The cost of MTPL consists of several components. Namely, tank tariffs and coefficients that apply to these tariffs. In order to understand what the price of insurance consists of, you should understand in detail the coefficients used.

Dear readers! Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem, please use the online consultant form on the right or call. It's fast and free!

What is KVS in OSAGO?

KVS in compulsory motor liability insurance is the coefficient of the driver’s age and experience. There are certain parameters for this coefficient:

- Namely, it will have an increasing rate if the person’s age is under 22 years and driving experience is less than 3 years. With such values, the VAC will be equal to 1.8.

- If the driver’s age is over 22 years and his experience is less than three years, then the FAC will have a value of 1.7.

- In the case where the age has not reached 22 years, and the work experience is over 3 years, then this coefficient will be equal to 1.6.

- Provided that the age is over 22 years of age and the experience exceeds 3 years, the FAC will be equal to 1.

Some nuances of KVS.

Questions often arise about age “discrimination” of the policyholder when calculating compulsory motor liability insurance. However, whatever you say, the 22-year limit is justified at least because it was introduced not by insurers, but by law. And as you know, “The law is harsh, but it is the law.” In addition, hand on heart, the incomplete legal capacity of persons under 22 years of age has long been generally recognized. This is confirmed by data from many special studies, as well as impartial statistics. For example, it has been proven that:

- Regardless of gender, persons under 22 years of age have significantly lower social responsibility indicators. Almost every one of us understands this, and the more we move away from this borderline period in our lives.

- Young people behind the wheel are much more likely to commit dangerous negligence, exceed the permitted speed limit, and generally act carelessly when driving. As a result, they become the perpetrators and victims of road accidents.

- They also have less ability to adequately assess the situation, which is aggravated by increased aggressiveness.

The main thing is that this problem is temporary, and therefore transitory. The longer you live (including through safe driving), the lower the FAC will be for you. It should be more offensive for women, for whom CASCO (vehicle insurance against damage, theft or theft) costs more than men.

A much more important question is from what date to count driving experience. Most people are of the mistaken opinion that the countdown should begin from the time when they received their driver’s license. But, according to Directive of the Bank of Russia No. 3384-U dated September 19, 2014, driving experience is counted from the date of receipt of the corresponding driving category.

When there is more than one driver

It is also a very common situation when several people can use one car. This is how it is often done in large families. In this case, the MTPL agreement cannot forget about any of those who are allowed to drive the vehicle. And it is clear that each of them has their own indicators of age and experience.

In such a situation, the coefficient of the driver whose coefficient is higher is used. For example, if among you there is a young person with little driving experience, the cost of insurance will be higher than without it.

Factors that influence the price of compulsory motor liability insurance

There is a certain algorithm for calculating the MTPL agreement. It is as follows:

- The base rate is taken. It can have different meanings depending on the type of vehicle and who owns it. Namely, a legal or natural person. It is worth knowing that the base rate is set by government decree and has a range. For example, the minimum base rate for category B is 3912 rubles, and its maximum value is 4118 rubles. These are amounts for individuals. If the owner is a legal entity, the rate will be different. And so on for each category of vehicle.

- Then the odds are applied to the tank bet. The original amount is multiplied by their value.

- The cost of an MTPL policy depends on which region of the Russian Federation the owner is registered in. This coefficient is determined by the payment index. There is a table that shows all regions of the Russian Federation, republics and territories. There is also a certain significance for cars whose owners are registered in foreign countries.

- For passenger cars, the cost of the policy is affected by their horsepower.

- Number of persons admitted to management. Namely, a limited circle of drivers, or an unlimited one. If the circle of those admitted to management is unlimited, then the insurance contract will cost 80 percent more.

- Bonus-malus coefficient. Accumulated discount under MTPL. For each accident-free year of driving, minus 5 percent is given. In the event of an accident, this criterion increases. How much the CBM will rise depends on the number of insured events. The maximum value is 2.5 and the minimum is 0.5.

- For trucks, the contract price is affected by whether they will be used with or without a trailer.

- Age and length of service of persons admitted to management. There are certain parameters when a multiplying factor is applied.

