Home/OSAGO/Increasing coefficient of MTPL after an accident

The law obliges citizens to purchase a compulsory motor liability insurance policy. Without it, you will not be able to get on the road while observing traffic rules. For insurers, selling a policy is an additional way to earn money. However, it is beneficial for organizations to only work with customers who do not have accidents. If an accident does occur, this will affect the cost of the MTPL policy. The insurance price can be adjusted depending on the number of accidents in the driver’s history by increasing the MTPL coefficient after an accident. In 2021, its value may change depending on the number of insurance claims.

What is KBM?

BMC or bonus-malus coefficient is an indicator that is used when calculating the insurance premium. There are 14 accident classes. Depending on them, a person may receive a discount or will be forced to pay more for the purchase of an MTPL policy. Initially, the indicator does not affect the cost of insurance. If a person has driven without accidents for a year, he is given a discount. It adds up. The maximum value of the indicator in 2021 may reach 50%. The opposite situation is also possible. If the insurance company suffered losses due to the fault of a citizen, the coefficient increases. As a result, the price of an MTPL policy may increase by almost 2.5 times.

Attention! If you have any questions, you can chat for free with a lawyer at the bottom of the screen or call Moscow; Saint Petersburg; Free call for all of Russia.

Insurance coefficients for road accidents

The OSAGO coefficient is established by Article 9 of the Federal Law No. 40 of April 25, 2002 On the Automobile Citizen. A whole list of indicators falls into this category. They are divided into two main groups - fining and rewarding. The first of them includes indicators designed to hold drivers who ignore the rules accountable. They are intended to encourage compliance with traffic rules. The second group includes coefficients that simplify the purchase of insurance for persons complying with traffic rules. The coefficients included in the category are aimed at reducing the number of accidents. In 2021, there are 6 main increasing coefficients:

- Kt. The level depends on the number of accidents occurring in the region where the driver is registered. Ordinary residents of small towns pay less.

- Book Depends on compliance with the terms of the insurance contract. If they are violated, this will entail an increase in the cost of the policy.

- Kvs. Depends on the age of the driver and his driving experience. The older the citizen, the lower the cost of issuing compulsory motor insurance.

- The KBM coefficient is allocated separately. It depends on the driver's accident level.

- KN —violation coefficient.

- KM - power factor. Depends on the strength of the car engine.

How is KBM calculated?

The bonus-malus coefficient in 2021 can be increasing or decreasing. It depends on the class of the car enthusiast. The easiest way to determine the value of the indicator is based on the table. Initially, the KBM is set at level 1. The driver is assigned class 3.

If a citizen does not violate traffic rules and does not take part in accidents, his MAC increases every year. As a result, a 5% discount is provided. The classes are indicated in the column on the left. So, if a person has been driving without incident for 10 years, he will be assigned class 12. The discount amount is displayed in the Impact on the insurance price column. Accident-free driving for 10 years allows you to receive a 50% discount.

A traffic accident will result in an increase in the MBI. Its level depends on the number of incidents in which the driver took part. Let's say the driver is assigned class 1. During the insurance period, 1 accident occurred. To understand how it will affect the price, you need to find your class and compare it with the Number of accidents column. It contains the letter M. Then you need to return to the Assigned class column and find the corresponding designation. It turns out that the price will increase by 145%.

| Assigned class | Indicator value | Impact on insurance price | Number of accidents in which the driver was involved during the insurance period | ||||

