The Russian Union of Auto Insurers (RUA) launched an Automated Information System (AIS) in 2013. This is a database where information about MTPL contracts is stored (the date the policy was issued, the period of its use, the name of the insurance company, the full name and VU number of the car owner, the registration number and VIN code of the car, the region of residence of the driver and his BMR (bonus-malus coefficient)) . During the period of using MTPL, your life circumstances in your small circle may change. For example, the rights were replaced. Therefore, you need to know how to change data in PCA. In addition, according to the legislative norm, the new details violate the rules of the current agreement (Article 451 of the Civil Code of the Russian Federation).

In what cases does it become necessary to make changes to the MTPL policy?

Amendments to the MTPL policy must be made when any data entered into the unified RSA database changes. A similar need arises in the following cases:

- replacement of a driver's license;

- the need to use the car outside the period noted in the insurance form;

- replacement of a vehicle passport (PTS);

- replacement of the state registration mark;

- change of car owner;

- change of the owner's name and place of residence.

In addition, changes are required if you need to transfer the car to another person for temporary management.

Rules for submitting an application

You must fill out the application to change your data using a ballpoint pen. It is recommended to write legibly, preferably in block letters. In the form, indicate the essence of the request, for example, changed: license, passport, last name, etc. And also write that you are asking to assign the accident-free discount to the updated data. Put the date and signature. The application must be submitted in 2 copies. One form remains with you, with a mark from the Investigative Committee on acceptance of the documents.

What are the dangers of having old data in your insurance?

Dear readers!

Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem, please contact the online consultant form

It's fast and free!

Or call us by phone (24/7):

If you want to find out how to solve your particular problem, call us by phone. It's fast and free!

+7 (495) 980-97-90(ext.589) Moscow,

Moscow region

+8 (812) 449-45-96(ext.928) St. Petersburg,

Leningrad region

+8 (800) 700-99-56 (ext. 590) Regions

(free call for all regions of Russia)

In accordance with paragraph 8 of Art. 15 of the Federal Law “On Compulsory Motor Liability Insurance”, the policyholder must notify the insurer of any changes in personal data.

If the driver does not tell the insurer his phone number, nothing bad will happen. But if amendments are not made when changing the last name, first name, place of registration or certain documents, the driver may face negative consequences.

What else to read:

- My car was scratched in the yard, what should I do?

- Europrotocol 2021

- How to get money instead of repairs under compulsory motor liability insurance: a detailed review

Thus, when checking documentation, traffic police officers may have many questions as to why the data in the car owner’s documents does not correspond to the information in his insurance policy. In this case, representatives of the traffic police have the right to invalidate the policy and issue a ruling regarding violation of civil liability.

This is not the worst consequence. The situation will be critical if an insured event occurs. No insurer will agree to compensate for losses under a policy whose data is untrue. Therefore, it is important that all changes are made in a timely manner - this will help save time, money and nerves.

Typical problems when applying for electronic compulsory motor liability insurance

As with many other innovations, a number of problems have arisen with electronic policies. They are associated with both technical and commercial reasons.

- Problems when registering a document through the website. The number of motorists who wished to obtain a policy in this way exceeded the capabilities of the technical infrastructure. The problem is related not only to the overload of the servers of the insurance companies themselves, but also to the inability to service such a number of requests coming to the database of the RSA - Russian Union of Auto Insurers (information about each insured person is stored by this association).

- Lack of information about vehicle registration in the database. One of the significant problems is the difficulty in exchanging data between the traffic police and the RSA. If the transfer of updated data occurs with errors, then there may simply be no information about the existence of the client’s vehicle.

- Lack of technical inspection data. One of the conditions for obtaining a policy is a valid diagnostic card. Data about it may also not be available on the RSA server and the system will not allow you to issue compulsory motor liability insurance.

- Inability to apply a reduction factor for accident-free driving. If the policyholder does not cause an accident, he is given a discount that accumulates every year. It can reach half the cost of the policy. For some reason the coefficient cannot be applied.

- Regional restrictions. Insurers provide the opportunity to purchase a digital policy only to residents of certain cities. They explain this by the “toxicity” of a number of regions. By this, companies understand the prevalence of “fraudulent schemes” and the unprofitability of activities in such territories.

- Problems for non-residents. These difficulties are associated with regional restrictions. If a citizen lives in the capital, but is registered in another city, it will not be possible to obtain a policy. In some cases, an absurd “verification” of the client is provided, lasting up to 30 days.

Some actions of insurers specifically encourage clients to refuse to issue electronic MTPL:

- reference to a certain limit regarding the number of digital policies issued per day or month;

- generating passwords containing characters in Cyrillic and Latin simultaneously;

- deliberately limiting the methods of payment for the policy;

- charging fees for transferring funds.

All of the above is intended to force the user to come to the office, where he will be forced to purchase insurance along with the imposed services. Insurance companies are trying in every possible way to increase the margins of insurance, which in terms of compulsory motor liability insurance in some regions of the country is simply unprofitable due to the activities of auto lawyers. It will not be possible to condition the possibility of issuing an electronic policy on the purchase of other company products on the website.

