Home/OSAGO/Compensation for vehicle insurance under MTPL in 2021

When purchasing a new car, the owner invests significant funds in the purchase. But as a result of an accident, the market value of the car may decrease significantly, so the car owner will not be able to receive an equivalent amount in the event of a sale. The proposed material discusses the features of compensation for the loss of the marketable value of a car under compulsory motor liability insurance in 2021, and whether the car owner should hope to receive it from the insurer, calculation methods, the procedure for compensation from the insurance company or the culprit of the accident, and other related issues.

When does the marketable value of a car lose under compulsory motor liability insurance?

Attention

Loss of marketable value under compulsory motor liability insurance is the difference between the price of the car before the accident and after restoration, with the elimination of damage received in the accident. Any, even the most high-quality repair is not able to eliminate defects without leaving a trace, and this will affect the value of the car in case of sale. That is why it is very important for the car owner to receive appropriate compensation from the insurance company.

According to Art. 7.1 of the methodological recommendations for forensic experts carrying out work to examine vehicles in order to determine the amount of damage, adopted in July 2013, payment of compensation for loss of marketable value of a vehicle under compulsory motor liability insurance in 2021 is possible only if the following conditions are met:

Attention! If you have any questions, you can chat for free with a lawyer at the bottom of the screen or call Moscow; Saint Petersburg; Free call for all of Russia.

- a foreign-made car should not be older than five years, a domestic one - three;

- machine wear level – up to thirty-five percent;

- compensation is paid if the accident was the first for the car;

- the car owner should not be at fault for the accident;

- compensation for vehicle insurance together with other insurance payments cannot exceed the maximum possible insured amount;

- the victim must have a valid MTPL auto insurance contract;

Please note:

Compensation under CASCO is subject to payment unless a contrary condition is specified in the contract.

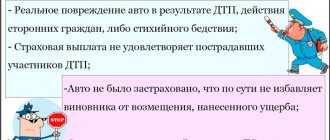

If the situation does not meet the above criteria, TCB will not be compensated.

General information about the loss of marketable value of transport

The TTS makes it impossible to sell the car at the original price.

Regardless of the level of repair work after an accident, there are still defects in transport that are easily detected by diagnostics. A buyer who suspects the car was involved in an accident may refuse to buy it or request a discount of 30–40 percent. The car owner can receive the TTS payment from the insurance company, which is obliged to reimburse this amount in addition to paying the costs of restoring the car. The size of the vehicle insurance is calculated based on the difference in the cost of the vehicle before the accident and after the repair. An application for payment of insurance policy must be submitted within the prescribed period and during the period of validity of the insurance contract. If this opportunity is missed, compensation can only be obtained from the culprit of the accident and through the court, which is fraught with long terms.

It is worth noting that you can only receive payment under CASCO insurance, because... in this case, it is the car, its performance and ability to operate that are insured. Only the injured participant in the accident has the opportunity to receive the TTS payment. For the culprit of transport accidents, a DSAGO agreement is valid, which covers damage caused to third parties.

Law on loss of marketable value under compulsory motor liability insurance

Article 5 of Law No. 40-FZ “On Compulsory Motor Liability Insurance” dated April 25, 2002, defines the rules of compulsory insurance and indicates the need to compensate for actual damage to the car owner in the event of an accident.

Many insurers refuse to pay compensation for the vehicle’s vehicle under compulsory motor liability insurance, justifying this decision with subparagraph “b” of paragraph 2 of Article 6 of Law No. 40-FZ, considering the decrease in the marketable value as lost profit. However, such a statement is incorrect. The clarification of the Supreme Court, set out in plenary decision No. 58 of the said authority, adopted in December 2021, speaks in favor of the car owner. The document determines the procedure for consideration by judicial authorities of cases regarding the payment of compensation under compulsory motor liability insurance in terms of vehicle insurance.

Attention

Clause 29 of Resolution No. 58 directly confirms the need to classify the loss of marketable value after an accident as real damage to the car owner and indicates that it must be compensated by the insurer under compulsory motor liability insurance.

If the amount of damage received exceeds the maximum possible amount of payment under compulsory motor liability insurance, the victim has the right to demand compensation from the person responsible for the incident, on the basis of Art. 1064 and 1072 of the Civil Code of the Russian Federation.

