Can the insurance company refuse to pay?

Any insurer has the right to refuse to pay insurance compensation. This is provided not only in the text of the insurance contract and insurance rules, but also in the Civil Code of the Russian Federation, as well as the law “On the organization of insurance business”.

Reasons for refusal to pay under CASCO:

- gross violation of traffic rules by the policyholder (for example, drunk driving);

- transport malfunction even before an accident or other insured event;

- unauthorized repairs without agreement with the insurer;

- permission to drive persons not specified in the insurance;

- violation of the loss settlement procedure described in the policy.

This is not a complete list of reasons for refusal. The reason may be non-payment of an insurance contract (for example, insurance for a credit car, which is renewed every year), obvious violations of the rules on the road (exceeding the speed limit, running a traffic light, crossing a double solid line and driving into oncoming traffic), an attempt at insurance fraud (rigged Road accident or overestimation of damage) and much more.

Sometimes an event is simply not recognized by the insurer as insurable. For example, if the car was scratched by animals, and the risk of falling icicles, hail or hooliganism was insured, then, naturally, a refusal will follow. The company also does not recognize the case of car theft from a yard or other place as insurance if the contract clearly states that it should have been stored only in a guarded parking lot.

Refusal for all the above reasons will be considered absolutely lawful. But there are also controversial grounds for refusal, which can be easily appealed in court. For example, these include the refusal to compensate for the loss of commodity value, which is real damage under civil law.

If the insurance does not indicate the risk of theft, the insurer has the right to refuse payment if the policyholder's car disappears.

Refusal to compensate for damages

This is the most common problem. Most often, the insurance company does not pay for MTPL or CASCO insurance, using formal reasons for this. Such actions are illegal and easily challenged.

The insurer does not admit that the vehicle was damaged as a result of the claimed accident.

This problem may arise for owners of OSAGO and CASCO policies. The insurance company independently conducts an independent auto examination. Its results indicate that under the circumstances stated by the car owner, the existing damage could not have occurred. You can challenge this by conducting your own independent examination. Often in such cases it is necessary to go to court. If the outcome is positive, the insurance company is obliged to compensate the client not only for losses after an accident, but also legal costs, costs for assessing damage after an accident, penalties, fines, etc.

Request lines are missing.

The law does not give insurers the right to refuse compensation for damage due to the client’s failure to comply with deadlines for submitting documents. In practice, this reason for refusal is used less and less by insurance companies, but in the case of CASCO, missing deadlines is still considered a weighty argument. Owners of CASCO policies, however, can defend their rights. Missing the deadline for submitting documents is a reason for refusing compensation only if it affected the degree of the insured risk. Insurers must prove this in court. Since it is impossible to do this, the refusal is illegal.

The culprit of the accident was not indicated in the policy.

The insurance company refused to pay if the driver at fault for the accident was not indicated in the insurance policy, was drunk at the time of the accident, or was driving the car without a diagnostic card. In all these cases the insurance must be paid. The only difference is that later insurers collect the compensation paid from the driver responsible for the accident.

Refusal of compensation by TCB.

LTS (loss of marketable value) is included in the losses arising as a result of an accident. Insurers refuse to compensate for the vehicle's vehicle technical characteristics. For CASCO insurance, such a refusal is unlawful, as well as for MTPL policies - compensation for vehicle insurance is carried out within the limits of the insurance company's liability. This compensation, as a rule, has to be recovered through pre-trial or judicial proceedings.

The person responsible for causing the damage has not been found.

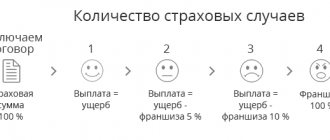

Payments under CASCO policies are made even if it is not possible to identify the person who damaged the car. In the absence of a culprit, losses are compensated if the policy is issued with “Damage” risk insurance.

The cause of the accident was a vehicle malfunction.

The insurance company refused to pay out under CASCO due to a vehicle malfunction. In such cases, insurers claim that the car was not damaged as a result of the accident, but already had damage before the accident, and it was they who caused it. In such a situation, the insurance company must prove that the car had defects before the accident. If she cannot do this, the damages must be compensated.

The cause of damage is natural wear and tear of parts.

The insurance company may claim that the damage was due to operating defects or normal wear and tear of vehicle parts. In most cases, these terms are interpreted incorrectly by insurers, and therefore refusals for these reasons are unlawful.

