Is it possible to sign up for an OSAGO policy online?

3.1 (61.25%) 16 vote[s]

A compulsory MTPL insurance policy can be issued not only for the owner of the car, but also for all persons who will be allowed to drive the vehicle. You can enter either a specific person or get unlimited access, but the cost of insurance will vary significantly. If you need to add an additional driver to your insurance, and you want to do it quickly, then today most services can be obtained using online access. Accordingly, the question arises: is it possible to make changes to the compulsory insurance policy, and to what extent is this function available online?

Why do you need to include other people in your insurance?

The desired rule, which states that the person you trust to drive your own “iron horse” must be included in your insurance policy, appeared relatively recently. Previously, the transfer of a car for use had to be accompanied by the execution of a notarized power of attorney, which stated that the owner of the car allows such and such a citizen to drive his car freely.

However, the required travel arrangements were abolished. Now, in order to legally drive the car of parents, children, friends, and so on, you need to fulfill only two conditions:

- take out an MTPL insurance policy;

- include in the documents the person you plan to entrust the car to.

By the way, it will not be possible to indicate anyone on the required paper. Drivers potentially taking over control of the car from you are subject to a minimum list of requirements:

- having a driver's license;

- coming of age.

As for the degree of intimacy between the owner of the machine and its third-party user, there are no restrictions. The second driver can be:

- children;

- parents;

- grandchildren;

- grandparents;

- friends and the like.

However, there are no legal restrictions regarding adding a complete stranger to your insurance; however, you yourself are unlikely to do this, since if there is a name on the insurance policy, a person can freely use your car, and even leave the city in it.

To a greater extent, it is the relatives who are puzzled by the procedure for adding an additional person to the insurance. For example, a grandfather wants to give his old car to his grandson, however, he doubts his complete prudence. As a result, it takes out insurance and adds the offspring to it, still retaining its status as the owner of the car.

How to add a driver to the policy?

Under no circumstances should you do this on your own. The policy form will be declared invalid, and you will not be able to do this, since when applying for insurance, a dash is placed in the empty lines of the table of registered drivers.

In order to include the driver in the insurance, in 2021 you will have to visit the office of the insurance company. This must be done by the policyholder (the one who is indicated in the corresponding column of the MTPL policy and who insured the car, not to be confused with the owner - these can be different persons) together with the person being added (second, third, and so on).

The first one needs to have a passport with him, the second one needs a driver’s license.

Something else useful for you:

- What documents need to be changed when changing your last name?

- New MTPL tariffs in 2021 – increase in insurance prices in the tables

- How much more expensive will OSAGO insurance be after an accident?

How is the cost of a policy calculated in 2021?

The main advantage of an online calculator is the ability to compare the cost of insurance from several insurance companies. Why, in 2021, can the price of a policy with the same data differ so much from different insurers?

The answer to this question lies in the base rate, the corridor of which is set by the Central Bank of the Russian Federation. Insurance companies may, at their discretion, apply a base rate within this band to their clients.

In 2021, the minimum base rate for passenger cars for individuals is 2,471 rubles , and the maximum is 5,436 rubles . Thus, in theory, the cost of compulsory motor liability insurance in different companies for the same drivers, owner and car can differ by more than 2 times.

Different types of vehicles have their own base rate limit ranges. They can be most clearly presented in the table:

| Vehicle | Base rate (minimum) | Base rate (maximum) |

| Passenger cars (for legal entities) | RUB 1,646 | RUR 3,493 |

| Passenger cars (for individuals and individual entrepreneurs) | RUB 2,471 | RUR 5,436 |

| Motorcycles, mopeds and ATVs | 625 RUR | RUB 1,548 |

| Passenger taxis | RUB 2,877 | RUB 9,619 |

| Trucks (<= 16 tons) | RUR 2,246 | RUB 6,064 |

| Trucks (> 16 tons) | RUB 3,382 | RUB 9,131 |

| Route taxis | RUR 3,905 | RUB 7,399 |

| Trolleybuses | RUB 2,134 | RUR 4,044 |

| Buses (<= 16 seats) | RUB 2,134 | RUB 4,165 |

| Buses (> 16 seats) | RUB 2,667 | RUR 5,205 |

| Trams | RUB 1,331 | RUB 2,521 |

| Tractors, road construction and other equipment | 872 RUR | RUB 1,952 |

In addition to the base rate, the increase or decrease in the cost of the MTPL policy in 2021 is affected by adjustment factors:

- KBM - accident-free driving coefficient.