Loss of Trade Property Law

The rules for compensation for actually incurred damage are prescribed in Article 5 of Federal Law No. 40 “On OSAGO...”. According to this legislative act, such damage is subject to compensation in accordance with the civil liability contract. Some insurance companies refuse to compensate for vehicle insurance, erroneously or deliberately referring to Article 2 of Federal Law No. 40. In this case, they equate TTC with lost profits.

Expert opinion

Maria Mirnaya

Insurance expert

OSAGO calculator

However, the ARRF in Resolution No. 58 clearly indicates the illegality of such an interpretation of the law. The Supreme Court considers the loss of marketable value of a car to be equivalent to real damage. Therefore, the injured party has the right to demand compensation, in accordance with Article 1064 and Article 1072 of the Civil Law.

How to get the lost value of a car under compulsory motor liability insurance in 2021?

Although the law obliges insurance companies to compensate for the loss of the marketable value of a car under compulsory motor liability insurance, in reality, problems often arise with receiving such payments.

Often, insurers delay the calculation of compensation or refuse to compensate for damage. In 2021, the motorist must submit a corresponding application to the insurance company. In case of refusal, the issue will have to be resolved in court, as in most cases it happens.

How to recover vehicle title from the person responsible for the accident?

It is possible to recover the loss of the marketable value of a car from the culprit only in situations where all the conditions for compensation for damage are met. The car owner has the right to carry out such actions exclusively through court proceedings. Based on the experience of motorists, the culprit of an accident often refuses and does not compensate for the damage, citing legislation and insurance rules, which do not contain a clause obliging him to pay damages to the injured party. However, litigation often ends in failure for the culprit of the accident, since the court takes the side of the victim, since, according to the Resolution of the Supreme Court of the Russian Federation, TC refers to real damage and is subject to full compensation.

Download the statement of claim for compensation for damages in case of an accident (sample)

Procedure for obtaining TC

If the circumstances of the accident and the characteristics of the car meet the conditions that allow the car owner to claim compensation for the lost value of the car under compulsory motor liability insurance, the algorithm for obtaining compensation is as follows:

- contact the insurer, reporting the fact of the incident and stating the need for insurance compensation;

- write the necessary application and provide the documentation required for consideration of the insured event;

- present the car for examination;

- after assessing the condition of the car, carry out repairs at a service station suggested by the insurance company;

- contact independent experts to estimate the cost of repairs, taking into account payment for specialist services and the purchase of replacement parts, the price of the car after restoration and comparison with cars of similar characteristics that have not been in an accident;

- when the results of an independent examination with a comparative analysis are received, it is necessary to submit an application to the insurer for compensation for the vehicle’s vehicle;

- If the insurance company refuses or does not provide a negative response in writing within five working days, the car owner must file a claim with the court.

The paper is drawn up in two copies, one of which, with a receipt stamp (date and incoming correspondence registration number in the Investigative Committee), remains with the car owner.

In addition to the above, in 2021 the owner of the car must first carry out the necessary pre-trial actions, without which the consideration of the case in court will not be successful. To do this, the insurer is sent a pre-trial claim outlining the claims presented and notification of the intention to go to court.

IMPORTANT

A claim should be filed only if the management of the insurance company does not agree with the proposed requirements.

When the refusal to pay the TTS came

If the insurance company refuses to reimburse the vehicle insurance, the issue must be resolved through the courts. However, it is not recommended to rush into this for several reasons:

- the period for consideration of claims is 30 days;

- services of a representative of interests in court;

- material costs for resolving bureaucratic issues (state fees, requesting certificates and acts).

The car owner still has the opportunity to turn to the Civil Code of the Russian Federation, which provides for a pre-trial settlement procedure by contacting the insurance company in writing. If she again reported the refusal or the client did not receive an answer, then a statement of claim is filed with the court. In this case, it is recommended to seek legal services to competently draw up a claim.

