What is TCB and who gets paid?

In legislative acts, loss of marketable value is defined as a decrease in the price of a car due to damage received in an accident. This interpretation of the UTS is given in the resolution of the Supreme Court of the Russian Federation No. 58. Therefore, two cars of the same model and year will be worth differently if one of them was in an accident and the other was not. This market rule applies even if the damage sustained in the accident is minor.

De jure, the vehicle’s vehicle’s technical damage control refers to the actual damage received by the vehicle. Therefore, he is subject to compensation under MTPL. But this rule does not apply in all situations.

Can not understand anything! How much will they pay in rubles?

The above formulas are used by independent experts, and even then the TCB program calculates them for them. It is not surprising that you are unlikely to be able to calculate it yourself.

But let's give a small example.

Let’s say the cost of the car on the date of calculation of the vehicle tax in 2021 will be equal to 500,000 rubles. The repair impacts included:

- replacement of the rear spar (0.5% according to the table),

- replacement of the rear panel (0.3% according to the table),

- coloring of this panel (0.5% according to the table).

We count: 500,000 rubles. x (0.5% + 0.3% + 0.5%)/100% = 6,500 rubles .

Thus, to the cost of restorative repairs of a vehicle damaged in an accident under compulsory motor liability insurance, an additional vehicle insurance amount of 6,500 rubles will be added.

In general, you can simplify the formula even more and, thereby, make the calculation even more roughly. Just take approximately 8-10% of the market value of the car - this will be the average amount of vehicle insurance for average damage to the car.

Looking ahead a little, let's say that if repairs were carried out at a service station in the direction of the insurer, then the victim will be able to simply receive payment from the TSA in cash in the same amount of 6,500 rubles.

Loss of Trade Property Law

The rules for compensation for actually incurred damage are prescribed in Article 5 of Federal Law No. 40 “On OSAGO...”. According to this legislative act, such damage is subject to compensation in accordance with the civil liability contract. Some insurance companies refuse to compensate for vehicle insurance, erroneously or deliberately referring to Article 2 of Federal Law No. 40. In this case, they equate TTC with lost profits.

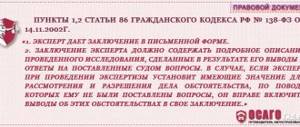

Expert opinion

Maria Mirnaya

Insurance expert

OSAGO calculator

However, the ARRF in Resolution No. 58 clearly indicates the illegality of such an interpretation of the law. The Supreme Court considers the loss of marketable value of a car to be equivalent to real damage. Therefore, the injured party has the right to demand compensation, in accordance with Article 1064 and Article 1072 of the Civil Law.

What it is

A car, as a rule, becomes unusable as a result of road accidents, so it must be restored.

The concept of “loss of marketable value” means the impossibility of restoring its technical condition and value in accordance with what it was before the accident.

It is expressed in objectively irreversible changes:

- its technical parameters characterizing the dimensions;

- physical and chemical properties that materials for the manufacture of structural parts have;

- characteristics in proportion to technological processes that gradually worsen the functional and operational characteristics of the vehicle.

The difference in price is the amount of commodity value that is lost when the car gets into an accident. In some cases, it significantly exceeds the amount of damage caused if the car was new and the accident was minor.

Compensation for loss of marketable value serves as proof that the car was actually involved in a traffic accident.

When is reimbursement for vehicle vehicle insurance carried out under compulsory motor liability insurance?

Even after a well-performed repair, when there are no external signs of damage to the car, its market price is still reduced by 15-30%. This is especially true for new cars - a price drop by 1/4 ultimately results in significant financial losses.

But not all drivers involved in an accident can count on compensation payments. According to the methodological guidelines of the Federal Budgetary Institution under the Ministry of Justice, the loss of commodity value is compensated if:

- The total service life of the vehicle is less than 5 years.

- The car has never been in a road accident with damage before.