Such a policy violates the law, and the corresponding requirements on the company’s portal will become irrefutable evidence of its guilt. Such actions of insurers often force them to file complaints against them with Rospotrebnadzor and the Bank of Russia.

Important: Do not hesitate to complain to insurance companies. In practice, the attitude towards the client after receiving money is so unpleasant for most of them that you need to have the proper restraint and be able to correctly and reasonably file a complaint.

Why is it important to report all changes?

Failure to make timely changes to the policy, as already mentioned, may result in refusal of compensation and invalidation of the policy.

Another negative point is the loss of discounts that drivers receive for accident-free driving. Quite often it happens that a client, having replaced his rights, does not notify the company about this, and as a result, all his bonuses are reset. Therefore, with any changes, it is important to make them timely in the policy. This will prevent a number of problems in the future.

What is needed to make changes to OSAGO: a guide to action

There is nothing difficult about making changes to your insurance policy. This procedure includes several basic steps.

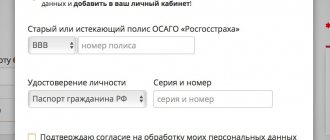

Statement

First you need to visit the insurer's office. You will need to write a statement. The form will be issued by a company representative.

You need to contact specifically the insurance company where you took out the policy.

It is recommended that you first call the insurer and clarify whether the employees will be able to make the necessary amendments to the insurance. This is due to the fact that many organizations make amendments only at their central offices.

Collection and submission of documents

The list of documents that insurance companies require to make changes includes:

- Policyholder's passport. If his interests are represented by another person, he must also present his passport and notarized power of attorney.

- Contract form received when applying for insurance. If the policy was issued electronically, you need to print out a copy of the agreement with the original signature and show it to the specialist.

- Document confirming the changes. Depends on the reason for the application: it could be a document confirming a change of surname, a new driver’s license, and so on.

Additionally, the insurer may ask the policyholder to present the car.

Getting a new policy

After the insurance company employee accepts the application with documents, he will make the appropriate amendments and issue a new policy. The new form will contain the number of the previously received policy.

According to the rules, the insurer can make changes on the back of the insurance form. In this case, a note about special conditions is placed on it, new information is entered, and the full name, position and signature of an employee of the insurance company are added. The date and time are indicated.

If the interests of the policyholder are represented by another person, a power of attorney must be presented. If the owner does not act as the policyholder under the contract, he also cannot make amendments without a power of attorney.

The power of attorney is drawn up by a notary. It indicates the details of the policyholder and the authorized person, the actions that the latter can perform and the validity period. Some insurers accommodate the client halfway and replace the policy with a regular power of attorney filled out by hand. It is better to first check with its representatives whether the insurance company will accept such a power of attorney.

Complaint to RSA

In general, when it comes to compulsory motor liability insurance, you must remain extremely careful and double-check the information entered by insurance agents several times. If the situation with the loss of the bonus has already occurred, then write a statement to the insurance company with a request to restore the KBM.

If the request is ignored, write a complaint to the RSA or the Central Bank. The official portals of both organizations have complaint forms that can be filled out and submitted remotely.

How to make changes to e-OSAGO

If the policy was purchased online, the procedure for making changes to it will be similar. But some companies give you the opportunity to make changes online. This is done on the website of your insurance company through your personal account.

The policyholder needs to make the necessary amendments to the electronic insurance. Then he will receive a new document electronically. Sometimes the insurer may send a justified refusal to make amendments. Then the car owner will have to visit the office of the insurance company, where he will receive a new paper policy. Its validity period will not change.

How to restore KBM online

If the insurer refuses to return your lost accident-free rating, and you don’t have time to litigate, you can contact the popular commercial online service KBMka. For 530 rub. The company’s specialists help reduce the BMF to a minimum level (0.5). To contact, follow the instructions:

- Open the website kbmka.ru.

- Fill in your full name, date of birth, series and ID number. Click "Check KBM".

- After checking, the “Restore KBM” prompt will appear. Click it.

- The “Fill out an application” section will open.

- Upload all MTPL policies, pay the invoice and click “Submit”.

Specialists will submit an application to the RSA to restore the KBM on your behalf. Expect results within 1-3 days (maximum 7 days). If the decision is positive, you will receive an SMS informing you that your bonus-malus ratio will be reduced. If the rating cannot be restored or it decreases slightly, then kbmka will return the entire amount of money to you.

If you have replaced your license, passport, vehicle registration number or PTS, then immediately notify the insurer. He will make changes to the RSA database. It is not recommended to ignore this condition. Since the next MTPL policy will be issued to you without the KBM cumulative discount.

Typical situations

The changes that need to be made to compulsory motor insurance differ, so it is worth considering each typical case separately.

Adding a new driver

This is the most common amendment that drivers apply to the insurance company. In addition to the documents already mentioned, you must present the driver's license, which must be included in the insurance.