| No one | 1 | 2 | 3 | 4 or more | |||

| M | 2,45 | 145% | 0 | M | M | M | M |

| 0 | 2,3 | 130% | 1 | M | M | M | M |

| 1 | 1,55 | 55% | 2 | M | M | M | M |

| 2 | 1,4 | 40% | 3 | 1 | M | M | M |

| 3 | 1 | 0% | 4 | 1 | M | M | M |

| 4 | 0,95 | -5% | 5 | 2 | 1 | M | M |

| 5 | 0,9 | -10% | 6 | 3 | 1 | M | M |

| 6 | 0,85 | -15% | 7 | 4 | 2 | M | M |

| 7 | 0,8 | -20% | 8 | 4 | 2 | M | M |

| 8 | 0,75 | -25% | 9 | 5 | 2 | M | M |

| 9 | 0,7 | -30% | 10 | 5 | 2 | 1 | M |

| 10 | 0,65 | -35% | 11 | 6 | 3 | 1 | M |

| 11 | 0,6 | -40% | 12 | 6 | 3 | 1 | M |

| 12 | 0,55 | -45% | 13 | 6 | 3 | 1 | M |

| 13 | 0,5 | -50% | 13 | 7 | 3 | 1 | M |

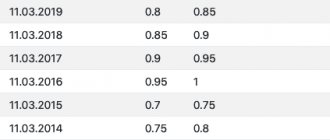

KBM standards in 2021

The main regulator of the “automobile insurance” is Federal Law No. 40-FZ “On OSAGO”. And the rules for this insurance are set by the Central Bank of the Russian Federation. By his Instruction No. 5000-U dated 12/04/18, from 04/01/19, the value of the KBM changes in the following order:

| KBM for the beginning of the year | How does the BMR change depending on the number of accidents? | ||||

| 0 | 1 | 2 | 3 | More than 3 | |

| 2,45 | 2,3 | 2,45 | 2,45 | 2,45 | 2,45 |

| 2,3 | 1,55 | 2,45 | 2,45 | 2,45 | 2,45 |

| 1,55 | 1,4 | 2,45 | 2,45 | 2,45 | 2,45 |

| 1,4 | 1 | 1,55 | 2,45 | 2,45 | 2,45 |

| 1 | 0,95 | 1,55 | 2,45 | 2,45 | 2,45 |

| 0,95 | 0,9 | 1,4 | 1,55 | 2,45 | 2,45 |

| 0,9 | 0,85 | 1 | 1,55 | 2,45 | 2,45 |

| 0,85 | 0,8 | 0,95 | 1,4 | 2,45 | 2,45 |

| 0,8 | 0,75 | 0,95 | 1,4 | 2,45 | 2,45 |

| 0,75 | 0,7 | 0,9 | 1,4 | 2,45 | 2,45 |

| 0,7 | 0,65 | 0,9 | 1,4 | 1,55 | 2,45 |

| 0,65 | 0,6 | 0,85 | 1 | 1,55 | 2,45 |

| 0,6 | 0,55 | 0,85 | 1 | 1,55 | 2,45 |

| 0,55 | 0,5 | 0,85 | 1 | 1,55 | 2,45 |

| 0,5 | 0,5 | 0,8 | 1 | 1,55 | 2,45 |

When does the OSAGO coefficient change?

The KBM coefficient can increase, decrease or remain at the same level. Its application is regulated by Appendix No. 6 to the Directive of the Central Bank of the Russian Federation No. 5000-U dated December 4, 2021. If a citizen does not get into an accident, the indicator begins to decrease. This leads to lower insurance costs. Accidents entail an increase in the CBM indicator. As a result, the price of MTPL will increase. However, there are cases when the coefficient remains at the same level. This is possible if the maximum discount level has been received. The accident will not affect the value of the KBM indicator in the following situations:

- MTPL insurance was purchased for a transit type vehicle;

- the MTPL policy has been issued for the trailer;

- the citizen is not to blame for the incident.

Please note

: The above rules do not apply to foreigners. If the case does not fall under the above list, the value of the compulsory motor liability insurance coefficient after an accident is adjusted in the standard way.

Increasing coefficient for compulsory motor third party liability insurance after an accident

Initially, the driver is assigned third class. It allows you to purchase an MTPL policy in 2021 at a standard price. If you manage to drive for a year without an accident, the class level increases. This allows you to count on a discount. The procedure is performed at the time of insurance renewal. The maximum discount level is available to persons who have reached class level 13. To get it, you need to renew your MTPL for 10 years and not get into an accident.

IMPORTANT

Every year without an accident allows you to count on a 5% discount. If the driver has not been involved in an accident within 10 years, insurance will be 50% cheaper. However, if at least one accident occurs, the CMV immediately becomes smaller. As a result, the price will increase. The class can be lowered by 2-7 grades. It all depends on the number of insured events during the reporting period. The more often you get into accidents, the lower the level of trust on the part of the insurer.