- KVS - coefficient of age and experience of drivers.

- — territorial coefficient.

- — vehicle power factor.

- — is the number of drivers allowed to drive a vehicle limited?

- - duration of insurance.

- — duration of insurance for foreign vehicles.

Agree, it is quite difficult to independently calculate the current policy price taking into account all the coefficients, and given the fact that policyholders do not know what base rate will be applied to them, it becomes completely impossible. The OSAGO online calculator solves this problem, as it takes into account the current base rates of companies and the current values of coefficients for 2021.

You can find out more about all values of MTPL coefficients in 2021 on our website.

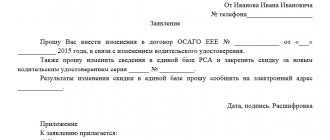

How is the procedure for making changes to the insurance policy carried out?

Insurance company employees give you a form to fill out: you need to fill out all the fields correctly and accurately, as for the new driver. Relevant copies of documents are attached to the form.

Based on the application of the vehicle owner, an additional agreement to the current insurance policy is drawn up. After the additional agreement has been printed, you need to carefully check all the data, especially the full name, driver’s license number and the driver’s date of birth, which was just written down. Any mistakes may lead to unpleasant situations in the future both with traffic police officers and with the insurance company.

For such services, the insurance company may require a financial reward: depending on the driver’s driving experience, which will be specified in the additional agreement (the more driving experience, the cheaper this procedure will cost).

OSAGO is a protection and guarantee of the safety of the car owner, so you need to include someone in the policy very carefully ; it is best to consult in advance with the employees of the insurance company where the client is served. If a permanent insurance company offers unfavorable conditions in a particular case, you can always compare similar offers on the insurance market, since the choice of offers is quite huge.

Procedure for entering data

The process of entering information about an additional driver takes place directly at the office of the insurance company that issued the current insurance policy. The completed application by the vehicle owner is subject to verification by company employees. When the application is reviewed and a positive decision is made, the following documents are issued:

- An insurance document that contains new information added.

- A document confirming payment of the cost for entering new data.

- A reminder for drivers about the civil liability insurance procedure.

- Bank, which is filled out in case of involvement in an accident (two copies).

Attention! The procedure does not involve payment for the services of insurance company employees. Requirements to pay for the actions of the insurance company can be regarded as grounds for contacting supervisory services with a complaint.

When should a driver be included in OSAGO?

Article 1079 of the Civil Code of the Russian Federation states that responsibility for the vehicle falls entirely on the shoulders of its owner. By concluding an MTPL agreement with an insurance company, a motorist can claim compensation for damage caused to his car as a result of an accident. This is only possible in insurance cases, that is, those circumstances that were specified in the contract. If, at the time of the traffic accident, the car was driven by a person who was not included in the compulsory motor liability insurance policy, the insurer may not compensate for the resulting material damage.

Thus, if other persons besides the owner can use the car, their data must be included in the insurance policy. This rule has only one exception: if the contract does not provide for restrictions on the number of persons allowed to drive a vehicle, then entering information about each driver is not required.

The insurance contract often names several drivers. The cost of processing the document in this case will depend on the driver with the highest coefficient. If the car owner subsequently wants to add new data to the policy, he will not have to pay extra for this.

What documents do you need to take with you?

