What does direct compensation for losses under OSAGO mean?

Direct compensation for losses means that the driver does not have to contact the company where the person at fault received insurance. With this approach, the victim has the right to request payments by contacting the company where he executed his MTPL agreement.

What is an alternative PPV under compulsory motor liability insurance?

Showing concern for car owners who suffered losses from a collision, the authorities passed a law giving the applicant the opportunity to independently choose an insurance company to receive compensation. Thus, the victim could use both the classic option of receiving payments from the company that insured the culprit, and the alternative option of contacting his own company.

However, the adopted law did not bring the desired results. Not very conscientious insurers used it as a loophole to “football” clients. Having presented a lot of arguments, the truth of which is difficult for an inexperienced client to verify, he was redirected to another insurance company. The process could be repeated there too. Instead of the expected simplification, the situation took a completely opposite direction.

There were also cases in which the victim submitted applications to both insurance companies at once in the hope of double payments.

The right of the victim to independently choose a company to receive compensation for the restoration of a damaged car is called an alternative PPV under compulsory motor liability insurance.

What is a non-alternative PPV in compulsory motor liability insurance?

In 2014, the law on payments underwent global changes. To resolve the situation, the authorities determined the only possible way to receive payments from the insurance company after the accident.

After innovations, you should apply for compensation only to the company with which the contract was concluded. The ambiguity in the relationship between the victim and the insurer was eliminated, along with the possibility of choice.

The payment method, when an application for compensation is submitted to the office of the company with which the contract was concluded, is called the non-alternative PPV OSAGO.

What else to read:

- My car was scratched in the yard, what should I do?

- Europrotocol 2021

- How to get money instead of repairs under compulsory motor liability insurance: a detailed review

Methods of compensation for losses

The direct method of compensation is applicable in the following cases:

- in the incident only vehicles were damaged, no harm was caused to the life and health of the participants;

- The car accident occurred as a result of a collision or other interaction between two cars, while the liability of both drivers was insured according to the rules of OSAGO.

In all other cases, a different procedure is provided, according to which compensation for damage under compulsory motor liability insurance is made by contacting the insurance company that issued the insurance policy to the culprit of the incident.

In addition, the law does not exclude the possibility of using both methods - for example, the victim has the right to make claims to the insurer of the culprit of the accident or to the culprit himself in court if it was subsequently established that harm was caused to the health of the driver or passenger.

What does the law say about PPV under compulsory motor liability insurance?

Dear readers!

Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem, please contact the online consultant form

It's fast and free!

Or call us by phone (24/7):

If you want to find out how to solve your particular problem, call us by phone. It's fast and free!

+7 (495) 980-97-90(ext.589) Moscow,

Moscow region

+8 (812) 449-45-96(ext.928) St. Petersburg,

Leningrad region

+8 (800) 700-99-56 (ext. 590) Regions

(free call for all regions of Russia)

The updated Federal Law on Compulsory Motor Liability Insurance, for which direct compensation for losses is assigned to the company of the victim's insurer, is the main act regulating insurance payments. Law No. 40 “On Compulsory Insurance” strictly defines the order of relationships:

- for insurance companies - in what situation, which company bears the costs;

- for the client - the conditions for contacting a particular company.

Also, direct compensation for damages from compulsory motor liability insurance is indirectly influenced by:

- Articles 186, 366, 325 of the Civil Code of the Russian Federation - on issues of financial relations;

- Chapter 55 of the Civil Code of the Russian Federation - annex to the Agreement for members of the Union of Insurers;

- Order of the Ministry of Finance of 2009 is the basis for the development of general norms of Federal Law No. 40.

The introduction of updates allowed:

- stop fraudulent machinations of insurers and unscrupulous clients;

- eliminate the ambiguity of existing legislation;

- make the payment procedure easier;

- exclude unjustified refusals by the insurance company to pay the client;

- reduce the period for receiving compensation.

Conditions for non-alternative direct compensation under MTPL

The new legislation allows the victim to undergo a simplified procedure for compensation for damage by contacting the insurance office where he executed the contract. This opportunity is provided if the approved conditions of the compulsory motor insurance policy are met:

- no more than two cars were damaged, one of which belonged to the victim, and the second belonged to the initiator of the incident;

- the participants in the accident have no injuries requiring medical intervention;

- Both drivers have MTPL policies;

- The traffic police report clearly indicates the culprit of the accident.

Once you make sure that the necessary requirements are met, you can receive direct compensation under OSAGO.