When the driving class drops below level three, penalties apply. This is reflected in the tariff. The cost of insurance can increase almost 2.5 times. The class cannot be lower than level M. If a citizen hopes to return to the standard fare, he must drive for at least 4 years without an accident.

Restoring KBM after an accident

If an accident occurs, there is a risk of losing not only part of the accumulated bonuses, but also completely losing this increasing coefficient. If the incident was not the driver’s fault, he will not lose the KBM.

In case of participation in a traffic accident as a result of non-compliance with traffic rules, inattentive driving, or driving under the influence of alcohol or drugs, the KBM will be lost. In addition, insurance after such events will cost much more.

The only way to restore the coefficient is to drive the car without accidents for a long time.

You can restore the KBM by contacting the insurance company, the Russian Union of Auto Insurers or the Central Bank. Private online companies and brokers are also engaged in the restoration of KBM.

How does the OSAGO coefficient increase after an accident?

The value of the indicator depends on the number of incidents that the person encountered during the validity period of the insurance policy. Each situation is considered individually. The decision to increase the value of indicators is made by the commission of the insurance company. It operates within the framework of the norms of the Civil Code of the Russian Federation, Federal Law No. 40 on OSAGO, as well as Federal Law No. 4015-1 On the organization of insurance business in the Russian Federation. If the standards are not observed, the citizen has the right to go to court and demand compensation for damage. However, this fact remains to be confirmed.

Newcomers are especially strictly controlled. If a citizen took part in one incident, he will be assigned first class. The KBM coefficient will drop to a level below average. The price of insurance will increase by 55%. If a driver is involved in two or more accidents, he is assigned class M. The coefficient increases to 2.45. When buying a policy next time, a citizen is obliged to pay 145% more than in the standard case.

If a person uses the services of one insurer for a long time, control is less stringent. Typically this is reflected in a discount for one year of perfect driving. If a person drove for 10 years without an accident, but during the insurance period was involved in an accident three times, he will be assigned a standard level. It should be taken into account that the value of the indicator reflects the number of accidents that occurred during the entire period of validity of the insurance policy, and not just incidents in one year.

How does the BCM change after an accident?

The KBM changes as a result of an accident only for the person responsible for the accident. Let's take a closer look at how exactly this coefficient grows.

For drivers with the lowest CBM scores, for a single accident for which they are at fault, the coefficient changes by one step. Conversely, for the highest values of BMI, if the driver is at fault in an accident, this indicator can soar by 5–6 points. The “bonus-malus” becomes unchanged at the minimum threshold. Here, even the absence of an accident does not make the coefficient below 0.5%.

The more insurance cases a motorist is at fault for, the worse it is for his insurance history and for KBM. Having become the culprit of more than three accidents, the policyholder will increase his BMR to the maximum - 2.45. That is, he will be forced to buy an MTPL policy at a price that is almost two and a half times more expensive than the face value.

The increased “bonus-malus” after an accident remains for one insurance period. With trouble-free driving, it will decrease annually and may again reach the lowest value of 0.5.

How to “protect” the KBM after an accident

The existing form of “motor citizenship without restrictions” can also help the unlucky driver. With such insurance, the BMR is always equal to 1 and does not change, even if the motorist is at fault for four accidents in one year. But there is one “but”! The cost of such an agreement is much higher. So, you need to calculate what is more rational to pay: a high coefficient or expensive insurance.

It is also possible next year not to include the driver who caused the accident on the list of those allowed to drive a vehicle. To calculate the cost of the policy, the number of road accidents only among drivers included in the insurance is taken into account.

How long does the increased MTPL coefficient last after an accident?

Attention

The validity period of the MTPL increasing coefficient after an accident reflects the principle of concluding a contract. Typically, insurance is provided for one year. The validity period of the coefficient will be identical to this period. When it is completed, the indicator will change. It may increase or decrease.