Collection of vehicle insurance under CASCO insurance through the court

After considering the case, the judge schedules a hearing at which the issue of recognizing the claims of the injured car owner as justified is decided and the insurance company is obliged to pay the insurance premium by a court ruling that has legal force. If the court decision is positive, the client is entitled to:

- payment of vehicle insurance under CASCO in full, satisfied by the court;

- payment by the insurance company to the client of a penalty for failure to fulfill contract obligations in the amount of up to 50% of the amount of the subject of litigation;

- compensation for all costs of the trial.

10 days after the court decision, the decision comes into force and a sum of money is recovered from the insurance company in favor of the client.

Required documents

Receiving compensation for vehicle vehicle technical liability under compulsory motor liability insurance in 2021 involves the need to prepare the following documentation:

- papers previously provided as a result of the accident - statements, copies of the traffic police protocol, notice, accident report, examination results;

- car owner's passport and driver's license;

- insurance contract;

- confirmation of payment of state duty;

- diagnostic card and documents for the car (PTS and STS);

- an application with a corresponding request, drawn up according to the sample provided by the insurer;

- documents on the current market value of the car, determined by an expert;

- papers indicating the cost of the appraisal examination and confirmation of its implementation.

The documents are provided personally by the car owner or his authorized representative to the office of the insurance company. If, instead of the owner of the car, the papers are provided by an authorized person, his powers must be confirmed by a power of attorney.

Application to the insurance company for compensation for loss of marketable value of a car under compulsory motor liability insurance

There is no unified application form to the insurance company for compensation of loss of commodity value under compulsory motor liability insurance in 2021. Insurance companies may use their own templates for such requests. The main requirement is compliance with office work standards. An application for reimbursement of vehicle insurance is drawn up indicating the following information:

- the addressee of the application indicating the name of the structure, position, full name (right, top);

- applicant data;

- circumstances of the appeal with links to supporting documentation;

- information about the car and its estimated value after restoration;

- the amount of the recovered TTS based on the opinions of independent experts;

- bank details of the account where funds need to be transferred;

- list of attached papers.

At the end of the application, the applicant must sign indicating the full name and current date. A sample application is provided here.

Calculation of loss of marketable value of a car under CASCO

| Ytotal | The total loss is the loss of value that is calculated. |

| Ycar | The cost of repair work to restore parts of the body that make up its frame, which are non-removable. |

| Yel | The cost of repair work to restore all parts of the body that are removable. |

| Body | The cost of replacing the body or repairing those parts that violate the structural geometry. |

| Yokr | Body painting cost. |

To calculate what payment is due in 2021, the formula may be supplemented with other components depending on the specific situation.

Methods for calculating the lost marketable value of a car

Attention

A full calculation of the technical balance can only be performed by qualified experts from an organization that has a license for this type of activity. Several methods are used during the calculations. Which one to use is decided by specialists, but in most cases the Ministry of Justice is used, since it most fully satisfies the requirements of the judicial authorities.

Having studied the accepted methods, the car owner can independently calculate the amount of compensation or use an online calculator offered by one of the many sites on the Internet. But such a calculation is illegal and is used as a preliminary one to assess whether it is worth engaging experts to assess compensation - only the results of the conclusion of a certified organization are taken into account by insurers or courts.

Methodology of the Ministry of Justice

According to this method of calculating the vehicle price in 2021, the percentage of the price of a car after restoration as a result of an accident is compared to a similar one that was not involved in an accident.

The following formula is used for calculation:

C = S x ∑Ki/100 , where:

- C – part of the price of the car by which the market value decreased as a result of the incident (after restoration). This parameter needs to be set;

- C – how much the car cost before the accident;

- Ki is a special correction factor used by an expert when assessing a car.

When choosing an adjustment factor, follow the following rules:

- if, when restoring a machine, it becomes necessary to replace components connected by welding, the correction value is reduced by five times from the original value;

- Repairing parts should not cost more than replacing them;

- when eliminating defects that were not the result of an accident, the coefficient is reduced by half;

- the price of the car is reduced if, as a result of restoration, it was necessary to apply a new paint coating on the body.

The coefficient values are indicated in the tables of this methodology.

Calculation example of TCB

Below is an example of a calculation for a car that cost 600,000 rubles before the incident, if only the upper cross member of the radiator frame had to be repaired:

C = 600000 x 0.1/100 = 600 (rub.).