Errors when handling and reporting road accidents

After an accident, you must stop the car, turn on the emergency lights and put up a warning triangle (at least 15 meters from the car in the city and 30 meters outside it). If there are victims, you should call an ambulance immediately.

Next you need:

- report the accident to the traffic police and the insurer (phone numbers are in the policy);

- exchange contacts with other participants in the accident;

- take a photograph of the accident scene;

- collect contact information of witnesses in case of trial;

- wait for the arrival of the emergency commissioner or another representative of the insurer.

The insurer's dispatcher must record the date and time of the accident, and also advise what to do next. This is the correct procedure, but not every car owner follows it.

Next, you will need to prepare a written application and submit it to the insurance company. Typically, insurers require that this be done within 5-7 days from the date of the accident, but in the case of theft or theft - within 1-3 days.

Erroneous actions:

- leave the scene of the accident;

- go to the first service station and pay for repairs out of your own pocket;

- violate the application deadlines;

- receive money from the guilty party without knowing the extent of the actual damage.

When registering an accident, it is important to ensure that all formalities are followed. We fill out a notification of an accident with a diagram of the accident directly at the scene of the incident (if there are no victims and the parties decided to resolve the dispute without involving the traffic police) or we monitor the receipt of documents from the traffic police confirming the fact of the accident.

When receiving documents, make sure that their contents are accurate. Any corrections must be certified by an official’s signature and seal.

○ Going to court.

When contacting supervisory authorities, you need to remember: they only ensure that there are no violations of the law. They do not resolve disputes between the insurer and its client regarding the amount of compensation and interpretation of the provisions of the contract. Therefore, in many cases, after a claim to the insurance company has been unsuccessful, a citizen needs to go to court.

✔ Preparation for appeal.

Submitting an application requires some preparation. Therefore, before filing a claim, the client of the insurance company must:

- Maintain pre-trial order. Under OSAGO it is mandatory, under CASCO – only in cases where it is specified in the contract. If there is such an indication, then before going to court, you must file a claim and wait either for a response or for the deadline to expire.

- Conduct an independent examination to determine the exact amount of damage caused to the car. To do this, you need to contact an expert appraiser who has the necessary license and deals with auto issues. A representative of the insurance company must be invited to the examination (for example, by telegram). However, if after the invitation no one from the insurance company showed up, this will not invalidate the examination.

- Calculate the full amount of expenses incurred related to the claim of the unpaid amount. This will include expert fees, postal and transportation costs, etc. If you win the case in court, these costs will be reimbursed by the insurance company.

- Collect other evidence that will confirm the plaintiff’s case. Their exact list will depend on the specific circumstances of the case.

In the event that damage to the car was caused as a result of an accident, the applicant may need documents issued by the State Traffic Safety Inspectorate: an accident diagram, a certificate, an inspection report. In addition, if a medical examination was carried out, its results may also be required in court.

✔ Filing a claim.

When filing a claim, a citizen must be guided by the norms of the Code of Civil Procedure of the Russian Federation. First of all, you need to be guided by Part 2 of Art. 131, which describes the requirements presented by the court to the claim:

- “The statement of claim must indicate:

- 1) Name of the court to which the application is filed.

- 2) The name of the plaintiff, his place of residence or, if the plaintiff is an organization, its location, as well as the name of the representative and his address if the application is submitted by a representative.

- 3) The name of the defendant, his place of residence or, if the defendant is an organization, its location.

- 4) What is the violation or threat of violation of the rights, freedoms or legitimate interests of the plaintiff and his demands.

- 5) The circumstances on which the plaintiff bases his claims, and evidence confirming these circumstances.

- 6) The price of the claim, if it is subject to assessment, as well as the calculation of the collected or disputed amounts of money.

- 7) Information about compliance with the pre-trial procedure for contacting the defendant, if this is established by federal law or provided for by the agreement of the parties.

List of documents attached to the application.

List of documents attached to the application.- The application may indicate telephone numbers, fax numbers, email addresses of the plaintiff, his representative, the defendant, other information relevant to the consideration and resolution of the case, as well as the plaintiff’s requests.”

List of documents attached to the application.

List of documents attached to the application.The law does not provide for other requirements, as well as an official application form.

The statement of claim must be accompanied by:

- A receipt confirming that the fee has been paid.

- A copy of the application for the defendant (required) and third parties (if they are involved in the case).