Of course, before coming to the insurer’s office, you need to prepare and collect a package of documents that you need to take with you. However, this process will not take much of your time, since the insurance company requires information from:

- your previously issued insurance policy;

- passport belonging to the owner of the car;

- driver's license of the person included in the policy;

- data from the main document of a citizen of the Russian Federation belonging to the new driver (passport).

In addition, it is most likely that when you visit the office, you will be asked to complete an application for the requested change. In it you will need to express your desire to make changes to the MTPL insurance policy.

What is required to edit the policy

To register a new driver in OSAGO, you need the policyholder’s passport, the original policy with the insurance contract, and documents for the car. You will also need the new driver's driver's license. The passport and personal presence of the person you want to include in the insurance are not required.

Also, if you change the terms of the policy, you will need to pay an additional insurance premium. It will be calculated based on the driver's characteristics. The lower the age, length of service and KBM, the higher the bonus will be.

How to save money when adding a driver to your insurance policy

Insurance companies provide their clients with flexible discount systems, and a certificate of break-even driving of a vehicle also plays an important role when applying for a service (such a certificate is issued by the insurance company where the driver is served). if the client is a regular of a particular insurance company, then, of course, only having an insurance policy will be enough (insurance agents will find the rest of the data in the company’s databases).

If the driver who is included in the insurance policy is a client of another insurance company and there are no supporting documents about his accident-free driving, then the insurance company may refuse the discount (the right to receive it is automatically lost).

The size of the discount for the client is calculated according to the accident-free experience (the driver’s class is determined).

- 1 year of driving without accidents – 4th class – 5% discount.

- 2 years of driving without accidents – 5th class – 10% discount.

- 3 years of accident-free driving – 6th grade – 15% discount.

- 4 years of accident-free driving – 7th grade – 20% discount.

- 5 years of accident-free driving – 8th grade – 25% discount, etc.

Registering a driver with MTPL is a responsible procedure and requires not only money, but also attention to calculations and registration. By adding another driver to your insurance policy, legal and financial responsibility is automatically shared, and if an accident occurs, the person responsible should actually be held accountable for the incident.

How much does it cost to include an experienced driver in your insurance?

In this case, the magnitude of the coefficient also depends on age. And here the rule “the older, the cheaper” also applies. Thus, the minimum payment is made by experienced drivers over 59 years of age. If over the past three years a citizen has managed to avoid accidents, he will receive a reduction factor of 0.93.

Let's look at the cost using an example. With a base rate of 3,000 rubles, a regional coefficient of 1.2 and a power factor of 1.6, such a driver will have to pay 5,356 rubles. For comparison, a citizen under 22 years of age and with 3 years of experience will need to deposit at least 9,500 rubles.

To register a driver with experience in OSAGO, the owner of the car needs to pay the difference with the initial cost of the contract.

If you study the innovations for 2021 in detail, an attempt to reduce the cost of insurance for experienced drivers becomes obvious. The size of the benefit in this case is directly proportional to the driving experience. Newcomers have nothing to rejoice at - for them the surcharge has only increased.

What determines the cost of making additional payments? driver

All insurance companies must have the same cost. How much it will cost to add a person to your MTPL policy depends on:

driving experience (less/more than 3 years);

age (under 22 years old/over 22 years old);

individual accident rate (other names: KBM, “Bonus-malus”).

Based on driver data, a coefficient is calculated from 1 (over 22 years old, driving for 3 years, accident-free driving for 5 years) to 1.8 (under 22 years old, with less than 3 years of experience). It is the coefficient that determines the cost of signing up for compulsory motor liability insurance. The discount for accident-free driving is checked against the general database of insurance companies. The company is not obliged to provide it, but is interested in this - otherwise you will buy insurance from another insurer, so when purchasing a policy you are usually given a maximum discount.