The maximum amount of payments for loss of the marketable value of a car under compulsory motor liability insurance cannot exceed 400 thousand rubles . Such a limit is established by the provisions of Federal Law No. 40.

What is loss of marketable value of a car?

VTS traditionally refers to a reduction in the price of a car.

If the car was in an accident or was damaged in a snowfall or flood, then even after restoration it will cost much less than before.

Performance characteristics and presentation deteriorate; it will not be possible to hide the information that the car was under repair.

The size of the vehicle is calculated using special formulas, but in fact it is equal to the difference between the price of a repaired car and a new model (taking into account the wear and tear of the car).

How to receive payment of the vehicle insurance policy under compulsory motor liability insurance

Receiving compensation under the TTS is possible only after the injured driver contacts the insurer.

The step-by-step procedure algorithm looks like this:

- The owner of the damaged vehicle contacts the insurance company regarding the accident.

- Draw up a statement in the prescribed form.

- Collect all necessary documentation for calculating payment.

- Submit an application with supporting documents to the insurer.

- Provide the car for inspection by experts.

- After the vehicle is inspected by experts, it is repaired according to the direction received from the insurer.

- After repairs, the car owner carries out an independent assessment, which concludes with an estimate of its market price.

- A comparison is made between the price values of a restored car and a similar car that has not been in an accident.

- Based on the difference in indicators, the owner of the damaged vehicle submits a claim to the insurance company for compensation of lost commodity value.

Application for vehicle insurance under compulsory motor liability insurance, sample

A prerequisite for receiving payments for compensation of TCB is the submission of an application and a set of documents. It is not at all necessary to submit them together with the main claim for compensation for damage under compulsory motor liability insurance. The legislation sets a period of 3 years for this from the date the car gets into an accident.

sample

The application is written in free form, either on a special form or on a standard A-4 sheet. It specifies the details for the insurer to transfer the amount of money. The car owner may also require payment of compensation in cash, having received it from the company’s cash desk.

Package of documents required to be submitted along with the application:

- Certificates and copies of protocols from the traffic police about the circumstances of the accident.

- Vehicle owner's passport.

- PTS and SOP of the car.

- A valid MTPL policy.

- Diagnostic examination card.

- Machine appraisal report.

- Receipt for payment of the examination.

We receive compensation under UTS OSAGO correctly

Dear readers!

Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem, please contact the online consultant form

It's fast and free!

Or call us by phone (24/7):

If you want to find out how to solve your particular problem, call us by phone. It's fast and free!

+7 (495) 980-97-90(ext.589) Moscow,

Moscow region

+8 (812) 449-45-96(ext.928) St. Petersburg,

Leningrad region

+8 (800) 700-99-56 (ext. 590) Regions

(free call for all regions of Russia)

In fact, the methodology for calculating the amount of compensation is quite complicated, since it depends on a number of factors. Thus, each damage to the body, parts or paintwork of a car has a coefficient. Depending on the type of repair performed, the complexity of the operations and the type of damaged parts, the final amount of the insurance payment will change. Some situations where a serious accident has occurred may result in a payment of up to 10% of the value of the car on the secondary market at a particular point in time.

A ruling from the Supreme Court, issued on January 29, 2015, obliges insurance companies to pay compensation for the loss of marketable value of a car under compulsory motor liability insurance.

This document states the following: insurers are obliged to pay the amount for the vehicle obtained as a result of calculation based on the fact of damage to the vehicle. What's really going on? Ninety-nine percent of insurance companies do not pay TSA voluntarily. Payment is made only after drawing up a pre-trial claim and a correctly drawn up application.

