Information about the owner in the contract

When concluding a CASCO agreement, the owner of the car as a driver may not be included in the policy if insurance is purchased for one of the family members or for a person to whom the car was leased or used free of charge.

If the policyholder is not specified in the contract, then he is not considered a person authorized to drive a car (except in cases with a multidrive policy).

We emphasize that we are talking only about CASCO with a limited number of persons who are given the right to drive a car.

If the policyholder is a legal entity. person, then CASCO is issued for any number of drivers. Accordingly, anyone can drive an insured car.

What happens in the event of an accident if the driver is not included in CASCO insurance?

As mentioned above, the disadvantage of not including a second participant in the traffic is that the insurer will refuse to pay compensation in the event of an accident. However, it is necessary to take into account 2 agreements: OSAGO and CASCO.

As for the mandatory product, if the driver:

- injured, then payment is provided, and it does not matter whether the driver is included in the contract or not;

- the culprit is included in the insurance, then payment is provided to the victim;

- guilty and not allowed to manage, compensation at your own expense.

As for a voluntary contract, the insurance company has the right to legally refuse payment. In this case, it does not matter whether the driver who is not registered under CASCO is the guilty or injured party.

Who can enter the details of the second driver?

Only the policyholder, that is, the one who purchased the CASCO policy, has the right to register the second and other drivers.

But he has the right to issue a power of attorney to another person who will assume the responsibilities of concluding a CASCO agreement and making changes to it.

The power of attorney must be notarized.

It is prohibited to include a second driver in the contract yourself (without notifying the insurance company and drawing up an additional agreement to the CASCO contract).

How much does it cost to add new people to your insurance?

The inclusion of new persons in the policy may increase insurance risks and therefore the insurer has the right to revise the amount of the insurance tariff.

This is done if new persons are young and do not have a driving record, as well as discounts for break-even insurance.

The amount of the surcharge depends on the following factors:

- how many months are left until the insurance period expires;

- number of drivers, their age, driving experience;

- temporary or permanent inclusion of a new driver in the policy.

For calculation, the insurer takes the total cost of CASCO for the year with the required number of drivers. The cost of current single-driver insurance is subtracted from this figure.

The difference is multiplied by the number of days remaining until the end of the insurance period. The resulting figure is divided by the number of days in a year.

On average , the surcharge for a policy for two drivers is usually 5-10% of the contract amount . The less time before the end of the insurance period, the less the additional payment will be.

If there are only a few weeks left before the policy ends, the company may even refuse to add new persons to the insurance.

How much does it cost to add a new driver to the contract?

To include a new person in a voluntary insurance contract, you may need a certain amount of additional payment, which depends on the following factors:

- Age and experience of the new driver . If it is necessary to include in the insurance a motorist with experience that is not inferior to other drivers of this vehicle, then the cost of insurance will practically not change. It’s another matter if the policy needs to include a young motorist with little or no driving experience. In this case, the price of the issue may increase significantly. In this case, applying for multidrive comprehensive insurance will help you save money.

- Duration of the insurance contract . The cost of a reissued policy if there is a month or two left until the end of the insurance contract will be significantly less than if you decide to include another motorist just a few days after purchasing CASCO.

- Insurance period . There are situations when one more person needs to be included in the insurance for a short period, for example, for a vacation or trip abroad. In this case, the losses for the family budget will be insignificant, and insurance protection will protect you from unwanted financial expenses after an insured event.

Don’t want to worry about the safety of your car while a newbie with no experience is driving? After including it in the policy, you are guaranteed financial protection in the event of an insured event.

Is it possible to enter data via the Internet and how to do it?

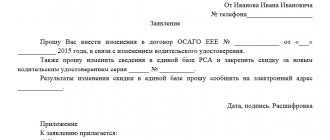

Many insurers offer the opportunity to add new drivers through a personal account on their website. To do this, you need to register and enter your contacts.

Basically, online adjustments are subject to e-CASCO, which is currently offered by a limited number of companies.

To add drivers, submit an application.

Scans of documents can also be sent online.

To add you must specify:

- his full name;

- age, driving experience;

- driver's license number;

- CASCO agreement number.

If a regular CASCO insurance was issued, then to add drivers you still need to visit the insurer’s office and bring the original passports and driver’s licenses of the new persons admitted to driving.

Sometimes the company also asks for a copy of the insurance contract and a receipt for payment.

Is it necessary to indicate all persons admitted to management?

It is necessary to enter all persons who operate the machine . If this is not done, then difficulties may arise with payment if the accident is caused by a person who is not allowed to drive.

Most likely, the insurer will pay compensation at the request of the insured, but then turn to the culprit of the accident with a recourse claim, demanding compensation for losses.

Insurance company refusal to pay

The absence in the policy of an indication of the driver who was driving the car at the time of the accident does not relieve the insurance company from the obligation to pay compensation.

This is stated in paragraph 34 of the Resolution of the Plenum of the Supreme Court dated June 27, 2013 No. 20 “On the application by courts of legislation on voluntary insurance of citizens’ property.”

If, despite judicial practice, a refusal to pay occurs, the client has the right to go to court and appeal this decision.