Cost of the procedure

Do I have to pay for changes to my insurance? If you want to add a new driver, then in most cases you have to pay extra. This is due to the fact that the risks of driving a car by a new driver increase, especially if his experience or past history is worse than that of the existing policyholder. The new calculation will now take into account not only the data of the current owner and the car, but also the new driver, and to be more precise, the coefficient of experience and age, as well as the bonus-malus coefficient (accident-free driving).

- If the driver is less than 22 years old and has less than 3 years of experience, then a coefficient of 1.8 is applied to this formula, which means that the cost of insurance will increase by 80%, that is, almost twice.

- If the driver is already 22 years old, but has not yet had 3 years of experience, then a coefficient of 1.7 is applied, respectively, the amount of the initial payment must be multiplied by 1.7, the increase will be 70%.

- If the driver is less than 22 years old, but has more than 3 years of experience, then the insurance agent will enter the value 1.6 into the CIC formula, where the increase in price is 60%;

- If the driver is over 22 years old and has more than 3 years of experience, then the cost of the policy remains at the same level, in this case the coefficient is equal to one.

But if the new driver has a bad reputation, namely, in the past he was involved in an accident with violations, then the cost of insurance will be adjusted depending on the value of the BMR (bonus-malus), starting from the value in the unified RSA database.

It is important to understand that the established coefficients will be multiplied by the initial cost of insurance, and then recalculated taking into account the remaining days until the end of its term. That is, for example, initially you paid 4,920 rubles when registering a policy, after registering a new driver over 22 years of age, but with less than 3 years of experience, the policy price increases by 1.7 and equals 8,364 rubles. But there are 92 days left until the end of the policy, respectively, the cost of additional payment will be: 8364/365*92=2108 rubles. Thus, you will need to pay an additional 2,108 rubles for insurance in a specific case. But it may also be that you don’t need to pay anything at all (if FAC = 1).

How many people can be included in the policy?

According to the law on compulsory motor liability insurance, an unlimited number of drivers can be included in the insurance, despite the fact that on the front side of the policy there are only 5 points in the section “Drivers admitted to driving”.

If you are going to take out unlimited insurance, there will be a dash in the lines indicating additional drivers without a single entry.

How many drivers can I sign up for free?

The procedure for adding a new person to OSAGO is free. Moreover, the number of people entered is not limited. Even though there is a limited number of fields in the policy for drivers, the legislation does not impose limits on the number of persons allowed to drive. If the insurance company complains that they have nowhere to add a person to the insurance, that’s their problem (in practice, they write it on the back of the policy).

Which insurance companies are involved in the calculation?

After filling out the form, the online calculator sends the data in encrypted form using a secure protocol to insurance companies, on whose side the cost is directly calculated. This is how we manage to provide users with accurate prices for compulsory motor liability insurance.

The list of insurance companies involved is quite wide and may be adjusted during 2021.

Also, the number of insurers may differ in different regions of Russia. Almost always, large companies are included in the calculation, such as Rosgosstrakh, Alfastrakhovanie, Tinkoff Insurance, Ingosstrakh, SOGAZ, Soglasie, Yugoria and others.

To calculate the cost of voluntary car insurance, you can use the CASCO calculator.

How to get a discount

Since the discount helps save money on a compulsory motor liability insurance policy, every car enthusiast is interested in receiving it. However, you cannot increase it yourself, or even more so, buy it. The bonus is awarded only to careful motorists who follow traffic rules and are not the culprits of the accident. Every year, such citizens receive a 5% bonus from the state. To receive the maximum bonus of 50%, you must drive your iron friend for 11 years without an accident.

In conclusion, it can be noted that every traffic participant who wants to drive must be insured. You can make changes to a previously purchased MTPL through the office, or independently. It is important to understand that the insurance company has the right to request additional payment. Its size is determined by the current tariff guidelines.

How to calculate the price of driver registration?

So, we already know how much our OSAGO policy costs. This cost is made up of the base rate and odds. Important! Your insurance is calculated based on each driver's worst-case odds (even if they are different).