Notice the word “correct” mentioned above. It is a correct statement drawn up according to a template that in almost one hundred percent of cases leads to payment to the victim. This happens in a pre-trial manner, which makes this procedure as profitable and useful as possible for the vehicle owner. We have prepared an algorithm of actions that will help you correctly prepare all the documents and submit applications to the necessary authorities:

- The first and most important thing to do is to calculate the vehicle technical value and obtain a certified “Certificate of Calculation of the Cost of Loss of Marketable Value of the Vehicle.” This document can be issued at any company that provides appraisal services in the context of restoration repairs. Experts will evaluate a certified copy of the repair report, as well as the vehicle inspection report from the insurance company, if available.

- After this, you need to write an application for compensation of the TTS, attach the above-mentioned act to it and send it to the insurance company. We will attach a template application at the end of the article.

- We remind you that most cases end in pre-trial proceedings. As for the case when you are denied payment, you will definitely have to go to court. The appeal is made directly to the insurance company. Situations are possible when a company goes bankrupt or the amount of the calculated payment exceeds the limit specified in the MTPL policy. In such a situation, a statement of claim must be filed against the individual responsible for the accident.

Unified methodology for calculating the technical stability

Calculation of the car's vehicle vehicle value is carried out by employees of the insurance agency in accordance with established methods. They were developed by the Forensic Science Center under the Ministry of Justice. The amount of value lost on a car that has been involved in an accident depends on the type and severity of the damage received, as well as a number of additional factors.

It is calculated using the formula: UTS = Sts x (∑Kuts: 100%).

Where:

- UTS – the amount of loss of commodity value, expressed in rubles.

- Pts – the price of the vehicle at the time of calculation (after restoration).

- ∑Kuts – repair impact coefficient, expressed as a percentage.

All digital values inserted into the formula are established during an expert examination of the machine.

We calculate the vehicle's vehicle's vehicle: key techniques

The marketable value of a car can be calculated using one of three methods given below. Among others, these calculation options are used most often by expert appraisers due to the fact that they give amounts that are as close to reality as possible. Qualitative calculation of vehicle insurance under compulsory motor liability insurance can be carried out in the following ways:

- Guideline Document Methodology.

- Halbgewax technique.

- Methodology of the Ministry of Justice of the Russian Federation.

Let's look at the first two. At this point, it is important to understand that any of the above calculation methods can only be used for vehicles that are not older than 5 years and do not have a wear level higher than 40 percent. In other words, it all depends on the value of the car at the time the accident occurs.

Terms of payment of vehicle insurance under compulsory motor liability insurance

The law does not establish specific deadlines for filing an application for reimbursement of TCB. Therefore, by default, they are taken for 3 years - this is the time limit in force in the Russian Federation for property claims. The insurance company, after receiving a request with all the necessary documentation, is obliged within a month . When an agency, for any reason, refuses to pay compensation under the TTS, it is obliged to notify the owner of the vehicle within five days. The notice must indicate specific reasons for the refusal with reference to applicable laws.

Judicial practice: typical cases

We have already mentioned that, according to statistics, the majority of correctly completed applications for TCB compensation are resolved at a pre-trial hearing. However, this does not negate the fact that failures do occur. Most often, this happens due to the fault or carelessness of the plaintiff: incorrectly filled out applications, an incomplete list of documents, an erroneously conducted examination, etc.

As a result, the insurance company gets away with it, saving considerable sums on its clients. We can safely say that in 1 out of 10 cases it will not be possible to reimburse the TCB. In general, failure to comply with at least one of the points listed above in the article is enough to receive a refusal to pay. Another option, which is more common than others, is the right of the insurance company not to reimburse the cost of the vehicle. If this is stated in your MTPL policy, then the court will most likely side with the accused.

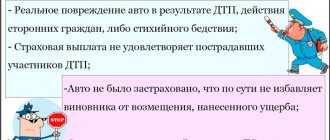

In what cases is the payment of TTC not carried out?

The owner cannot always demand payment for the loss of the marketable value of the car under compulsory motor liability insurance. The insurer has the right to legally refuse this in the following situations:

- The passenger car is more than 5 years old, and the truck is more than 3 years old.

