CASCO and OSAGO - what are the differences?

First of all, drivers should understand the difference between the two types of insurance, which are widely used in the Russian Federation. In the case of compulsory motor liability insurance, only the owner's liability is insured. This means that if you are the culprit of the accident, then the policy is used to compensate the victim. However, if you were injured, then your compulsory motor liability insurance is not involved, since the payment must be made through the insurance of the person responsible for the accident. OSAGO is mandatory for all motorists.

Drivers can take out CASCO insurance at their own discretion, and this type of insurance is issued for a wide variety of cases - theft, accident, road accident, damage due to adverse weather conditions, and so on. Unfortunately, voluntary insurance is not fully regulated by government agencies, and it is much more difficult to obtain CASCO compensation. Insurers are resourceful and will try to deny payments.

Using voluntary insurance is a purely personal decision. However, you must know what to do if OSAGO does not pay or underestimates the amount.

Cases when the insurance company denies compensation under compulsory motor liability insurance

Dear readers!

Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem, please contact the online consultant form

It's fast and free!

Or call us by phone (24/7):

If you want to find out how to solve your particular problem, call us by phone. It's fast and free!

What else to read:

- My car was scratched in the yard, what should I do?

- Europrotocol 2021

- How to get money instead of repairs under compulsory motor liability insurance: a detailed review

+7 (495) 980-97-90(ext.589) Moscow,

Moscow region

+8 (812) 449-45-96(ext.928) St. Petersburg,

Leningrad region

+8 (800) 700-99-56 (ext. 590) Regions

(the call is free for all regions of Russia)

First of all, read the list of situations when you do not receive payment under compulsory motor liability insurance. These rules are enshrined in regulations. This includes:

- not an insured event - there is no confirmation of the fact;

- there is no way to assess losses, for example, during quick repairs or disposal of a car;

- the driver who caused the accident does not have valid MTPL insurance;

- the insurance owner did not inform the insurer about the emergency;

- moral damage or lost profits are not compensated;

- an emergency occurred on the training ground during a training ride, during testing or in competitions;

- the damage was caused by special cargo;

- the car was damaged during loading and unloading operations;

- damage has been caused to the environment - spill of fuel, chemically active substances, etc.;

- force majeure circumstances - military operations, floods, fires and other natural disasters.

Please note that damage to passengers or persons in the performance of official duties is indemnified under other types of policies. All of the points described above are legal grounds for refusing to pay drivers, so you won’t be able to seek compensation even in court.

The insurance company is required to issue a refusal in writing, detailing the reason. If you think that the reason for the refusal is dubious and your case is not included in the list described above, then you can try to seek compensation in pre-trial or court proceedings.

The insurance company refused to pay: what to do? Instructions

Below we will look in more detail at how to act in order to challenge the illegal refusal of insurance compensation. Cases where no response was received from the insurer at all also fit here, because the algorithm in a dispute with the insurer is the same.

Do I need to do an independent examination?

Let's say right away that you do not have such a responsibility. But whether it is necessary or not, you will have to decide for yourself. The thing is that the costs of conducting an independent examination may not be reimbursed to you, especially if the insurer did conduct at least some inspection of your car.

The simplified procedure for filing an application and disagreements does not contain a mandatory requirement for an examination, and there are no such requirements when contacting the financial ombudsman. Therefore, the victim now does more of the examination for himself, in order to know how much he is still owed and whether he is owed at all.

But part of the examination is an inspection of the car, drawing up a report and taking photographs. This is the procedure you will definitely need. Since it is better to send photographs of all damage to the financial ombudsman yourself, and not hope that the insurer will present them.

Step No. 1: Statement of disagreement in the Investigative Committee

It is easier and better to submit the application using the standard form, which has been approved by the financial service. This way, it will be considered faster and it will be easier to submit it electronically.

This can be done either through your personal account on the insurer’s website or through the application form there on the website. You can also send it to the official mail, which is listed in the register of insurers.