For example, if 2 people are included in the insurance: aged 25 years and 35 years and with experience of 7 years and 1 year, respectively, then the calculation will be based on the minimum age and minimum experience. However, age and experience are actually one factor; both parameters work in pairs. How exactly, we will clarify below!

We need to understand what parameters are being added to MTPL. If all of his coefficients are higher or equal to the coefficients of already added people, then adding such a driver to the insurance will be absolutely free. Also, the price is not affected by the period for which you sign up a person - be it for a month or for the whole year.

Let's look at how the price of insurance is affected by the included driver, depending on each of the 2 coefficients we need!

Age and experience of the new driver

There are 56 values for this parameter after recent changes.

As you can see, the younger the added driver and the less experience he has, the more expensive it will be for us to add him. For beginners without experience, as a rule, it turns out to be very expensive to add (sometimes almost 2 times more expensive than the original cost of insurance).

It is important to know that the cost of adding will not depend on the insurer - it will be the same in different insurance companies, be it Rosgosstrakh, Reso, SOGAZ, VSK, Alfastrakhovanie, Ingosstrakh or another - even a little-known company. There is a basic rate for everyone, period.

But let's look at examples!

Example No. 2: we enter a newcomer without experience

Given : 1 person is included in the current policy: his age is 26 years, and his length of service is 5 years (coefficient 1). The initial price of insurance is 6,000 rubles.

Required : include a young novice driver aged 18 years and zero experience in the insurance.

How much will it cost : a coefficient of 1.87 will be applied to the second person - the highest. Therefore, it will be expensive to include it. But it would be a misconception to expect that it is exactly 87% more expensive. The fact is that the calculation is cumulative - the coefficients are applied to the base rate one by one. First territorial, then KBM, then age and length of service, and then the rest. That is, the calculation is not rigid.

In our case, the cost of such a policy with a newly registered novice driver without experience will cost about 3500-4500 rubles. But this is not the biggest price, because KBM is applied before age and length of service, so it has a greater influence on the final calculation. With a different initial insurance price and the same coefficients indicated by us, you can calculate the cost as a percentage.

Example No. 1: we enter a driver with experience

Given : 2 people are included in the current insurance: 21 years old and 1 year of experience, 25 years of age and 3 years of experience. The cost of the policy was initially 6,000 rubles (the maximum coefficient of 1.8 was applied).

Required : add a driver with 15 years of experience and 30 years of age to the MTPL insurance.

How much will it cost : free (with the same or better KBM), since the new person being entered is with experience, a coefficient of 1 will be applied to him, and the policy will be calculated according to the worst driver - that is, a 21-year-old with 1 year of experience.

Driver accident-free

As we have already noted, the bonus-malus coefficient has a much greater impact on the cost of enrolling a person in auto insurance. Thus, a driver with the maximum KBM rate may cost you 2(!) times more than the original price of OSAGO. It's creepy, but it's a fact!

The fact is that the range of bonus-malus bets is from 0.5 to 2.45. You can read more about the rates and how much the policy becomes more expensive after an accident where you are at fault in a special article about increasing the CBM. You can also check your KBM and the registered driver according to our instructions. KBM is also included in the policy when it is sold (similar to age and length of service, the worst coefficient is taken into account).

Example No. 1: we enter the worst culprit of the accident

And we will start with the most disgusting example with the maximum price for adding a driver.

Given : the initial cost of the policy is 2800 rubles - everything is at the minimum: registered with experience with a low-power car and a minimum KBM of 0.5.

Changes to OSAGO

Changes as of August 24, 2021:

- Individualization of tariffs. Now insurers will be able to set individual rates for different drivers within the same territory. The main factor that insurance companies will take into account when setting the tariff is the presence of gross traffic violations. Companies may also take into account other circumstances at their discretion.

- Tariff corridors for all types of vehicles have been expanded. For example, the corridor for individuals' cars has been expanded by 10% in both directions.

- The age and length of service coefficients have changed. For young drivers the price has increased slightly, for experienced drivers it has decreased.

