On April 1, 2015, new territorial OSAGO coefficients came into effect, and on April 12 of the same year, basic tariffs came into effect. After this innovation, policies increased in price by an average of 40% and many owners are afraid of a further increase in prices for compulsory motor liability insurance.

In this article we will look at what the cost of compulsory motor liability insurance depends on and how the tariff system for pricing an insurance policy has changed over time? What are the prospects in this direction and is it true that the only reason for the constant increase in prices is the desire of insurers to earn more?

What is the base rate?

The cost of an MTPL policy is calculated based on a number of fixed variables, the main one being the so-called base rate.

The basic tariff is understood as a legally established amount, on the basis of which the cost of the policy is subsequently determined by applying various coefficients. The basic cost is the same for all citizens of the country, regardless of region, driving experience and other individual parameters. The only parameter that is taken into account when calculating the basic tariff is the type of vehicle; for example, for a truck this figure is 1.5 times higher than for a passenger car.

According to the law (No. 40-FZ dated April 25, 2002), all powers to regulate basic tariffs are vested in the Central Bank of the Russian Federation. Since the introduction of the first MTPL rate in 2003, it has remained unchanged for a long time. In determining its value, the regulator was primarily guided by the principle that the amount of money collected by companies from the sale of policies should exceed the costs of paying insurance premiums.

The first increase in the base tariff occurred in October 2014. It was due to the fact that over many years, during which the rate did not change, while the economic situation had seriously changed and, taking into account inflation, the funds received by organizations from the sale of policies were simply no longer enough to cover payments for insured events. As it turned out later, the new prices did not last long, and their increase itself was one of the urgent measures to stabilize the car insurance market. A full revision of prices and the establishment of new base rates for compulsory motor liability insurance policies from April 1, 2015 at the time of publication of the instruction of the Central Bank of the Russian Federation No. 3604-U.

Formula for calculating compulsory motor liability insurance

The tariff corridor within which the cost of compulsory motor liability insurance can be set is strictly controlled by the regulator, which is the Central Bank of the Russian Federation. The price depends on several factors, so it is different for each car owner.

The cost is determined by a formula where the base MTPL rate is multiplied by the coefficients.

Formula for calculating compulsory motor liability insurance: T = TB x KT x KBM x KVS x KO x KM x KS x KN x KPr

- TB - basic tariff

- CT - territorial coefficient

- KBM - bonus-malus coefficient

- KVS - age and length of service coefficient

- KO - limiting the number of drivers

- KM - power factor

- KS - seasonality coefficient (period of use)

- KN - violation coefficient

- KPR - trailer coefficient

Previously, the rate was fixed, but now companies are reducing rates to attract customers. Most often, beginners have favorable conditions. Old-timers in the insurance market with big names rarely make discounts. Their trump card is a high reliability rating.

Tariff corridor from April 1, 2015

According to the above-mentioned instructions of the Central Bank of the Russian Federation, instead of a fixed base rate, a so-called tariff corridor was introduced, allowing companies to use any amount in the range from 3,432 to 4,118 rubles for the initial calculation of the cost of the policy. This decision was made based on the following considerations:

- To create competition in the MTPL market, and, as a result of competition, to improve the quality of auto insurance. When the rate was a fixed amount, the offers of most companies were not much different from each other, and the struggle for clients took place mainly only at the advertising level, since more serious steps in this direction were impossible, due to a clearly defined limitation in the price of the policy.

- Provide insurance organizations with flexibility in terms of setting prices for different categories of clients (individuals, individual entrepreneurs, pensioners, etc.) and different regions.

At the moment, it cannot be said that the measures taken are working effectively, since the price corridor is practically not used. Due to the long validity of the previous tariff system, the sale of MTPL policies was an unprofitable enterprise for many companies. In this regard, insurance organizations simply increased prices, basing their cost calculations on the new maximum allowable rate of 4,118 rubles (for example, Renaissance Insurance, Soglasie, Uralsib established such a rate in all regions of the Russian Federation, and SOGAZ, Ingosstrakh, VSK, AlfaStrakhovanie, RESO -Warranty in most regions).

How does the price corridor work in practice? Let's say we have a standard 120 hp machine. The owner of the car (over 22 years old) lives in Moscow, has over 3 years of driving experience, and has not previously been insured. Depending on the base rate, the price of an annual policy for a given vehicle can range from 8,236 to 9,883 rubles, that is, the difference is almost 20%.

OSAGO coefficients

The basic tariff (TB) of MTPL is approved by the Central Bank of the Russian Federation, and additional coefficients are established based on the provisions of Federal Law No. 40 and the addition of additional regulations. The value of the coefficients can either reduce the final cost of the policy or increase it. Let's consider the meaning of each of them.