In the example, the amount of compensation due to the car owner will be six hundred rubles, if we use the methodology of the Ministry of Justice.

Guidance document method

The most complex technique that involves determining the price loss separately for each affected part. The following formula is used in the calculation:

In general = У1 + У2 + … + Уn , in which

У1 – Уn – the cost of restoring individual parts damaged in the accident. These characteristics are preliminarily calculated using the formula:

m

At el. = K2 x ∑K1 x Ci,

1

Where:

- coefficients K1 and K2 , respectively, are corrections that take into account the influence on the technical stability of the method of restoration and the degree of wear of parts;

- Ci is the retail price of the repaired spare part;

- m is the number of parts in need of repair or restoration.

The coefficients are taken from the tables given in the methodology.

Calculation example of TCB

An example of a calculation for minor damage to the front bumper of a car, with a part cost of 1,200 rubles:

- coefficient K1 is assumed to be 0.4, as for repair No. 1;

- K2 coefficient – 0.030 (removable body element);

- At the bump. = 0.030 x 0.4 x1200 = 14.4 rubles.

The damage indicated is minor, so the compensation amount is small. Using the above method, the TTC is calculated for each element, and the resulting values are summed up.

This technique is used for exclusive and expensive foreign-made car models.

Halbgewax method

This technique most accurately determines the value of the control unit and is used more often than other calculation methods. The formula is similar to that used in the Ministry of Justice method, but there are some differences:

Y = K / 100 x (CR + CO) , where:

- U – claim value;

- K – amendment accepted according to the table;

- CR – market price of the machine, taking into account wear and tear of elements;

- СО – repair cost for complete restoration of the car.

The coefficient used in the calculation takes into account the cost of spare parts (SM) and the amount of payment for the services of repairmen (SR). Two parameters are defined:

- A = (CO/CR) x 100%;

- B = (SR/CM) x 100%.

Calculation of UTR is advisable if the following conditions are met:

- Indicator A ranges from 10 to 90. If the price for restoring the car turns out to be incomparably less than the total cost of the car, the examination and calculation of the technical damage control will cost much more than the final compensation;

- Value B exceeds 40 - the cost of work significantly exceeds the price of spare parts and components.

An example of calculating the vehicle insurance

An example of calculating the loss of marketable value of a car under compulsory motor liability insurance, worth 600,000 rubles, two years old, if the CO is 70,000 rubles, and the SM is 20,000 rubles. (accordingly, the work will cost SR = 70,000 – 20,000 = 50,000 rubles):

- A = (70000/600000) x 100 = 11.67%;

- B = (50000/20000) x 100 = 250%;

- the coefficient for additional indicators will be 3.5;

- UTR = (3.5/100) x (600000 + 70000) = 23450 rub.

In this situation, the car owner must receive compensation in the amount of 23,450 rubles.

Loss of commercial value (TCV) of the car. Collection, judicial practice

Definition of the concept of TCB

Loss of commercial value (LCV) of a vehicle is a decrease in the value of a vehicle caused by premature deterioration of the commercial (external) appearance of the vehicle and its performance qualities as a result of a decrease in the strength and durability of individual parts, assemblies and assemblies, connections and protective coatings due to a traffic accident and subsequent repairs (see decision of the Supreme Court of the Russian Federation dated July 24, 2007 N GKPI07-658).

Question: is the loss of marketable value taken into account when determining the amount of insurance payment (does the insurance compensation refer to actual damage or to lost profits)?

Answer: yes, loss of marketable value is taken into account when determining the amount of insurance payment.

Explanations of the Supreme Court of the Russian Federation on the classification of technical damage to real damage

By decision of the Supreme Court of the Russian Federation dated July 24, 2007 N GKPI07-658, paragraph one of subparagraph “b” of paragraph 63 of the Rules for compulsory civil liability insurance of vehicle owners, approved by Decree of the Government of the Russian Federation dated May 7, 2003 N, was declared invalid from the date the court decision entered into legal force. 263 (as amended by Resolution No. 775 of December 18, 2006), in the part that excludes the amount of loss of marketable value from the insurance payment in the event of damage to the victim’s property.