The norm is not always observed. Much depends on the insurer. Often organizations take advantage of the inexperience of owners. In order to continue to force the citizen to pay a large amount, the documentation deliberately does not indicate the validity period of the CBM. There are known situations where the indicator was overestimated by accident.

Experts advise keeping records yourself. To do this, you need to find out when the policy was issued and how long it will be valid. Additionally, information about the date of conclusion of the contract is required.

Increasing KBM OSAGO after an accident, if not at fault

Questions arise when the owner of the car was not driving, or the accident was not his fault. In the latter case, there is no change in the BMC. However, it will be necessary to prove that another person was the culprit of the incident. Typically, insurance organizations refuse to compensate for damage if there is indisputable evidence of the car owner’s guilt. To assert your rights, you must obtain a conclusion from law enforcement agencies. The evidence is also provided by the video recording. Therefore, experts advise installing the equipment even on old cars, the equipment of which does not provide for this.

Several drivers can be included in the insurance at once. In this situation, the increase in BMV will occur only for the person who was driving at the time of the incident. The norm applies if the citizen’s guilt is proven. The law does not allow increasing the value of the indicator if the traffic police representative has not confirmed that the driver’s actions resulted in the occurrence of the incident. If a person is involved in an accident through no fault of their own, the incident will not appear on the driving record. It is believed that it remains accident-free.

What is mutual guilt?

As a rule, in an accident there is one culprit whose actions or violations of traffic rules led to the incident. Sometimes there are cases in which violations of the rules are committed by both drivers, then the fault of both participants and damage to both vehicles is recorded. A double violation is recorded by state inspectors in a personal report for each participant in the accident.

The following items must be included:

- what rule did the driver break?

- punishment provided for such a violation by law.

How to bypass the MTPL increasing coefficient after an accident?

Not all drivers are willing to pay additional money for insurance. Therefore, attempts are being made to avoid an increase in the bonus-malus coefficient after an accident. Previously, the following methods helped:

- transfer to another insurance organization;

- concealment of information about the incident at the time of change of insurer;

- purchasing an MTPL policy for another person.

Usually the latter method was used. The trick worked if the policy was issued to several citizens at once. An increase in the indicator after an accident occurred only in the person who was driving at the time of the accident. Moreover, if the policy is issued to several persons at once, the maximum cost was set depending on the data of the drivers. To avoid increasing the price of insurance, individuals did not include the problem driver in the MTPL policy. In this situation, the coefficient did not change. This method was most suitable for married couples.

However, due to the creation of a unified RCA database, most of the above methods do not work. In 2021, the most reliable way to avoid increasing the compulsory motor vehicle insurance coefficient after an accident is not to participate in an accident. Insurers and authorized bodies monitor changes in the indicator. Frauds are monitored. A number of motorists claim that they managed to reset the indicator value. The action was completed without renewing the policy for a year. However, such situations are accidental. Information about the incident is entered into the general database within 15 days from the moment of the accident. Subsequently, it is enough to indicate the citizen’s ID number to find the data.

For your information

If a person wants to avoid a higher MLA after an accident, they can try to negotiate personal compensation for damages. In this case, the insurer is not contacted, and traffic police representatives are not called. The method is considered risky. Not every driver will agree to meet the culprit of the incident halfway. If the accident occurred due to the fault of another person, you need to understand that an oral agreement does not guarantee the provision of funds. The method is recommended to be used if the amount of the insurance payment is less than the amount of money that will have to be provided for the subsequent renewal of the policy.

Deliberate attempts to avoid increasing the BMV after an accident are punishable. If a person does this, he may be brought to administrative responsibility in 2021. In some cases, criminal penalties are applied.

How will the vehicle driver's vehicle change after an accident?

No organization operating in the auto insurance market would want to deal with a careless driver who continually endangers himself and other road users. Therefore, for each accident, insurers punish such motorists with a ruble, calculating the amount of the insurance premium taking into account the increased bonus-malus.

If at fault, how will the KBM change?

When a driver causes an accident, his insurance company pays compensation to the injured person. Consequently, she suffers losses, and this is unprofitable for her. In order to somehow compensate for the insurance payment for an accident, the insurer reduces the class of the car owner in the next insurance period. The BMI increases after an accident, and the cost of the policy after the accident increases accordingly.