- in case of refusal of insurance payment under MTPL.

- .

Example contacts of some insurance companies:

- PJSC IC "ROSGOSSTRAKH" - email address. mail, official website: https://www.rgs.ru;

- JSC "AlfaStrakhovanie" - mail, website: www.alfastrah.ru;

- JSC "RESO-Garantiya" – email. mail, office website: www.reso.ru.

You should pay attention to some nuances.

- If you do not know the exact amount of the claims, write 400,000 if you require only insurance compensation, and 800,000 if you require both payment and penalty. No one will pay you more than these amounts anyway.

- If you contact the insurance company at fault and you do not have your own policy, then indicate the policy of the second participant and the date of its conclusion. Information on the policy can be obtained on the RSA website.

- Describe the essence of the requirements at your discretion: in detail, or briefly.

An electronic application is essentially a scanned version of the original paper application with a live signature.

It is necessary to record the sending, if by email, then send letters with delivery notification, print a copy of the sent letter. A copy can be sent to your address.

In paper form, either hand it in with a mark at the company’s office, or send it by registered mail with a list of the contents and notification.

Step #2: Contact your financial ombudsman

Again, it is easier, faster and more reliable to send an appeal through your personal account on the website of the financial ombudsman.

The amount of text there is limited, so be sure to indicate the main points and data in the text, and you can attach a detailed statement as a separate file.

.

Here we also present the nuances of this appeal.

- If you do not have a copy of the insurance policy, please attach a printout from the RSA website when sending an application for refusal under MTPL.

- If you want the financial ombudsman to consider your application instead of being refused and going to court, then attach as many documents and evidence in your favor as possible, including photographs of damage that can be examined.

- Now experts have started calling the victims and asking about examining the car. If the car has already been repaired, or they cannot show it, then they simply tell the financial officer that they could not inspect it and cannot carry out an examination. He, in turn, stops consideration. To avoid this, show the car, even if it has been repaired, and, if possible, record documents and negotiations. Tell the experts that photographs of the damage are on file.

- If the authorized person does not like something or requests some additional documents, they can be sent through a new appeal indicating the number of the previous one.

Remember that the insurer is not interested in considering this dispute by the ombudsman, so he may not provide him with any documents at all, which means that everything will depend on your appeal and your evidence.

Step #3: Go to court

At this stage, be careful - you can go to court within 30 days after the decision of the financial ombudsman comes into force, do not miss this deadline. If you missed it, apply for reinstatement indicating valid reasons for missing it.

The requirements that must be submitted are those that were stated in previous applications to the Investigative Committee and the financial institution. If you did do an examination, then submit it to the court and demand payment for it either as damages or as legal expenses, depending on whether the insurer examined the car or not.

Below are a number of nuances.

- If the commissioner refused to consider or terminated it for some reason, then in the statement of claim, in addition to the basic requirements for the Investigative Committee, you must indicate where the financial officer was wrong and why he had to consider your application and make a decision.

- The examination of the financial ombudsman is equivalent to a judicial one, that is, in order to challenge it, one must not only apply for a judicial examination, but also justify why the financial examination is bad.

- A copy of the claim will need to be sent to the authorized person; this can already be done by mail. The application itself is enough, without attachments, since the law says nothing about applications.

- The court must attach evidence of compliance with the pre-trial procedure, that is, either a financial decision, or an agreement with the insurance company, which was concluded at the commissioner stage, or a notification from the financial service about the acceptance or refusal of your application.

We strongly recommend that you familiarize yourself with the explanations of the Supreme Court on FINUPU.

Rules regarding deadlines

A common reason is when the insurance company does not pay under the compulsory motor liability insurance within the specified time frame. The law stipulates that the insurer is obliged to consider your case within 20 calendar days, excluding weekends and holidays. This period may increase to 30 days if the car is sent for repair to a workshop with which the insurer has an agreement. During these days, the insurer is obliged to compensate for losses in accordance with the insurance or provide a justified refusal.