You can first send a claim to the insurer with a request to eliminate the violations and make a payment.

Right to recourse

The insurer is not obliged, but has the right to file a recourse claim against the culprit of the accident. The insurance company does not have the right to demand compensation from someone who is not at fault for the accident and who is simply not included in the policy.

But, if a driver who is not included in the insurance is found to be at fault, this is the basis for the insurance company to receive back the paid insurance amount through subrogation.

Any court decision on the insurer's claim can be appealed to the appellate and cassation instances.

Example of subrogation

Let’s say the car was driven by driver Ivanov, an 18-year-old son, who was not included in CASCO due to the high cost of the policy. They only registered his father with a good accident-free record, believing that they would receive the payment in any case.

The young man committed an accident and was the culprit. The amount of damage was estimated at 300 thousand rubles.

The father collected all the documents and submitted an application for compensation.

Within a month, the insurer reviewed the application and paid for repairs at the service station in the required amount.

A couple of months later, driver Ivanov received a copy of the insurance company’s recourse claim and an invitation to court.

Since all the evidence of his guilt was presented, Ivanov will be forced to compensate the insurance company for the cost of repairs (240 thousand rubles).

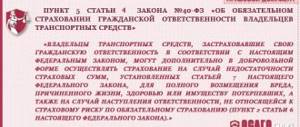

Is it necessary to include a second driver in CASCO?

Unlike “automobile insurance,” CASCO is voluntary insurance. In other words, it is not necessary to formalize it at all. And there is no penalty for his absence. As a rule, it is done by those who are not confident in their driving skills. And also when a new expensive car is purchased. When there is a risk of theft or damage. The restoration of which will require considerable personal financial expenditure.

Thus, it is not necessary to add a driver to this type of insurance. However, it is worth considering several nuances. Let’s say that one person has CASCO insurance, but the other driver is not included in the insurance. While driving along the route, he gets into an accident. Depending on who is found to be at fault for the accident, the following scenarios are possible:

1. The “opponent” is to blame for the incident and has a valid MTPL policy.

Then the offender’s insurance will cover the damage caused to the property. But only within 400 thousand rubles. If there is significantly more damage, the remainder could be covered by CASCO insurance. However, the driver does not pass through it, which means this type of insurance does not apply to him.

2. The same situation, but the culprit does not have a “car license.”

In this case, the issue of compensation is even more acute. Firstly, CASCO is also not valid for this driver. You will not have to rely on compensation from your insurance company. Secondly, it will be possible to “extort” money from the person responsible for the accident only through the court. And this is a long story and not always with a happy ending.

3. The collision was caused by the driver himself, who was not included in the optional insurance policy.

It is precisely such incidents that are covered under CASCO insurance. However, not for this person. Since he is not on the list of insured persons. That is, you will have to repair the car at your own expense.

As you can see, CASCO does not cover warranty cases if the vehicle was driven by a person not included in the policy. Therefore, if you have insurance for one driver, it is better to include a second one.

Policy Multidrive without restrictions

Multidrive is a CASCO insurance with an unlimited number of drivers allowed to drive the vehicle.

At the time of an accident, it may not be the policyholder who is driving, but any person, and at the same time, the owner of the multidrive can count on payment in full.

Claim for damages by the culprit

Subrogation means the transfer to the insurer of the right to demand compensation from the person responsible for the accident (Article 965 of the Civil Code of the Russian Federation).

If the driver who caused the accident was not included in the multidrive policy, then the insurer has the right to send him a letter demanding that he pay the amount of damage voluntarily.

If this is not done within the agreed time frame, a lawsuit will follow.

The policyholder is obliged to transfer to the company all documents and evidence necessary for going to court (this is provided for in the Insurance Rules).

In case of refusal, the insurer is released from paying the insurance compensation in full or in the relevant part and has the right to return the excess amount of compensation paid.

The right to demand compensation from the guilty party arises after full payment for the insured event has occurred.

Are there any restrictions?

Drivers over the age of 23 who have a driver's license (usually more than two years) can be included in the CASCO policy.

Drivers included in the policy must drive the vehicle legally.

Will damage be compensated if the driver is not included in CASCO and is involved in an accident?

In accordance with the Rules of Comprehensive Vehicle Insurance, the CASCO insurer recognizes such a case as not insurable and has the right to refuse payment of compensation.

In this situation, the owner of the vehicle can count on payment of insurance compensation only under the MTPL policy. The MTPL insurer of the driver through whose fault the accident occurred pays compensation for damage to the victim, but makes recourse claims to the culprit for compensation for losses incurred.

To receive compensation for damages, regardless of the role of other drivers driving your car during an accident, you need to include in your CASCO policy all people who may be given control of the vehicle.

What to choose?

New drivers can easily be included in an already issued CASCO agreement . To do this, you need to come to the office with documents and make changes to the policy or submit all the data in your personal account on the insurer’s website.

In some cases, you will have to pay extra for this service. The amount of the surcharge depends on how much time is left before the expiration date of CASCO, as well as on other factors.

If you have unlimited multidrive insurance, then you don’t need to arrange anything - anyone who has the legal right to do so can get behind the wheel of a car.