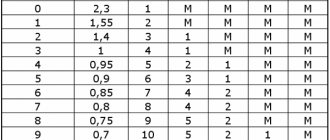

PIC table for compulsory motor liability insurance for 2021

| Experience | |||||||||

| 0 | 1 | 2 | 3-4 | 5-6 | 7-9 | 10-14 | More than 14 | ||

| Age | 16-21 | 1,93 | 1,9 | 1,87 | 1,66 | 1,64 | X | ||

| 22-24 | 1,79 | 1,77 | 1,76 | 1,08 | 1,06 | 1,06 | X | ||

| 25-29 | 1,77 | 1,68 | 1,61 | 1,06 | 1,05 | 1,05 | 1,01 | X | |

| 30-34 | 1,62 | 1,61 | 1,59 | 1,04 | 1,04 | 1,01 | 0,96 | 0,95 | |

| 35-39 | 1,61 | 1,59 | 1,58 | 0,99 | 0,96 | 0,95 | 0,95 | 0,94 | |

| 40-49 | 1,59 | 1,58 | 1,57 | 0,95 | 0,95 | 0,94 | 0,94 | 0,94 | |

| 50-59 | 1,58 | 1,57 | 1,56 | 0,94 | 0,94 | 0,94 | 0,94 | 0,93 | |

| More than 59 | 1,55 | 1,54 | 1,53 | 0,92 | 0,91 | 0,91 | 0,91 | 0,90 | |

In September 2021, the KVS table was updated . The number of gradations by age and accumulated experience has been increased (there are now 58 variations). For experienced drivers, the cost of the policy decreased by 7%, for young drivers without experience it increased by 6%.

How to calculate your age and experience coefficient?

This coefficient is calculated quite simply. Namely, if a person is under 22 years of age and his driving experience is less than 3 years, then an increasing coefficient of 1.8 is applied to the calculation of the compulsory motor liability insurance policy.

If the driver is over 22 years old and has less than 3 years of driving experience, then this coefficient is 1.7.

In a situation where the driving experience exceeds three years, and the driver is under 22 years old, then the FAC will be equal to 1.6. An increased value will not be applied if the person admitted to driving has more than 3 years of driving experience and his age exceeds 22 years.

Where and how is KVS used?

It is used in conjunction with the other coefficients, which make up the formula for calculating the cost of an MTPL policy: TB, CT, KBM, KO, KVS, KM, KN, KP. Each of these values is calculated based on the driver and vehicle data, after which all the results are multiplied. All values, except TB (basic tariff), are additional (multiplying) coefficients that can either reduce the final cost or increase it.

- TB (basic tariff) gives a specific value for a particular type of vehicle: motorcycle, car or tractor. It is important to note that the last category of transport includes an ATV, although it is often placed in the group of motor vehicles.

- CT (territorial coefficient) depends on the frequency of accidents in a certain region, as well as on the number of population and transport in it. In dangerous regions of the country it can take a value of up to 2, and in safe regions where traffic is not very strong - up to 0.5.

- KBM (bonus-malus) – what is KBM? This is an incentive for drivers who follow the rules and do not get into accidents or traffic accidents for a certain period of time, but it is also a punishment for violators. According to the KBM, the driver is assigned a group (13th - maximum), and from it the value of the coefficient is determined: for example, group 11 - 0.6, that is, a 40% discount. But there may be a fine in the form of an increased coefficient if the driver has an accident, up to 2.45, that is, plus 145% of the cost of the policy.

- KO (limitation of the number of persons) - under standard conditions, if only one driver is indicated in the policy, then this value will be equal to 1, but if several persons are included in the policy, it can become equal to 1.8.

- KVS (age-experience) - this coefficient is responsible for the driver’s experience and age.

- KM (engine power) is a control for the engine power of the insured vehicle. If it is less than 50 horsepower, then the value will be 0.6. The maximum possible KM is 1.6, it is considered with an engine power of 150 horsepower.

- CN (violations) - if the driver has not previously committed violations related to insured events and road accidents, then this factor will not affect him; in other cases, there will be a higher amount for the compulsory motor liability insurance policy.

- CP (validity coefficient) - the longer the period for which the policy is issued, the greater this value. It is important that the policy cannot be valid for longer than 1 year (in this case the value will be 1), then it must be purchased again.

Help : the cost is calculated using the formula: TB*KT*KBM*KO*KVS*KM*KN*KP, for example, 1673*1.3*0.8*1*1*0.9*1*1 = 1565 rubles , which will need to be paid for the policy.

Is it profitable to buy a policy for young drivers?

You should know that according to the legislation of our country, every vehicle owner must have a compulsory insurance contract. And if the car is driven by a young person, then it should be included in the insurance.