Delays can be caused not only by the incompetence of insurance company specialists. Often the problem arises with a car service that eliminates the consequences of an accident. A long negotiation on the cost of repairs, a shortage of spare parts or a long queue - all this can cause delay. If the deadlines were violated or you are not satisfied with the refusal, you can go to court to resolve this issue.

How to counteract

To avoid problems when insurers allegedly did not receive the necessary documents, require confirmation from insurance employees. Make copies of documents that indicate the date and number of the incoming letter. Additionally, ask for the copies to be stamped and signed by the responsible person. Thanks to this, insurers will not be able to freeze you out.

To review cases, insurers can request a certificate from the traffic police. However, a document can take quite a long time to arrive by mail. As a result, due to a lack of materials for the examination, your payment will be delayed. Remember that if you need such a certificate, it is easier and faster to take it yourself.

Arbitrage practice

MTPL insurance from a well-known company does not always guarantee that problems with receiving payments in the future will not arise. In court, they most often defend their rights when the refusal was not in writing or the established deadlines were grossly violated. In this case, you don’t have to go to the Central Bank or RSA, but immediately send a claim. It is realistic to study such cases on the official resources of the judicial system of the Russian Federation in order to objectively assess your chances.

Failure to pay compensation on time under compulsory motor liability insurance is a common practice faced by many victims of road accidents. Not everyone knows what to do in such a situation and how to react to violations by the insurer. Having familiarized yourself with the approximate procedure, you can confidently defend your rights in government agencies.

Payment amount

A common complaint is that insurance companies pay drivers little. It is necessary to study the question of how much a driver can legally receive under a motor vehicle insurance policy. The maximum amount for property is 400 thousand rubles. If there are victims of an accident or harm to health - 500 thousand rubles. If a large amount is needed to compensate for the accident, then the missing money is recovered from the culprit of the accident. The examination to determine the amount is carried out in accordance with current regulatory documents or according to the assessment of representatives of the insurer.

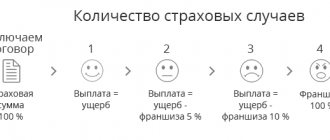

There are two main cases of distribution of cash payments:

- classic - for an amount of 500 thousand 25 for the funeral procession and 475 relatives of the deceased;

- reduced when the insurer, due to various tricks, deliberately reduces the insurance payment.

To exclude the second option, it is recommended to resort to an independent examination.

Pre-trial proceedings

Litigation is an expensive, lengthy and unpleasant process not only for drivers, but also for the insurer. In most cases, representatives of compulsory motor liability insurance try to avoid litigation, so first of all, try to achieve pre-trial payments.

Step 1: Independent examination

If the insurer did not make a payment, did not provide a refusal within the specified time frame, or you are not satisfied with the amount of compensation, then first perform an independent examination. First, you will need it to file a claim. Secondly, it will be useful when going to court in the future, if the case comes to pass.

The procedure for ordering an examination consists of the following steps:

- Search for a specialized company, an independent specialist. You must first make sure that the appraiser has the appropriate license or agreement.

- Agreeing on the time and place of the examination with the appraiser and a representative of the insurance company. It is recommended to notify the insurer by registered mail.

- Carrying out an examination. They can take place without a representative of the insurance company if the latter does not appear at the agreed place and time.

- Providing an expert report with photographs.

The presence of the insurer does not affect the independent examination. He can observe and ask questions. Once you have the results in hand, be sure to make multiple copies.

Step 2: Claim

Sample claims are at the end of the page.

Before resolving issues in court, the driver is required to file a claim with the insurer, which stipulates disagreement regarding the decision or claim for violation of the law. The insurer, for its part, is obliged to resolve this issue within 10 working days. The company may issue a written refusal, which will already be the basis for further legal proceedings, or satisfy your requirements.