At the same time, the Supreme Court of the Russian Federation indicated:

“...In accordance with Article 15 of the Civil Code of the Russian Federation, a person whose right has been violated may demand full compensation for the losses caused to him, unless the law or contract provides for compensation for losses in a smaller amount (clause 1); Losses are understood as expenses that a person whose right has been violated has made or will have to make to restore the violated right, loss or damage to his property (real damage), as well as lost income that this person would have received under normal conditions of civil circulation if his right was not violated (lost profits).

From the analysis of Article 6 in conjunction with paragraph 2 of Article 12 of the Federal Law “On Compulsory Insurance of Civil Liability of Vehicle Owners” it follows that if damage is caused to the property of the victim, compensation within the limits of the insured amount is subject to actual damage. This condition of the public contract of compulsory civil liability insurance of vehicle owners is directly enshrined in subparagraph “a” of paragraph 60 of the contested Rules.

Loss of marketable value is a decrease in the value of a vehicle caused by premature deterioration in the marketable (external) appearance of the vehicle and its performance as a result of a decrease in the strength and durability of individual parts, assemblies and assemblies, connections and protective coatings as a result of a traffic accident and subsequent repairs.

Thus, the loss of the marketable value of a vehicle, entailing a decrease in its actual (market) value due to a decrease in consumer properties, refers to real damage and, along with restoration costs, should be taken into account when determining the amount of insurance payment in the event of damage to the victim’s property.”

By the decision of the Supreme Court of the Russian Federation dated November 6, 2007 N KAS07-566, the decision of the Supreme Court of the Russian Federation dated July 24, 2007 was left unchanged, the cassation appeal of the Government of the Russian Federation was not satisfied.

Plenum of the Armed Forces of the Russian Federation in 2021 confirmed that the vehicle insurance is subject to compensation, including when the car is repaired under compulsory motor liability insurance

The real damage resulting from a traffic accident, along with the cost of repairs and spare parts, also includes the loss of marketable value, which is a decrease in the value of the vehicle caused by the premature deterioration of the marketable (external) appearance of the vehicle and its performance as a result of a decrease in strength and durability of individual parts, assemblies and assemblies, connections and protective coatings due to a traffic accident and subsequent repairs.

Loss of marketable value is also subject to compensation if insurance compensation is carried out within the framework of a compulsory insurance contract in the form of organizing and (or) payment for restoration repairs of a damaged vehicle at a service station with which the insurer has entered into an agreement for the repair of the vehicle, in accordance with the law. the limit of the insurance amount (See paragraph 37 of the Resolution of the Plenum of the Supreme Court of the Russian Federation of December 26, 2017 N 58 “On the application by courts of legislation on compulsory insurance of civil liability of vehicle owners”)

0

Author of the publication

offline 12 hours

GarryB83

0

Comments: 0Publications: 1252Registration: 07/17/2018

What to do if payment is refused?

If the insurance company refuses to compensate for vehicle insurance under compulsory motor liability insurance, in 2021 the car owner must file a claim with the court at the location of the insurance company. The appeal must contain the following information:

- the name of the body to which the claim is filed, indicating the surname and initials of the head;

- personal information of the applicant;

- description of the circumstances of the case, taking into account the attempt to resolve the issue pre-trial;

- regulatory references confirming the legality of the application;

- requirements presented by the applicant;

- list of attached documents.

IMPORTANT

At the end of the application, the applicant must sign and indicate the date the paper was prepared. To increase the likelihood of successful consideration of the case, qualified legal assistance will not hurt.

What to do if payment is refused

Legislative norms oblige insurers to pay MTPL clients under compulsory motor liability insurance. But not all agencies comply with this instruction - they try to provide compensation under various pretexts. In this case, the owner of the damaged vehicle has the right to apply to the judicial authorities to protect his interests.

Expert opinion

Maria Mirnaya

Insurance expert

OSAGO calculator

Before filing a claim in court, the driver should collect the most complete documentary base to prove his case. This is a copy of the claim submitted to the insurer, its written refusal to pay compensation, the conclusions of independent appraisers, etc. Based on the results of the consideration of the case, the judge issues a verdict on forced recovery from the insurance company of the cost of the vehicle insurance in favor of the plaintiff.