policy for a year at once. After doing some calculations, you can understand that this is much more profitable than a short period.

Payment for a shorter period is calculated taking into account a coefficient that can increase the price by 20%, or even 60%. For example, for MTPL for 3 months you will have to pay almost twice as much as for the same months, but with annual coverage. And if you sign a contract for 6 months, you will have to pay for it as for seven months. And if you take out a policy for 9 months, it will cost the same as an annual one.

In addition, the cost of car insurance services is constantly increasing. Given this trend, you will have to pay more for each new short period. And after signing a contract for 12 months, the insurer no longer has the right to charge an additional payment from the owner due to an increase in tariffs.

Even for the purpose of attracting clients, the insurance company does not have the right to enter into an agreement for only one or two months. The minimum time cannot be reduced as it is established by law.

To register a car without any problems, the minimum duration of insurance must be 3 months. To avoid standing in line, you can get it online.

When going out on the road, each driver must have a printed copy of the electronic MTPL insurance or a regular form received at the office.

How much will it cost

If you take out insurance for six months, the procedure for calculating the cost of the MTPL policy remains unchanged, but you need to take into account that the final price is less profitable than if you entered into an agreement for a whole year (what is the price of an annual policy?).

You can find more complete information about the conditions and cost of obtaining temporary insurance here, and in this article we talked about the features and prices of a policy with an insurance coverage period of 3 months.

The price for a car license agreement depends on a number of factors (region, driver experience, etc.) and may change over time. Each type of car has its own basic tariff.

The cost of the insurance premium is calculated based on:

- Base rate.

- Odds that can either lower or increase the base rate.

- Period of insurance coverage of the policy.

Basic tariffs for auto insurance policies are set by the Central Bank and cannot be higher or lower than the maximum permissible values. You can read more about the factors influencing the cost of compulsory motor insurance and the differences in prices in different insurance companies in this article.

Calculation procedure

Your base rate depends on the following criteria:

- Type of your vehicle.

- From the person who owns the vehicle (individual or legal entity).

Today the basic tariff for passenger cars is:

- For individuals 1980 rub.

- For legal entities persons 2375 rub.

- For cars used as taxis RUB 2,965. You can read more about MTPL for taxi drivers here.

Coefficients for calculating the amount of insurance premium:

- The territoriality coefficient depends on the region in which the vehicle will be used and varies from 0.7 to 2. For small cities where the risk of accidents is lower, this value will be 0.7; for larger cities, this coefficient will be higher, but not more than 2.

- The accident rate, or bonus malus as it is also called, depends on the number of accidents in which the driver of the vehicle was involved in the previous period and ranges from 0.5 to 2.45.

- When drawing up a motor vehicle license agreement, the Insurance Company assigns vehicle drivers a class from 1 to 13. If you have no driving experience or it is minimal, then you will be issued a third class with a coefficient of 1. If you have a long driving experience, then you can get the highest class for accident-free driving with a coefficient of 0.5.

If during the previous insurance period the driver was involved in 4 accidents in which he was the culprit, then he will be assigned the lowest class with the highest coefficient of 2.45. - The driving experience and age of the driver also affect the final cost of the insurance premium.

The maximum coefficient of 1.8 will be received by drivers whose driving experience is less than 3 years and whose age is less than 22 years. If the driver’s driving experience is more than 3 years, then he is assigned a coefficient of 1. You can find out more about the coefficients and cost of compulsory motor insurance for beginners in this material. If this vehicle is driven by several drivers, then this coefficient is assigned to the driver who has the shortest experience and age. - In case of violations, a coefficient of 1.5 is assigned. This coefficient will be applied only to drivers who have violations such as: driving a vehicle while intoxicated, gross traffic violations, etc.

- If you take out a policy with a limited number of drivers, then you will be assigned a coefficient of 1, and for an unlimited number of drivers there is a maximum coefficient of 1.8. You can find all the information about compulsory motor liability insurance without restrictions on the number of drivers in this article.

- Also, the final cost of the insurance premium depends on the power of your vehicle - the coefficient in this case varies from 0.6 to 1.6. The smallest coefficient will be received by cars with a power of less than 50 hp. and the maximum coefficient is provided for vehicles whose power exceeds 150 hp.

- Also, the price of the policy depends on the age of your vehicle. The smallest coefficient of 0.5 is provided for cars less than 10 months old, the maximum coefficient in this case is 1.

- The final amount of the car insurance premium is determined by the period of insurance coverage. The shorter this period, the lower the final amount of the insurance premium. The price of insurance issued for 6 months will be equal to 70% of the annual cost of the OSAGO contract and when calculating the final premium amount, a coefficient of 0.7 will be applied.

IMPORTANT! Since an auto liability insurance contract is always issued for 1 year, the cost of extending a contract concluded for six months should not be higher than 30% of the cost of this contract for a year

How much does a car policy cost?

The policyholder can issue an insurance contract for any number of months, starting from 3 months. The insurance premium for such insurance is correspondingly less than for a standard year.

The difference is 50% of the annual cost. It is worth paying attention that when recalculating monthly, the price of 1 month is more expensive. In addition, the cost of a car insurance policy depends on many factors, which will be discussed below. Without taking them into account, it is impossible to name the exact cost of compulsory motor liability insurance.

What does the price depend on?

In addition to the insurance period, other factors also affect the cost of the policy . These include:

- Age and driving experience of the persons who will be included in the contract (how much does MTPL cost for a novice driver?).

- Car model.

- Region of vehicle registration (can a policy be issued in another region?).

- Engine power.

How to calculate?

There are two ways to calculate the cost of a car license:

- Using an online calculator.

- Make the calculations yourself.

To carry out calculations online, you can use the RSA website. The system will display two numbers: the maximum allowable and the minimum. More accurate data can be obtained using the online calculator on the website of the already selected insurer.

When making your own calculations, it is better to rely on Bank of Russia Instructions No. 3384-U dated September 19, 2014. It contains all the necessary coefficients and base rates. Calculations are made using the following formula:

T = TB x KT x KBM x KVS x KO x KM x KS x KN Let’s decipher the letter designations:

- TB - basic tariff for individuals who do not use a vehicle as a taxi - 3432-4118 rubles. The insurer may use a rate within these limits.

- CT – territoriality coefficient.

- KBM – bonus-malus coefficient. It depends on the driver’s class and the availability of insurance payments.

- KVS – driver’s age and experience coefficient.

- KO – used for limited insurance.

- KM – vehicle power factor.

- KS – insurance period is 3 months, so the coefficient is 0.5.

- KN - this coefficient is used only in case of violations in the previous period.

How to buy MTPL for three months online through the broker YOUR CASCO

From the beginning of 2021, insurance will mainly be issued online and issued to clients in the form of an electronic compulsory motor liability insurance policy, which each driver will still need to print out.

If you buy a car on credit, then financial institutions will definitely require you to take out insurance. But it is worth remembering that the cost of insurance for a new car will be much cheaper than the cost of registration for a NOT new car.

Therefore, before purchasing, we recommend that you look at promotions and offers that will allow you to save significantly when buying a car.