Territorial coefficient

This value indicates the area of primary use. TK reflects the intensity of traffic: the greater the traffic flow, the higher the cost of the policy. The highest traffic is in Moscow, in the Moscow region it is already lower. The level of congestion on the roadway increases or decreases the risk of accidents. This coefficient was planned to be cancelled, but at the last moment it was retained.

The TC is calculated at the place of registration of the driver or at the place of registration of the vehicle (for firms, companies). The value will be different for cars, trucks and tractors.

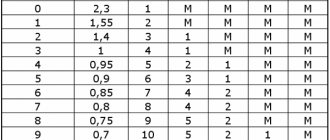

Bonus-malus coefficient

This value reflects the participation of a car in an accident. This is the accident rate. For accident-free driving it will be much lower than for those involved in an accident. Moreover, the bonus is reduced only in the absence of insurance payments. If his own vehicle was damaged in an accident due to the driver’s fault, CASCO insurance is paid.

Using the KBM table you can calculate your bonus malus. It states:

- driver class (for beginners it will be equal to 3);

- coefficient corresponding to the class (beginners – 1);

- a zero coefficient means no compensation for an accident;

- unit – one accident with payment of compensation;

- two – 2 accidents, etc.

The tables reflect the change in driver class, depending on the presence/absence of accidents and insurance compensation.

The KBM for each driver included in the policy is calculated separately. As a result, the highest accident rate is taken.

If several drivers are indicated in the MTPL, the maximum value is taken for the KBM. That is, it is unprofitable to include inexperienced drivers with a high risk of accidents in your insurance. Firstly, they can damage the car. Secondly, the cost of the policy becomes many times higher because of them.

Driver age and experience

FAC is an indicator of the driver’s professionalism. The more years, the more experience and the less risk of an accident. If the contract includes young people (up to 20 years old) with minimal driving experience (up to three years), the final cost of the policy will be high. With unlimited compulsory motor liability insurance, PIC 1 is automatically set.

Limits on the number of drivers

KO is the coefficient of restrictions. There are two types of motor vehicle:

- with a limited number of drivers;

- no limits.

In the first case, persons authorized to drive the vehicle are included in the insurance. If you need to add to the list of permitted drivers, contact the Investigative Committee employees for this. In the second case, any driver can drive the car with the approval of the vehicle owner; a driver’s license is required.

For compulsory motor liability insurance with restrictions, the KO is equal to one, for a policy without restrictions, the KO is 1.87.

Unlimited insurance costs much more, almost twice as much. This is due to the coverage of possible risks of an emergency situation caused by inexperienced drivers. A policy with restrictions takes into account the experience and age of all drivers, which increases (reduces) the final price.

Engine power

KM characterizes the vehicle according to horsepower. We planned to remove this parameter from the list of coefficients, but changed our minds. For one unit we took a motor with a power of 50 to 70 hp. With. (Horse power).

The higher the engine power, the higher the cost of the policy.

KM value for MTPL:

- less than 50 l. With. – 0.6 units;

- 50 – 70 l. With. – unit;

- 70 – 100 – 1.1 units;

- 100 – 120 – 1.2 units;

- 120 -1 50 – 1.4 units;

- 150 and above – 1.6 units.

Size and other external factors do not affect engine power, only horsepower.

Violation rate

This value (KN) characterizes cases of violation of the insurance contract. These violations are not related to the emergency situation, but to the rules of the Investigative Committee itself. Violations include:

- false documents;

- obviously false information.

The following are considered violations:

- intentional actions causing harm to health or threat to life;

- causing harm under the influence of narcotic substances – alcohol, drugs;

- driving a car by a person who does not have the right to do so;

- leaving in danger;

- willfully leaving the scene of an accident before traffic police officers appear;

- other unlawful cases established by the Investigative Committee.

Expert opinion

Ivan Strahovsky

Insurance expert

OSAGO calculator

If violations are detected, the insurance company will increase the cost of compulsory motor liability insurance by 1.5 times . This applies to both the owner of the vehicle and drivers registered in the MTPL. Even if there is one violation, the coefficient increases.

Insurance period

The CP is used for cars registered abroad. The basis is the unit denoting one year.

- 5 – 15 days – 0.2;

- 16 – 30 days – 0.3;

- 2 months – 0.4;

- 3 months – 0.5;

- 4 months – 0.6;

- 5 months – 0.65;

- 6 months – 0.7;

- 7 months – 0.8;

- 8 months – 0.9;

- 9 months – 0.95;

- 12 months - 1.

The cost of the policy depends on the number of days insured. The fewer there are, the lower the price.

Seasonal coefficient

KS is the seasonality coefficient. it also affects the final insurance amount. For example, if a car owner uses a vehicle not all year round, but for a certain period, it is not cost-effective to pay for annual insurance. Equipment for removing snow, watering a flower bed or harvesting fruits is used for a limited period of time. However, this rule applies only to special types of equipment, and not to passenger cars.

Trailer coefficient

CPR characterizes an increased risk of an emergency, as the total weight of the vehicle increases and control deteriorates.