When is the MTPL applicable? Conditions and grounds

There are two conditions, they are clearly stated in Article 14.1 of Federal Law No. 40. In order for the victim to contact his insurance company, two circumstances must be met simultaneously:

- Only vehicles are damaged in an accident.

- All participants in an accident, no matter how many there are, have valid MTPL policies.

8(800)350-23-68

Dmitry Konstantinovich

Expert of the site "Legal Consultant"

Ask a Question

It is no coincidence that we have italicized information about the number of vehicles involved in the accident (according to clause 1 of Article 14.1 of Federal Law No. 40 - “two or more vehicles”). The point again is outdated information, which is full of information on the Internet. Previously, one of the conditions for using the PES was the participation of only two vehicles. This restriction has now been lifted.

When should you contact the insurance company at fault?

From the above conditions, or rather from the circumstances when they are not met, a non-alternative option follows, i.e. when you can only contact the insurance company of the culprit.

Accordingly, if there are injured people, then direct settlement of losses is impossible. With this option everything is more or less clear. Some difficulties arise in the absence of compulsory motor liability insurance for participants in an accident:

- If the culprit does not have a policy, then there is no company that will compensate for losses. In this case, insurance companies are completely excluded from the process. Compensation will need to be received either by agreement or through the court.

- If the victim does not have a policy, this is a violation of traffic rules and an administrative penalty may be applied for driving without insurance, but this does not deprive him of the right to compensation under the compulsory motor liability insurance of the perpetrator . Accordingly, the victim can contact the insurance company of the perpetrator, regardless of whether he has his own MTPL policy.

In what cases can payment be refused?

Refusal to pay and direct reimbursement are completely different concepts. A company has the right to send a notice of refusal to pay if there were gross violations when submitting documents or attempts to imitate an accident. The most common legitimate reasons for denial of payments include:

- incomplete package of documents;

- lack of a valid policy;

- attempting to obtain compensation for damaged art objects;

- violation of application deadlines;

- details for crediting funds are not specified;

- False information about the situation was provided.

Justified refusal in PES

Denial of direct compensation implies that the victim will still receive insurance payments, but a simplified method is not available to him. Reasons for refusal confirmed by law include:

- the insurance company of the accident initiator has gone bankrupt or lost its license;

- the company that insured the culprit did not take part in signing the agreement on simplified payments;

- contacting a company representative office instead of the main office;

- the victim filed a claim for payments to both companies at once;

- errors were made when applying for the policy;

- the protocol does not indicate a specific culprit of the accident or several are indicated;

- the European protocol is filled with gross violations;

- the vehicle was repaired before an expert assessment of the damage was carried out;

- there are casualties in the collision;

- more than two cars were damaged;

- The insurance specialists were not able to inspect the car within the established time frame.

Reference! Direct compensation for losses under compulsory motor liability insurance is impossible if any of the established reasons occur.

Unreasonable refusal

When an insurance claim is received that involves a large amount of payments, the company does its best to get rid of the client. Commonly used reasons for unlawful refusal include:

- this law does not apply in our organization;

- We have too many applicants, contact the initiator’s company;

- Now there are temporary financial difficulties, bring your application later.

None of these reasons is a legal basis for refusal. An insurance company that uses such methods is flagrantly violating the law.

In this case, the victim must request a written refusal indicating the reason. Based on the issued document, you should contact the RAS and, possibly, the court.

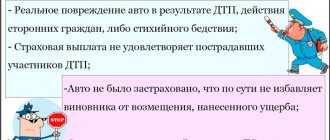

When PES is not possible

To fully understand direct compensation for losses under compulsory motor liability insurance, what it is, it is necessary to study the circumstances in the event of which payment is not made:

- the person whose actions caused the accident does not have a compulsory motor liability insurance policy or the expiration of its validity period;

- causing damage to property other than the car as a result of an accident, for example, real estate;

- the injured person has already submitted an application for compensation to the company in which the person responsible for the incident is insured;

- incorrect registration of the accident according to the European Protocol;

- lack of agreement between the parties to the accident, for example, about the causes of the accident;

- the participant in the road accident made a training trip in a car together with an instructor;

- the car damaged as a result of an accident took part in a test drive, race or other event of a similar nature;

- the actions of the person responsible for the accident became the reason for legal proceedings;

- the victim refused to provide the car for an independent examination;

- the insurer was not notified in a timely manner about the fact of the traffic accident;

- There are victims in the accident.

This list is not exhaustive. If there are legal grounds, the insurer may refuse to apply the PES in other situations. If the victim does not agree with his decision, he has the right to challenge the actions of the Investigative Committee in court, the verdict of which is final.