- Copies of documents confirming the plaintiff’s position. The originals are presented at the hearing itself, and copies are attached to the case file.

- Petitions. The plaintiff has the right to ask the court to consider the case in his absence, to call witnesses, to demand evidence that he himself was unable to obtain, etc.

The statement of claim is filed with the court in whose territory the structural unit of the insurance company with which the dispute arose operates. You can file a claim in the following ways:

- Appearing in person at the court office.

- By sending a claim by mail.

- Using the Internet. This option is provided for by the Code of Civil Procedure, but a qualified signature will also be required here.

✔ Proof in court.

As a rule, the case is scheduled for consideration approximately a month after the claim is received by the court. The exact deadline depends on how many judges are currently working and how busy they are with other cases.

After the case has begun to be considered, the plaintiff must prove his case. There is no specific algorithm for proving it in court - it all depends on the circumstances of the case. In this case, the following can be used as evidence:

- Any documents containing information necessary for the case.

- Testimony of witnesses. The plaintiff must ensure their appearance himself. However, if necessary, he can ask the court for assistance and to send a subpoena to a specific person. As a rule, this is necessary in cases where the witness is busy during the meeting and needs to officially confirm to the employer the need to leave the workplace.

- Expert testimony. If the damage has been confirmed by an independent assessment, the appraiser may be summoned to court.

- Photos and videos. Typically, photographs are printed and attached to the case, and records are shown directly at the meeting, if technically possible. The files with the recordings themselves must be transferred to a medium (usually a CD or DVD), which can already be attached to the case.

- Evidence. In disputes about CASCO, they are rarely used, but the Code of Civil Procedure of the Russian Federation allows their use.

The procedure for the presentation and use of evidence is regulated by Chapter 6 of the Code of Civil Procedure of the Russian Federation. The plaintiff must first remember the following rules contained in this chapter:

- The evidence must be relevant. This means that only those that contain the information necessary for consideration should be used. Outsiders may be dismissed and not considered by the court.

- Evidence must be admissible. In some cases, the law directly restricts the use of certain types of evidence. For example, since by virtue of Art. 940 of the Civil Code of the Russian Federation, the insurance contract must be written, then if the document was not signed, by virtue of Art. 162 of the same code, witness testimony cannot be used to confirm the fact of its conclusion.

- Proving specific facts falls on the party that relies on them. The court can help with collecting evidence, but the judge will not prove anything for the plaintiff.

✔ Court decisions.

After the case is considered, the judge makes one of the following decisions:

- Satisfy the demands made by the plaintiff in full.

- Partially satisfy.

- Refuse the stated demands.

In the first case, after the decision comes into force (and usually the insurance companies try to appeal it, and then you have to wait for a judicial act from the second instance), you can already apply for a writ of execution and go with it to the bailiffs.

If the plaintiff does not agree with the judge’s decision, he has the right to appeal it. According to the Code of Civil Procedure of the Russian Federation, this can be done as follows:

- On appeal - if the decision has not entered into force.

- In cassation - if the entry has already taken place, and the appellate instance has refused to satisfy the complaint.

- In the supervisory court, through the Supreme Court - if cassation did not help.

What to do if the insurance company refuses?

If the policyholder did everything correctly, but received a refusal from the insurer, then he can appeal it. To do this, you will need to collect evidence of your case (certificate of an accident, notice and other documents), and prepare a claim. Sometimes it is also necessary to conduct an independent examination of the damage so that there is something to operate in court.

The policyholder must:

- Collect evidence that you are right.

- Prepare the text of the claim in two copies and send it to the insurer.

- If you receive a refusal (after 10-30 days), you can file a complaint with the regulator.

- If the complaint to the regulator does not help, you must file a claim in court.

- Obtain a court decision (on the collection of insurance payments or on refusal to satisfy the claim).

Disputes with the insurance company can drag on for 3-6 months. and sometimes for a year. However, filing a lawsuit does not guarantee a positive result. It is worth deciding on legal battles only if you are firmly convinced that your rights have really been violated.

○ Pre-trial dispute resolution.

If the company refuses to pay compensation, underestimates the amount or delays the consideration time, it makes sense to first contact the insurer itself. In the event that the refusal or other unlawful actions are caused not by the company’s internal policy, but by the incompetence or mistakes of a particular employee, at this stage it is possible to resolve the matter amicably.