- The car, more than 2.5 years old, was used with increased intensity. This is established based on the results of assessing the wear of main components and parts by experts.

- The car has already been repaired before, including painting after receiving scratches.

- Parts damaged in an accident show signs of natural wear (scratches, rust).

When loss occurs

Insurance is the possibility of obtaining compensation for damage to property. In the case of a car, its payment is made in a number of cases specified by law. One of them is a reduction in the primary commodity price of a car (after an accident); according to compulsory motor liability insurance, this risk must be covered.

VTS is a drop in the price of a vehicle caused by wear and tear of the body and internal mechanism parts. May occur as a result of an accident or improper operation.

Factors, the presence of which allows us to talk about the emergence of CTS:

- Physical malfunctions, seal damage.

- Defects resulting from road accidents and restoration work.

- Existing shortcomings are reflected in the appearance of the car.

- The consequences are irreversible and cannot be restored.

What to do if payment is refused

Legislative norms oblige insurers to pay MTPL clients under compulsory motor liability insurance. But not all agencies comply with this instruction - they try to provide compensation under various pretexts. In this case, the owner of the damaged vehicle has the right to apply to the judicial authorities to protect his interests.

Expert opinion

Maria Mirnaya

Insurance expert

OSAGO calculator

Before filing a claim in court, the driver should collect the most complete documentary base to prove his case. This is a copy of the claim submitted to the insurer, its written refusal to pay compensation, the conclusions of independent appraisers, etc. Based on the results of the consideration of the case, the judge issues a verdict on forced recovery from the insurance company of the cost of the vehicle insurance in favor of the plaintiff.

Application to the insurance company

If all the conditions specified above are met, the car owner is obliged to obtain an independent expert report. It will contain not only conclusions about the technical condition of the vehicle, but also the specific amount of the vehicle insurance amount.

With this document you need to go to the insurer to draw up an application. There is no strict sample application, so the application is written according to the rules of the official application, indicating the essence for which the car owner is applying, as well as attaching a copy of the examination report.

It is not a fact that compensation will be paid immediately, so you need to be prepared to seek money through the courts. Although recently insurers have stopped arguing with the policyholder on this issue, because the courts in 99.9% of cases decide the case in favor of the plaintiff, i.e. car owner.

FAQ

When determining the vehicle insurance and litigation with the insurance company, some questions arise related to the calculations, examination and accounting of the vehicle insurance by different companies. An easy way to calculate the due amount of the TTS is quite important, since it makes it possible to easily determine the amount, and the driver who wants to receive compensation must understand the nuances that arise.

Is it possible to calculate online?

Online services have long allowed you to use a calculator specially designed for calculating the TTC, which, after entering the data, produces the result.

You can find it by searching, and the best sites offer flexible settings for the calculation process. Among the different blocks, you can choose a list and the severity of the work performed, including painting, replacement, and work in violation of the factory assembly.

All that remains is to enter the cost of the car at the time of the accident, taking into account depreciation, after which the calculations will be made automatically.

The results of such actions cannot be provided to the insurance company for payment, but the car owner himself will be able to understand what he can count on. Official confirmation of the size of the TCB requires contacting a disinterested expert; only his conclusions will be accepted.

In what cases is an independent examination of a vehicle required?

The insurance company can independently conduct an examination with the involvement of experts, but the owner may not agree with the amount, and this is his right.

The insurance company may even refuse to pay, and in both cases it is necessary to involve an independent expert to conduct a study to determine the extent of the lost value of the car.

Most often, the reason for the examination is precisely dissatisfaction with the amount of payment offered by the insurance company, and in the hope that the expert will estimate the damage higher, the driver turns to a specialist. Experts' results, duly certified and in the correct form, serve as the basis for providing funds or recourse to court in case of refusal.

Is this value taken into account by Rosgosstrakhavto?