- passenger vehicles, motorcycles – 1.16;

- freight transport, tractor – 1.24;

- other type of transport – 1.

the presence of a trailer in the application for compulsory motor liability insurance .

Table of basic MTPL tariffs in 2021

The table below shows the basic rates for compulsory motor liability insurance in force in 2021.

| Vehicle type | Tariff corridor | |

| Min. amount, rub. | Max. amount, rub. | |

| Motorcycles, mopeds | 867 | 1 579 |

| Cars | ||

| For legal entities | 2 573 | 3 087 |

| For individuals | 3 432 | 4 118 |

| For taxi | 5 138 | 6 166 |

| Trucks | ||

| With a maximum weight of less than 16 tons | 3 509 | 4 211 |

| With a maximum weight of more than 16 tons | 5 284 | 6 341 |

| Vehicles for transporting passengers | ||

| With a number of passenger seats up to 16 inclusive | 2 808 | 3 370 |

| With more than 16 passenger seats | 3 509 | 4 211 |

| Trolleybuses | 2 808 | 3 370 |

| Trams | 1 751 | 2 101 |

| Tractors, self-propelled road construction machines | 1 124 | 1 579 |

The influence of the driver’s age and experience on the outcome

This coefficient directly depends on the age of the driver himself and his driving experience. The minimum premium will be for an insurance holder who is over 22 years of age and has at least 36 months of driving experience. Drivers under 22 years of age, with zero driving experience (after driving school), will pay the maximum.

It is important to understand that if several drivers have the right to get behind the wheel, then the maximum coefficient is taken, and for an unlimited number of people who can use the car it is equal to 1.

| № | Experience and age | Coefficient |

| 1 | The driver is under 22 years old and has less than three years of experience | 1,8 |

| 2 | The driver is over 22 years old and has less than three years of experience | 1,7 |

| 3 | The driver is under 22 years old and has more than 3 years of experience | 1,6 |

| 4 | The driver is over 22 years old and has more than three years of experience | 1 |

Other innovations of the Decree of the Central Bank of the Russian Federation No. 3604-U

It is worth noting that with the introduction of the order, not only the total cost of the policy increased, but also the maximum amount of insurance payments. If previously it was 120 thousand rubles for compensation for damage caused to property, and 160 thousand rubles for compensation for harm to life and health, then in 2021 the maximum payment limit would be increased to 400 and 500 thousand rubles, respectively.

Along with the adoption of the law on new tariffs, the Central Bank obliged all insurance companies to post and promptly update relevant information about the cost of the policy on their websites and online calculators. And in theory, any citizen, choosing the appropriate MTPL option for himself, can go online and check out the prices. However, in practice, most organizations hide the base rates page deep in the depths of their websites. Apparently, there is an unspoken agreement between insurers on this matter to counter dumping.

In addition to the new tariff rate, the Central Bank decree also provided for a change in regional coefficients. This parameter is determined for different regions based on the degree of road congestion and the average accident rate in the area. The highest coefficient is set for cities such as Murmansk, Chelyabinsk - 2.1; Kazan, Perm, Tyumen, Moscow, Surgut - 2. The cheapest new insurance will cost residents of regions such as the Chechen Republic, the Republic of Dagestan, Kalmykia, Crimea, Trans-Baikal Territory - coefficient 0.6.

Features of calculating the cost of an MTPL policy

When calculating the cost of a car license, the following are taken into account:

- registration;

- age, driving experience;

- driving history;

- insurance company rates in the area.

Registration

To reduce the price of compulsory motor liability insurance, you can insure a vehicle for a relative registered in a small city or village. This matters for a car owner registered in a metropolis. The risk of an accident in large cities increases several times, and accordingly, the price for a vehicle license will increase. As a result, you can pay half as much money for the same insurance.

Age and experience of drivers

The older the drivers included in the insurance contract, the lower the final price of the auto insurance policy. This is due to the risk of accidents on the roadway. It is assumed that young motorists are much more likely to get into accidents than older ones. If you include a young driver in your MTPL contract, you should prepare for increased cash costs.

Driving history

The increase in the total for the vehicle license depends on this item. If drivers included in the policy often violate the rules of the DD, there is a risk of reducing the class to the lowest. The reduction in class (and increase in price) depends on the insurance company paying compensation to repair damaged cars and other property of the victims.

Expert opinion

Ivan Strahovsky

Insurance expert

OSAGO calculator

Accident-free driving increases the bonus malus every year, which gradually reduces the cost of the vehicle license . But if the lists of persons allowed to drive include drivers who were involved in road accidents, this reduces the BMR indicator and increases the total amount.

Prices of companies in your city

Prices for compulsory motor insurance differ from company to company, since the Central Bank has allowed deviations from the established norm by 40%. You can find out about prices in your city on the RSA website, which contains information about all members of the union in different regions of the Russian Federation.