The claim form can be found on specialized Internet resources. The document must be handed over personally in the office to an authorized employee against signature or the claim must be sent by registered mail with notification and inventory to the insurer. This will eliminate situations where you are waiting for a response to a claim that has not even reached the addressee. When preparing a pre-trial claim, consider several important nuances:

- indicate in your claim comprehensive information – policy number, circumstances and reasons why you do not agree with the insurer’s decision;

- the document is drawn up in two copies - you give one, and the second remains in the hands of the driver;

- If for some reason it is impossible to personally deliver a letter or they refuse to accept it, send a claim via mail with notification of receipt.

Please note that the insurance company does not have the right to refuse without reference to the relevant legislation. Otherwise, this is a direct reason to resolve the issue in court.

Step 3: Contact the Russian Union of Insurers (RUA) or the Central Bank of the Russian Federation

PCA will be useful if there are serious violations in your relations with insurers, for example, an unjustified refusal to pay or a demand for unspecified documents. The union also deals with issues related to the bankruptcy of an insurance company. If your problem is a disagreement with the amount of payment, then skip this step and get ready for court.

A similar function is performed by the central bank, which regulates the activities of all financial institutions in the country. The bank can punish for direct violation of the law, but the Central Bank of the Russian Federation will not resolve disputes between drivers and insurers.

There are standardized forms of contacting these bodies. Additionally, leave your contact information and attach all documents that prove that you are right. If the insurance company does not pay under compulsory motor liability insurance and the steps described above did not help, the only option left is the court.

Step 4: Trial

The court decides all issues relating to the collection of fines, compensation for damage caused and compensation for moral damage. However, be prepared that the process may drag on for months, not to mention the costs of a lawyer. The first thing you need to do is prepare a complete list of documents with which you can go to court. This includes:

- Statement.

- Receipt for payment of state duty.

- A document about the relationship between the plaintiff and the Investigative Committee, a receipt for payment.

- Copies of documents.

- A copy of the refusal to pay.

- A copy of the pre-trial claim.

- A copy of the insurance company's response to the pre-trial claim.

- A copy of the vehicle certificate.

- A copy of the insured person's passport.

- A copy of the power of attorney (if the plaintiff is represented by another person).

The lawsuit contains the following information:

- Full name of the judicial authority.

- Plaintiff's details (full name, address, telephone number).

- Name of the insurance company (full name, legal address).

- The essence of the claim. Amount of damage. penalty for non-payment. Costs of litigation.

Documents can be submitted in person through the court office or by registered mail. However, preparing documents is only half the battle. The most difficult thing is to prove that you are right at the meeting. For this purpose, it is allowed to use photographs, videos, eyewitness testimony and more. The plaintiff may also request assistance from the court if special permission is required to obtain any evidence.

A positive court decision will oblige the insurance company to pay the full amount of compensation plus a fine of 50% of this amount. Additionally, legal expenses are compensated. Thus, your investment and lost time will pay off, but only if you are sure that the insurer’s decision is illegal. Statistics show that a quarter of compensation payments under compulsory motor liability insurance are carried out in court. This suggests that insurers quite often underestimate the amount of payments or neglect specific conditions and facts.

What is the deadline for filing a claim?

You may not have to submit a statement of disagreement for a long time - 3 years from the moment you learned that you were illegally refused, or when the deadline for a response has expired, but no response has been sent. But it’s not in your best interest to delay filing.

In situations where the insurer illegally refuses to pay insurance compensation, it is better to quickly go to court and ask for the current penalty there than to wait, and then the court will reduce this very penalty.

Plus, the period for consideration of your application will depend not only on the method of submission, but also on the period; if more than 180 days pass from the date of refusal, then the statement of disagreement will be considered by the insurer for up to 30 days.