- The cost of a policy without restrictions on drivers has increased. KO increased from 1.87 to 1.94.

- Regional coefficients have changed.

- The trailer coefficient has been cancelled. At the discretion of the insurance company, the presence of a trailer can now be factored into the base rate.

Changes from January 9, 2021:

- Basic tariffs have changed. The range has become wider. Let us recall that basic tariffs are set as a range for different types of vehicles. Coefficients are applied to the base rate and thus the final cost of the policy is calculated. Insurance companies can set their tariff within the corridor.

- The KBM will be installed once a year – on April 1. Until this day, it was set on the date the policy was issued.

- The coefficient for an unlimited number of drivers (KO) has increased from 1.8 to 1.87. The CR ratio for a legal entity remained unchanged – 1.8

- The number of driver categories for determining the KVS (age-experience) coefficient has been increased to 58. Each category has its own coefficient.

Amendments as of September 25, 2021:

- Now you must contact your insurance company for compensation, regardless of the number of participants in the accident. This is called “direct damages.” Previously, this option was possible only when there were two participants in the accident.

Changes from October 1, 2015:

- It is now possible to purchase

an electronic MTPL policy via the Internet. Only novice drivers, information about whom is not yet in the database of the Russian Union of Motor Insurers, will not be able to use this service. Check the possibility of providing this service with a specific insurance company.

New as of July 1, 2015:

- Car owners have the opportunity to renew

MTPL policies with their insurance company electronically via the Internet. To purchase a new policy, you must still contact the office of the insurance company.

A set of amendments regarding payments for harm to life and health dated April 1, 2015:

- The limit of payments for the life and health of victims increases from 160,000 to 500,000 rubles.

- The procedure for confirming the fact of injury to health in an accident and the procedure for receiving payment under compulsory motor liability insurance are being simplified.

Tariff changes from April 12, 2015:

- An increase in the base tariff by 40% and an expansion of the tariff corridor to 20 percentage points, so the increase was 40-60%.

- Changes in territorial coefficients both up and down.

The coefficients have been increased: Adygea, Murmansk region, Amur region, Mari El Republic, Voronezh region, Ulyanovsk region, Kamchatka region, Chelyabinsk region, Kurgan region, Chuvashia, MordoviaThe coefficients have been reduced: Leningrad region, Baikonur, Magadan region, Dagestan, Republic of Sakha (Yakutia), Jewish Autonomous Region, Republic of Tyva, Trans-Baikal Territory, Chechen Republic, Ingushetia, Chukotka Autonomous Okrug

- October 11, 2014

A decree of the Government of the Russian Federation has been adopted regulating the new procedure for calculating the compulsory motor liability insurance policy:

- The emergence of a tariff corridor, which allows insurers to deviate from the base tariff within certain limits. Thus, the cost of the policy in different insurance companies can now vary within small limits.

- Increase in base rates for all types of vehicles by 25-30%.

- Increase in payments under the MTPL policy from 120,000 to 400,000 rubles

- There is now an opportunity to send your car for repairs under the MTPL policy

- Expansion of the Europrotocol to 50,000 rubles

What happens if you don’t take out insurance according to all the rules?

Every resident of our country knows about a certain folk phenomenon that is almost magical in nature - the Russian “maybe”. This is what hundreds of drivers are guided by when entrusting their car to a friend, child, parent, etc. Yes, it is at this moment that he thinks “maybe it will blow through”!

However, as practice shows, mere hope for a successful outcome is not enough for it to actually turn out to be such. Typically, drivers who are not included in the insurance of the car owner find themselves in various kinds of troubles. These are the consequences that await them in each of them.

Consequence #1. In a sense, the easiest and safest consequence for illegally driving a car is a fine of 500 Russian rubles. It is this amount that punishes the laziness and greed of a car owner who did not want to take out insurance for his loved one according to all the rules.