Good to know! A large number of accidents negatively affects the driver's driving reputation. More than 3-4 accidents per year will lower its class to the lowest - class M. Not every insurer will want to get involved with a motorist who has a negative insurance history.

If it's not your fault

If the accident occurred due to the fault of another motorist, then the victim:

- receives compensation from the at-fault party's insurance company;

- does not lose a positive insurance history - his driving class does not decrease and his CBM does not increase.

But the culprit will have to restore the damaged car at his own expense and pay a large amount for insurance in the next period, since its class and bonus malus change.

If it is not the owner of the vehicle who is at fault, but the driver

What to do if you mistakenly increased your compulsory motor liability insurance ratio?

If a citizen moves to another insurance company, the CBM must remain at the same level. However, the insurer can take advantage of the driver’s inexperience and assign him a starting third category. The main argument is the lack of information about the citizen in the RSA database. If a person knows that he is entitled to a discount, the following actions are acceptable:

- personal request for information in the RSA database;

- visit to the previous insurer and obtain a certificate of cooperation;

- obtaining information from the Union of Insurers.

Nuances

The law does not allow insurers to independently change the BMR. If this happens and the organization’s actions are not justified, you can send a complaint. It is submitted to law enforcement agencies. However, you need to understand when an organization’s actions are legal. In this situation, it will not be possible to change the increasing coefficient. The law allows an organization to increase the price of compulsory motor liability insurance if:

- the citizen fled the scene;

- the early person flouted the rules and drove without insurance;

- false data about the characteristics of the accident were provided;

- at the time of the accident the person was under the influence of alcohol or drugs;

- the accident was caused intentionally.

If it is proven that the citizen is not the culprit of the incident, the MSC remains at the same level. If the policy is renewed for the next year, a discount must be provided.

| Question | Answer |

| When does the MTPL increasing coefficient change in 2021? | When renewing insurance. |

| Will the MBI increase if the driver is not at fault in the accident? | No, the indicator will remain at the same level. |

| How to avoid increasing the BMR? | Follow traffic rules and try not to get into accidents. |

| What to do if the MTPL ratio was increased by mistake? | Contact the previous company and get a certificate or check the RSA database yourself. The data is then provided to the new insurer. If he refuses to change the coefficient, legal proceedings can be initiated. An alternative is to send a complaint to the authorized body. |

Comments Showing 0 of 0

How does a traffic accident affect the CBM?

Understanding the basic provisions about the MSC, for many it becomes interesting, on what principle does this coefficient change in the event of an accident?

For convenience, there is a good table, thanks to which you can approximately see what coefficient will be taken into account when applying for the next insurance, which will be issued for the next year.

| Class/kbm | Surcharge/Discount | Number of insurance payments | ||||

| 0 | 1 | 2 | 3 | 4 | ||

| M | 145 | 0 | M | M | M | M |

| 0 | 130 | 1 | M | M | M | M |

| 1 | 55 | 2 | M | M | M | M |

| 2 | 40 | 3 | 1 | M | M | M |

| 3 | 0 | 4 | 1 | M | M | M |

| 4 | — 5 | 5 | 2 | 1 | M | M |

| 5 | — 10 | 6 | 3 | 1 | M | M |

| 6 | — 15 | 7 | 4 | 2 | M | M |

| 7 | — 20 | 8 | 4 | 2 | M | M |

| 8 | — 25 | 9 | 5 | 2 | M | M |

| 9 | — 30 | 10 | 5 | 2 | 1 | M |

| 10 | — 35 | 11 | 6 | 3 | 1 | M |

| 11 | — 40 | 12 | 6 | 3 | 1 | M |

| 12 | — 45 | 13 | 6 | 3 | 1 | M |

| 13 | — 50 | 13 | 7 | 3 | 1 | M |

Based on this table, we see that if the accident occurred in the third year and there was only one payment, the discount is canceled, and in the case of the policyholder's liability, the company will have to make a payment twice, and the price for the next policy will increase by 55%.

This memo should be kept by every car enthusiast who wants to save on an insurance policy.