If the insurer goes bankrupt

All insurance contracts for which an insured event did not occur are canceled in case of bankruptcy. However, according to current legislation, the insurer is obliged to pay amounts for damages to policyholders who have submitted the relevant documents.

If there are assets left after liquidation, they are sent to pay insurers. The problem is that these funds are primarily used to pay off wages and taxes. Also, in case of bankruptcy of a company, revocation of a license, or the impossibility of identifying the culprit of an accident, payments are made by RSA. You should expect the following payments:

- up to 160 thousand for compensation for damage to health;

- up to 160 thousand for damage to the property of several persons;

- up to 120 thousand for damage to the property of one person.

Non-payment under compulsory motor liability insurance

If the insurance company refuses to pay, this does not mean that the client is not entitled to legal compensation. Let’s try to answer the question in more detail: if the insurance company doesn’t pay, what should you do? First, let's understand all the intricacies and consider what types of insurance payments exist at the moment.

| Car insurance | All situations depending on the main types of insurance | Full or partial refund |

| Compensation under CASCO and OSAGO | Compensation for material damage | Repairs at a technical center or service station, funds for repairs, compensation for theft |

If the company does not pay insurance under the MTPL agreement, you will have to take certain actions to ensure that the terms of your insurance contract are met and compensation is paid.

As noted earlier, the ideal option is to immediately contact a lawyer to obtain the necessary advice.

A specialist will help resolve this issue as efficiently as possible, based on your specific situation and conditions, help you draw up a claim or claim and sue the insurance company to recover material compensation and other losses, if necessary.

At the first stage you need to understand:

- Is it legal for the company to refuse this or that payment?

- Have you submitted all the necessary documents regarding the insured event (for example, if the policy is lost, you need to take a duplicate).

- Has the damage caused during the incident been accurately assessed?

Refusal under compulsory motor liability insurance can be either for reasons contrived by the insurer or for legal reasons.

The main condition that must be met for payment is that civil liability can only occur when using the vehicle specified in the policy. According to the Civil Code of the Russian Federation, the one who caused the harm must compensate it in full.

But car owners are not obliged to compensate for damage caused in cases of force majeure or the intent of the injured party. In all other cases, civil liability occurs, which is insured by the MTPL policy.

If the victim himself contributed to the harm, increasing its size, for example, when establishing mutual guilt of the drivers, then the amount of compensation is reduced taking into account the guilt of each party. Mutual guilt is one of the reasons for refusal of payments under compulsory motor liability insurance.

Let's look at the most common reasons why compensation may not be paid:

- Incomplete list of documents provided by the victim (the list of required documents is specified in clause 44 of the MTPL Rules);

- refusal to conduct inspection and examination;

- inability to establish the circumstances and causes of the accident;

- refusal of direct compensation for losses;

- when registering an accident according to the European protocol.

If, when writing an application for compensation, you did not provide the necessary documents or did not provide the car for inspection, and you were refused payment, then in this case you are to blame. But if you have done everything according to the law, and payment is still refused, then you need to go to court.

conclusions

From all the information described, we can draw a conclusion with several tips that will help you receive payment under compulsory motor liability insurance:

- Notify insurers of the occurrence of an insured event as soon as possible. The further success of the proceedings largely depends on your efficiency.

- Collect the most complete list of documents and evidence that will help you win your case. Don't neglect witnesses or photographs.

- Always make sure that the insurer receives the documents you send. Take them in person against signature or send them by registered mail with confirmation of receipt.

- Use only trusted independent appraisers. Many insurers are in cahoots with inspection companies. As a result, such a “dummy” expert will underestimate the cost of losses.

- If the car is under warranty, and the insurer, through its service center, offers to supply third-party parts, do not agree. This may be a reason to remove the car from warranty.

- Be sure to take an interest in the progress of the business. If deadlines are missed, immediately file complaints with various authorities, supporting them with supporting documents.

- When going to court, be sure to keep receipts that show legal expenses. These expenses will be reimbursed if you win the case.