No more than five drivers can be included in the policy. If the contract already includes this quantity, then to add another person you need to write someone out. But there is also such a condition as “an unlimited number of persons admitted to management.”

Adding a new driver may require additional payment. It is calculated automatically. Additional payment is required in the following cases:

- The discount amount based on the RSA database is less than that used to form the initial calculation.

- The new driver’s age is less than 22 years or the driver’s experience is less than 3 years, provided that these indicators are higher for previously registered participants.

Changing the validity period

By law, you can buy insurance with a limited period of use (from 3 months). If the driver decides to increase this period, such changes must be made to the policy. When renewing, you must pay the difference for the required insurance period. The policy will indicate the new date.

These changes must be made before the insurance period specified on the form ends.

Replacement of driver's license

When replacing your driver's license, it is also important to make timely changes to your insurance, since the license number is indicated on the form. In addition, this is necessary to maintain a discount for accident-free driving. Additional documents will require a new ID.

At the same time, the number of the old certificate is most often indicated on the back of the new license. In this case, the driver should not encounter problems either when checking the papers by representatives of the traffic police, or during further communication with the insurer. However, in some cases, there may be quibbles that the current rights according to the number do not coincide with those specified in the policy, so it is still recommended to make changes. This is especially true in cases where the number of the old rights is not indicated on the new ones.

Change of place of residence

When changing registration, you need to contact the insurance company, presenting a document indicating the new place of registration. Usually this is a passport.

At the same time, the amount of the insurance premium can either decrease or increase, since it is influenced by the territory coefficient - CT. That is, either you will have to pay extra, or, on the contrary, part of the premium paid will be returned to you.

CT differs not only in different regions, but also in different cities. Therefore, it is important to promptly inform the insurer about a change of place of registration, even if the territory coefficient does not change.

Replacing PTS

When replacing a vehicle's passport, you must enter the new number and series of the document into the policy. To do this, you must present a new PTS. This procedure is free.

Replacing vehicle license plate

State registration plates are indicated in the insurance policy, so if they change, it is important to record this. This will help prevent problems both with traffic cops and with the insurance company.

Changing the license plate does not equate to replacing the car, so you only need to make changes to the policy, and not change it. If the car has not yet been registered, the license plate will not be entered in the column of the policy intended for this. Once the numbers are received, you need to inform the insurer about this within three days, who will make a note about this in the insurance.

Changes in personal data

The basis for amending the policy is also a change of first or last name. New data must be entered not only into OSAGO, but also into other documents for the car. Therefore, it is recommended to contact the insurer after you have changed your main passport, license, PTS and STS. Then you can immediately change other necessary data.

Some MREO branches require an insurance policy that already contains new personal data. In this case, you need to visit the insurer twice: the first - to change the name or surname in the policy, the second - to provide data on new documents for the car.

In this case, the amount of the insurance premium does not change, so no additional payments are needed.

Aleks261 › Blog › RSA has identified a way to fix KBM

RSA has determined a method for correcting the KBM www.asn-news.ru/news/55574#comment-99106 The bonus-malus coefficient (BM) for compulsory motor liability insurance of car owners for whom there is no payment data in the RSA AIS will be corrected automatically. This follows from the documents available to ASN from the meeting of the presidium of the Russian Union of Auto Insurers (RUA).

Corresponding changes to the rules of professional activity of the RSA were made at a meeting of the presidium of the union on December 15. It is assumed that if a citizen disagrees with the CBM applied to him, the insurer will be able to send a request to the AIS RSA for automatic correction of this coefficient.

During automatic processing, a contract with a minimum BMR of a given car owner will be selected (the driver will be identified by last name, first name, patronymic and date of birth or by identification document number). After defining such a contract, AIS RSA will automatically calculate its BMR for subsequent annual periods. In this case, the new coefficient will be determined by sequentially assigning the best KBM class.

This opportunity will work for car owners who do not have data in the AIS RSA on insurance payments that affect the CBM, it follows from the union’s materials.

As ASN has already reported, complaints about incorrect KBM make up a significant part of all complaints against insurers received by the Bank of Russia. Thus, in the third quarter of 2015, their number doubled compared to the second quarter of the same year: the regulator received 5,063 complaints. Moreover, in the second quarter there were only 2,424 such complaints, and in the first quarter – 753. **************************************** ************************* ******************************** **************************************** Some kind of noodles))) …”It is assumed that if a citizen disagrees with the CBM applied to him, the insurer will be able to send a request to the AIS RSA for automatic correction of this coefficient. During automatic processing, a contract with the minimum BMR of the given car owner will be selected.”…

Insurers themselves reset the BMR and do not enter information into the AIS. What prevents the insurer from correcting the KBM and its chaos in the AIS database? How will RSA process data on contracts if there is no information on contracts in the database? And who will force the insurer to make such requests? And how do we understand that the insurer “will be able” to make such a request, but the policyholder will not be able to? (Apparently they announced a fight against complaints). Again, everything will go in circles - requests will pour in from RSA to insurance companies that do not care about your (Our) KBM.