The claim procedure may be:

- Voluntary - in cases where the client of the insurance company decides to first deal with the problem in this way.

- Mandatory - if the terms of the contract concluded with the CASCO insurance company directly indicate the need to first file a claim.

You can submit a claim as follows:

- Appearing in person at the company office. In this case, it is necessary to prepare the claim in two copies: one remains in the office, on the second the employee who accepted the claim must sign and date it. This method proves that the claim was actually filed.

- Send by mail. In this case, a registered letter with notification is used and – highly desirable! – with a list of the contents certified by the post office operator.

- By email. However, in this case the applicant will need a qualified electronic signature. You can obtain such a signature and a certificate for it from one of the certification companies operating in Russia.

The claim itself must contain the following information:

- Information about the insurance company (name, address, full name of the director).

- Applicant details.

- Number of the contract concluded with the insurance company.

- The reason for the application indicating what, in the applicant’s opinion, violations were committed by the insurance company.

- The period within which a response from the company is expected.

- Details of the bank account to which the insurance compensation should be transferred.

The claim must be accompanied by copies of documents about the accident (if it occurred), an expert appraiser’s opinion on the cost of restoration repairs and other evidence confirming the citizen’s position.

Where can I go?

To protect your rights, you can contact the chairman of the company’s board, and then the court or the Bank of Russia or the prosecutor’s office.

The policyholder's appeal to law enforcement agencies or a financial regulator may lead to an inspection of the insurer and even revocation of its license if serious violations are identified.

If the claim is up to 50 thousand rubles, then you can contact a magistrate. In all other cases, you need to submit documents to the district court at the location of the defendant (insurance company).

How to properly file a claim?

After receiving a written refusal to pay compensation, you can begin to file a claim. The text is compiled arbitrarily, but in compliance with certain rules.

The claim must include:

- contacts of the policyholder;

- description of the problem (date of the accident, amount of damage, steps already taken to resolve losses);

- requirements and deadlines for their implementation;

- Bank details (if required).

All contact information must be included in the complaint. Be clear about when and where the accident occurred, exactly how your vehicle was damaged, and what the amount of damage was.

The insurer must be required to eliminate the violation of the law and pay the money within the established time frame (for example, within a month).

If the company decides to pay for the repairs, then the issue can be considered closed, but if a refusal follows, then it is necessary to move on to the next stage - resolving the dispute in court. If the requirements are partially satisfied, you can also go to court.

When to go to court?

There are reasons for refusal that can be challenged in court. These include, for example, refusal due to a violation of the deadline for submitting an application for payment. If the plaintiff complies with the statute of limitations, then judges consider such claims.

If the company refuses to compensate for the loss of marketable value, then this can also be appealed, since according to the civil code this is real damage. True, judicial practice in such cases is different - there are also refusals to pay compensation.

The courts are also loyal to attempts to challenge the refusal to pay due to a late insurance payment. In this regard, the Civil Code of the Russian Federation also gives recommendations to pay money, but with the amount of the overdue contribution offset against the insurance amount.

In what cases is CASCO not paid?

The car owner should carefully monitor the validity period of the CASCO agreement, because if he gets into an accident at least the next day after the termination of the agreement, he will no longer have to count on any payments. In addition, an expired vehicle inspection certificate may serve as a valid reason for denial of insurance payment.

CASCO does not cover cases where the vehicle was subjected to a radioactive explosion, military action, became a victim of a rally, or suffered from bacteriological, radiation or chemical contamination. If the subject of insurance has been confiscated by government agencies, then, of course, no payments are due to the policyholder.

Before making a decision on your insurance claim, insurance agents must personally verify the authenticity of the information you provide by inspecting the technical condition of the vehicle. At this stage, it is necessary to turn on maximum vigilance, because it is during the inspection period that the insurer will do everything possible to reduce the amount of insurance compensation or find a reason to refuse payments. So, if, as a result of an inspection by insurance agents, it turns out that due to careless driving, the headlights of the vehicle were damaged, or the upholstery was damaged due to smoking in the car, or the vehicle was left overnight in a place unsuitable for parking, unguarded by anyone, then the issue of payments will be doubtful.

Particular attention for the insurer deserves clarification of the situation regarding the state in which the driver was at the time of the accident - whether he was under the influence of alcohol or drugs, or whether the driver was not the owner of the vehicle, but a person not specified in the insurance policy. Based on a study of these factors, the insurer makes a decision on your application.