How to receive direct compensation for losses under compulsory motor liability insurance in 2021

Registration of a PES occurs in several stages. At each of them, it is important to avoid mistakes that will give the insurance company a reason to refuse. In general, the procedure for receiving direct compensation does not differ significantly from regular payments for an insured event and includes:

- collection of documents after an accident;

- transfer of the collected package to insurance employees;

- verification of the information provided by company employees;

- examination of vehicle damage;

- transfer of funds to the client's current account.

What documents to provide in order to receive direct compensation for damages from compulsory motor liability insurance?

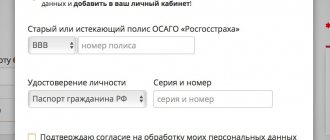

The set of papers required to receive services under a simplified procedure, in addition to the application, includes documents without which the application will be rejected. The package includes:

- passport of a citizen of the Russian Federation belonging to the applicant;

- permission to drive a certain type of vehicle;

- OSAGO;

- notification of an accident;

- confirmation of the guilt of one of the drivers from traffic police officers;

- checks and receipts for services paid in connection with the incident;

- details for transferring funds.

If the conduct of the case is entrusted to a lawyer, it is necessary to provide a power of attorney certified by a notary.

How to make an application for direct compensation under OSAGO

The application can be written either in free form or on the insurance company’s letterhead. It is better to clarify the correct form of writing directly at the company’s office. Many significant insurers provide a form to fill out when you submit a package of documents.

In most cases, forms are provided online. To download an application for direct compensation for losses under MTPL, you need to go to the official website of the insurer. If you don’t find the form on the website, it’s better to call the insurance company and find out if you can limit yourself to writing it by hand.

In any case, the application must be written in compliance with all the rules established for documents of this type. If any information is missing, the application will be returned for revision, and the victim will lose more time than planned.

The document states:

- full name of the company with which the insurance contract was concluded;

- information about the client’s place of registration and actual residence;

- Full name of the victim;

- telephone for communication;

- a detailed description of the accident that occurred (date, location, accompanying circumstances, nature of the impact);

- structures that were notified or took part in the registration of the accident;

- Full name of the accident initiator;

- information about his car;

- number of the MTPL policy belonging to the culprit;

- information about the damaged vehicle;

- applicant's policy;

- the amount of expenses associated with the accident (payment for a tow truck, expert...);

- applicant's signature;

- date and signature of the employee who accepted the documents.

Problems with direct indemnity

Despite the fact that updates to the law on PES have simplified the procedure for receiving insurance payments and reduced the percentage of fraudulent attempts on the part of insurance companies and clients themselves, certain difficulties remain unresolved. The PPV does not cover cases of mass accidents and those in which there are victims. Until now, the system of mutual settlements between insurance companies remains opaque. There are also many controversial issues regarding the payment of insurance compensation.

The problem of payments for non-contact accidents

The law has a limit on the number of cars damaged in an accident. Since the phrase “two cars” is used instead of the wording “no more than two,” disputes arise in the case of a non-contact accident.

A non-contact accident means that the car is damaged, but there was no collision with another car. Legally, this situation applies to insured events, provided that the car was used for its intended purpose.

In fact, insurance companies use the wording specified in the law to refuse to transfer payments. Thus, they force victims to undergo a lengthy and troublesome judicial procedure.

Underpayments under PES

According to the current legislation, the amount established by RSA is transferred from the insurer of the accident initiator to the insurance account of the victim. In this case, the amount of compensation actually paid is not taken into account. This gives rise to the use of various fraudulent schemes by insurance companies.

As a result, the client whose car was damaged suffers. If there is a large amount of payments to be made, the company tries to underestimate it as much as possible so as not to remain at a loss. With minor damage, the same thing happens, only the company is trying to make money in this way, receiving more compensation than was paid to the victim.

On average, the amount of payments under PES is underestimated by 25-40%, which in itself is already a lot. However, recently cases of underestimation of payments by 50% have become more frequent.

The only solution for the victim is to file a claim and recover the missing funds through the court.

Offer the victim to enter into a payment agreement

As a defense against lawsuits related to underestimation of the amount of payments, insurance employees use the “Agreement to Determine the Amount of Damage.” This document defines all criteria regarding the payment of compensation, including its amount.

If the client is persuaded to sign the agreement, he loses the opportunity to recover the missing amount through the court. The document gives the insurer the opportunity to consider that it has fully fulfilled all its obligations in a particular case.

It is possible to challenge the legal validity of a document in court in rare cases. At the same time, the trial procedure itself is quite problematic.