The contract with the insurance company sometimes contains a clause that in controversial situations, issues are resolved without court intervention. This is an illegal clause, since you can always appeal the insurer’s decision in court.

Now you know what to do if the insurance company does not pay money under compulsory motor liability insurance. The best outcome is to resolve the issues out of court. You should go to court if you are fully confident that the actions of the insurance company are unlawful or the amount of compensation is not appropriate.

Catalog of insurance companies in Russia

By following the link , you can familiarize yourself with the catalog of insurance companies in the Russian Federation offering compulsory motor vehicle insurance services. Description of organizations, current financial indicators, ratings, reviews and other information. If you have already had a positive or negative experience with compulsory motor liability insurance of any insurance company, leave your feedback. Thank you!

Link again. Also, be sure to write your comment below. What do you think about the topic of this material? Or maybe you have questions? Ask!

New law on claims in case of refusal to pay under compulsory motor liability insurance

In the field of motor third party liability insurance, there are a lot of not only different practices, but also changes that are trying to somehow improve things in the MTPL market or “patch” some “holes” in the law.

The last significant amendment to the Law on Compulsory Motor Liability Insurance, designed to improve the situation in the field of insurance, was the introduction of the institution of financial ombudsman as a new pre-trial stage of proceedings. As conceived by legislators, the financial ombudsman was supposed to become a kind of shield in front of the judicial system and with his decisions to protect the courts from a large number of claims against insurers under compulsory motor liability insurance, including those with illegal refusals of payments.

These amendments came into force and are mandatory for all victims from June 1, 2021. Article 16.1 of the Law on Compulsory Motor Liability Insurance was amended, in which a mention appeared of the Federal Law on the Financial Ombudsman and the observance of the mandatory pre-trial procedure specified in these two documents.

What procedure must be followed at the moment when appealing against the actions of the insurer?

- First of all, you need to receive from the insurance company a reasoned written refusal to pay compulsory motor liability insurance, or wait until the insurer has expired the statutory period of 20 days for payment or issuing a referral for repairs.

- The next step is to submit a statement of disagreement to the insurance company.

- After receiving another refusal or partial fulfillment of your demands, or the deadline for a response has expired, the victim turns to the financial ombudsman and submits the same demands that were submitted to the Investigative Committee, but were not satisfied.

- But after all this, the only thing you can do is go to court.

Let's compare the existing and previous procedures for appealing an insurance company's refusal:

Changes in the law On Compulsory Motor Liability Insurance on the procedure for appealing an insurance company's refusal

| WAS | BECAME |

| The victim receives a refusal from the insurer for insurance compensation or waits 20 days until the deadline for payment or issuance of a referral to a service station expires. | There have been no changes; the victim is also waiting for action from the insurance company. |

| Submitting a claim to the insurance company, in free form, with the attachment of an independent examination, if it was carried out by the victim. Submitted by mail or handed to the insurer with a mark. | Submitting a statement of disagreement to the insurer in an approved form or in a free form. It is submitted in the form of an electronic document or in paper form by mail or with a stamp. |

| Filing a claim in court | Submitting an application to the financial ombudsman, electronically, through the official website of the ombudsman or by mail in paper form. After receiving the decision of the commissioner, the refusal to consider or the expiration of the period for a response, the victim goes to court. |

It is important to pay attention to the timing of both the submission of all these applications and the timing of their consideration. Previously, the period for consideration of your claim was 10 calendar days, but now, if you submit a statement of disagreement electronically using a standard form and no more than 180 days have passed since the insurer violated your rights, then 15 working days, and in all other cases 30 days.

Then the financial ombudsman will consider your application within 15 working days from the date of receipt, but may extend this period if he decides that an examination is necessary.

Briefly, to summarize, we can conclude that there are more pieces of paper, time is dragging on, but the number of cases in the courts has not decreased.