The law states that all insurance companies, regardless of whether an OSAGO or CASCO agreement is drawn up, must consider vehicle insurance as damage and make appropriate payments.

The Rosgosstrakh company, which provides both types of insurance, must take into account the UTS, but court practice already has a number of cases in which this insurer refused to pay the commodity value.

The client still received payment according to the court decision, but when insuring with this company, you should know that the clause on the absence of payments under the TTS must be excluded from the contract, otherwise it will not be possible to prove the right to this money.

Find out what a tachograph is from the article: tachograph. What is the fine for a tachograph without cryptographic information protection in 2021, read here. If you want to know the list of documents for obtaining a driver card for a tachograph, see here.

Loss of the marketable value of a car occurs in serious accidents in which the car is severely damaged and even its restoration does not return the market value. In this case, the owner can apply for payments under the vehicle insurance policy, but to do this, he must have a fairly new car that has not previously been involved in an accident, and the driver himself must not be the culprit of the accident. If you refuse to provide funds, you can go to court, but there must be grounds for this that will be considered significant by the judge. Practice shows that most often car owners still receive the amount of vehicle compensation due to them, which is required by a court decision.

Receive payment under the TTS in court

They apply to the court to protect their rights in the case when the insurance company refuses to pay and when the amount of compensation exceeds that required under compulsory motor liability insurance or comprehensive insurance. The statement of claim must contain the following information:

| No. | Claim document | Attachments to the claim |

| 1 | Name of the district court | All correspondence with the insurance company: initial application, subsequent claim, written refusal (if any) |

| 2 | Details of the plaintiff and defendant | STS and PTS for a car, diagnostic card |

| 3 | Circumstances of occurrence of damage | Traffic police protocol and European protocol (if available), resolution to initiate a case, all notices, document identifying the culprit of the accident, etc. |

| 4 | Size and list of damages | Examination report |

| 5 | Measures taken by the plaintiff to resolve the dispute out of court | Policy, MTPL agreement, CASCO insurance |

| 6 | Requirements of a material nature (for UTS) and moral (for the unjustified refusal of the insurance company to pay) | Agreement with an expert organization and receipt for payment for services |

| 7 | List of additional documents | Receipt for payment of the state fee for going to court |

| 8 | Date, plaintiff's signature |

On a note!

The Europrotocol allows you to quickly determine the damage that occurred after an accident. But it is possible to issue it provided that all participants in the accident have compulsory motor liability insurance.

The court may order several additional procedures. Namely:

- re-examination of the market value of the car;

- forensic examination for hidden damage that may have occurred before the accident, establishing the wear and tear of the car.

Attention!

The statement of claim is submitted to the court at the location of the insurance company or residence of the guilty participant in the accident (if compensation is required from him).

In what cases do they go to court?

Lawyers advise that cases involving insurance and compensation payments be resolved pre-trial. But if you can’t reach an agreement, you’ll have to go to court. Writing a statement of claim is justified in the following cases:

- The insurance company categorically refuses to make payments.

- The Investigative Committee refuses to negotiate - does not accept the application and claim, and does not give a written response to them.

- The refusal of the claim and application is unfounded.

- The payment was made, but not in full.

- The insurance company agrees to pay compensation, but does not pay it, and there is a significant delay.

- The Investigative Committee makes a claim that the car owner is guilty and ignores the protocol, resolutions and other documentation submitted to the traffic police.

- The compensation, together with other insurance payments, exceeds the amount under compulsory motor liability insurance.

- SK insists on increasing the parameters of age and wear.

- The insurance company initially does not recognize the loss of a car’s marketability as an insured event.

On a note!

The insurance company will definitely conduct its investigation and pay attention to the nature and duration of the damage, and how its presence affects the value of the car.

In what cases will a claim be denied?

In addition to the cases explicitly specified in the law (age, wear and tear of the car, etc.), there are a number of circumstances in which the expert commission will not prepare a calculation for payment. Namely:

- Domestic trucks more than a year old.