It should also be mentioned that the fine itself, of course, is small, however, the very mention of your mistake will be stored in the databases of the traffic police and the insurance company, which ultimately may negatively affect other processes ongoing in your life.

Consequence No. 2. If a driver who is not registered in the policy while driving your car gets into a traffic accident, the consequences will be much more serious. The insurance company servicing your car will refuse to cover damage caused to vehicles, which means that the unlucky driver will have to cover all the costs out of his own pocket.

The required amount may be so impressive that you will not be glad that you initially did not pay additional funds for making changes to the policy

Is it possible to add a second driver to the document without his presence?

The modern pace of life imposes corresponding obligations on citizens. Unfortunately, if it is necessary to urgently renew an insurance policy for a car, and the second driver is busy, many citizens think that the procedure will have to be postponed, because both managers of the “iron horse” must participate in it.

However, in reality this is a simple misconception. By law, you have every right to amend your policy by adding a driving permit for another driver, without the presence of that person.

You can add another driver to your insurance yourself

If you issue an electronic policy, in fact, you yourself can be anywhere, since in this case you only need:

- information from the documents listed in the sections above;

- making an additional payment for driving insurance for the second driver.

In the case of receiving a paper original document, the presence of only one person is required - the direct owner of the car, regarding whose insurance the changes are made. You will also need to take with you the documents of the person who will become the second driver of the car you are looking for.

The opposite situations can also occur, when the owner of the car does not have time, but his friend, on the contrary, has it. In this case, you need to do the following:

- issue a power of attorney in the name of the second driver, implying the performance of certain actions on behalf of the car owner (for example, signing papers, etc.);

- notarize the required document;

- send the second driver to deal with the task alone.

The option with a power of attorney is very convenient, however, its execution takes approximately the same amount of time as adding new nuances to the policy, therefore, from a strategic point of view, unless in the future you are going to entrust similar things to your friend or family member, it is easier to go straight away to the insurance company.

Is it possible to add a driver to insurance online?

If you have a valid MTPL policy and you need to add a new driver there, many decide to do this in the same way as applying for an electronic policy - through the insurance company’s website, that is, leaving an application online. In fact, this can be done. If you register on the site or log in with your details, your current MTPL insurance will be displayed in your personal account. You can click on it and view the completed data during initial registration. Where there is a column with these drivers, you can make adjustments to the insurance, but this action is considered illegal.

Very important! Under no circumstances try to make changes to your insurance through your personal account on the insurance company’s website; such actions are considered illegal, even if you are technically able to do so. You can change the data in the policy in accordance with legislative acts only by personally contacting the insurance company office.

Why does this question remain relevant? Until recently, such a solution was actually implemented in practice. Those companies that are actively engaged in new developments that will improve customer service have introduced the function of online changing insurance data, but a few weeks later the state prohibited such an action, including new persons enrolled in insurance on their own. Only a company employee can change the policy data, enter it into the unified RSA database and endorse it with a signature and seal. And since not everyone has yet been notified of the cancellation of this opportunity, they are trying to add a new driver without the knowledge of the insurance company.

Thus, it is impossible and strictly prohibited to independently enter the data of another driver into the MTPL insurance policy. Such actions may result in criminal liability and will be considered fraud. Therefore, do not listen to the advice of friends, acquaintances, or do not put into practice your guesses about the new online opportunity to make changes to your insurance; only personally contact the insurance company branch with the necessary package of documents.

Alternative options

There is an alternative insurance option in which there is no need to enroll a new driver. Anyone can use it to legally drive a vehicle. This is the so-called MTPL policy that is unlimited in scope of persons.

Such a policy usually costs twice as much as usual and you will have to pay an average of at least 15 thousand rubles for it. However, such a policy will eliminate the need to spend time each time adding a new driver or, if there is a frequent need to transfer control to different persons for a short period of time.

When applying for such a policy, you need to be attentive to the form. The differences between a policy with a limited number of insured persons and an unlimited number of insured persons are small but significant.