- Foreign trucks used in commercial transportation that are more than 2 years old.

- Foreign buses used for commercial transportation of passengers (for example, public transport), more than 3 years old.

- Foreign buses used as tourist transport are more than 5 years old.

Attention!

There is a statute of limitations for cases of collection of TTS; currently it is 3 years.

Popular questions on the topic

Question

: What is the time frame for filing a claim, usually immediately after an accident?

Answer

: The standard period for filing a claim for compensation for damage received in an accident is 5 days. But the interval does not apply to the position of the vehicle. To determine the amount of loss you need to have an expert opinion on hand. For these cases, the statute of limitations applies; compensation for the TTS can be claimed within 3 years.

Question

: Is it possible to carry out an examination without the presence of a representative of the insurance company?

Answer

: The examination is scheduled for a specific date, which is agreed upon by the customer and the contractor. You must notify the insurer at least three days in advance. If a company representative fails to appear at the specified time, the inspection procedure is carried out without him.

Question

: If you have already submitted an application for compensation for emergency damage, but later a conclusion about the presence of a technical equipment appears, do you need to submit another one?

Answer

: Yes, based on the results of the examination, the amount of the technical compensation is established, and an application is submitted specifically for compensation for this damage. But if the maximum insured amount is indicated in the first application, then there will be no refund for the second position (only within the insurance limits).

How to get a refund

An insured car under compulsory motor liability insurance in 2021 - 2021, which was involved in an accident, must be restored at the expense of the limit. Since UTS is a real damage recognized by the Supreme Court, the company has no right to refuse it. There are certain conditions and criteria that deserve attention. The appointment procedure will also be discussed below.

Conditions for receiving:

- issued only to the affected participant;

- the amount of the UTS is included in the total limit of the insurance return payment;

- the age of the vehicle is not more than 3 and 5 years for domestic and foreign transport, respectively;

- in terms of wear and tear, the percentage compared to a new car is not higher than 35;

- systems, parts, problems with which caused the loss of primary value, were not damaged under other circumstances.

Important!

A percentage of 35% or more gives the insurance company the right to refuse to pay compensation to the insurance company.

Receipt procedure

- Registration of road accidents in compliance with the law.

- Ordering an examination of the car for which you plan to receive a refund.

- Submitting an application and a complete package of accompanying papers to the responsible company.

- Payment of funds.

Important!

When considering an application, close attention is paid to the correctness of the application, as well as the completeness of the additional documentation provided.

Required documents

- passport copies + original document for identification;

- OSAGO agreement;

- certificate from the traffic police about the accident;

- vehicle inspection report;

- report on the completion of the assessment examination;

- notification of an accident;

- resolution on initiating an administrative case;

- driver's license.

On a note!

Copies of the above-mentioned papers are attached to the application. Originals are needed to verify facts. In the future, when filing a claim, it will be necessary to obtain a court decision and compulsory collection of compensation.

Statement

An application must be submitted for compensation for loss of marketable value of a damaged car (MTPL guarantee). There is no single standard form enshrined in law. You can take the example of previously submitted applications as a model.

Example of filling out with a list of required positions

- A cap. The recipient's full name must appear in the right corner at the top of the page. You also need to enter the full name of the head of the department to which the application is being sent. Below in the same part of the document indicate the applicant’s full name with his contact number and address.

- Information on compulsory motor liability insurance (date, number, validity period, type of vehicle).

- Reasons for contacting. You should indicate the details of the incident (circumstances of the accident, the cars involved) that caused the decrease in the value of the car.

- Damage size. Calculated based on the results of the examination.

- Request for payment of a refund under the UTS indicating the amount.

- Account details to which funds will ultimately be credited.

For reference!

The maximum refund amount under compulsory motor liability insurance in 2019-2020, taking into account the basic compensation and the technical insurance, cannot be higher than 400 thousand rubles.