Its cost to such a person will be much more expensive. Namely, 60 or 80 percent. There is an opinion that if you make an unlimited number of drivers, then insurance will be cheaper. This is not true, since in this case the cost of the policy will be the same as with a young driver.

Unlimited insurance

An MTPL policy for an unlimited number of drivers is issued in the same way as a standard policy. It allows any person who has a driver’s license with an open category for this vehicle to drive an insured car, motorcycle, ATV or other vehicle, but it will no longer be possible to take into account his experience, so the FAC in this case is equal to 1.

Obtaining this policy greatly simplifies the operation of a vehicle in a large family (if the vehicle is driven by more than 5 people) or a company (MTPL is issued to a legal entity), but for this you will have to pay a higher price for the policy, since in this case the KO value will be equal to 1.87 . The advantages of unlimited insurance are the following:

- If a driver in an insured vehicle gets into an accident, the insurance company will not be able to refuse payment, citing the fact that the driver was not included in the policy, but, of course, the elementary rule - having a driver's license - must be followed in any case.

- Any number of people can operate a vehicle - this is convenient for both companies and large families.

- There is no need to calculate the FAC for each driver and then enter them into the MTPL policy for this vehicle.

Useful tips when applying for a policy

- Now many insurers sell additional contracts. You should know that every policyholder has the right to buy compulsory motor liability insurance without any other insurance products.

- It is also possible to issue an insurance contract for a period of use of 3 months or more. In this case, the cost will be 50% of the total contract amount. At the end of this period, a person can renew his insurance.

- When concluding an agreement, you can make one list of persons admitted to management. And then add to it, or exclude someone.

- If the car is more than three years old, then a technical inspection is a mandatory requirement. However, its term may expire the next day. The main thing is that it is in effect at the time of purchase of MTPL.

- A person has the right to choose the insurance company with which he wants to sign a contract.

To calculate the cost of compulsory motor liability insurance, several factors are taken into account. The age of the driver and his driving experience significantly affect the price of insurance. Therefore, if a young driver does not drive, then you should not just include him in the policy.

If the need arises, you can add to the list of persons admitted to management at any time during the term of the agreement. If any violations arise, you can contact the RSA to resolve the problem situation. The central bank is also the supervisory authority of insurers.

How is the cost calculated?

Calculation is possible in two ways - in a special online calculator or manually using a formula. The cheapest insurance will be for adult drivers with a long accident-free driving record.

Manual calculation

The cost of the MTPL policy is calculated using the formula = base rate x KTxKBMxKVSxKOxKMxKS

Explanation of the symbols of the coefficients:

- CT - territorial;

- KBM - accident-free operation;

- KVS - age-experience;

- KO - unlimited or limited insurance;

- KS - power;

- KS - seasonal operation.

If they plan to include several drivers in the policy, then the highest FAC value is taken to calculate the price. Let's look at it with an example. For driving a passenger car with a 106 hp engine. With. (KM = 1.2) 2 drivers were allowed (age 35, 10 years of experience and age 55, 20 years of experience) with accident-free driving (KM = 0.95). Of the two FACs (0.95 and 0.93), we choose the first option. The territory of primary use of the machine is Murmansk (CT = 2.1). The policy is issued for a year (KS = 1), limited insurance (CR = 1).

The cost of the policy at the minimum base rate = 2471X2.1X0.95X0.95X1X1.2X1 = 5619 rubles.

The cost of the policy at the maximum base rate = 5436X2.1X0.95X0.95X1X1.2X1 = 12363 rubles.

Expert opinion

Ivan Strahovsky

Insurance expert

OSAGO calculator

This calculation method is not reliable. Each insurance company sets a base rate within a legally established range of values . Insurers are also allowed to apply additional criteria, determined independently, when determining the price of a policy. For example, in some insurance companies the size of the base rate is influenced by the sales channel (office, official website, agent, etc.). During the reform, the calculation system lost its unified character and became more individual.

OSAGO online calculator

Each insurance company is obliged to provide current and potential clients with the opportunity to apply for electronic compulsory motor liability insurance. The official websites of insurers provide special calculators for calculating the price of a policy. The visual design may differ, but the essence is the same.

For the calculation you need to provide the following data:

- vehicle category (truck, bus, passenger car, motorcycle, etc.);

- technical characteristics (make and model, year of manufacture and power in hp);

- vehicle registration data (registration number and VIN, PTS or STS);

- purpose of use (renting, driving lessons, personal, taxi, etc.);

- passport details of the policyholder;

- a list of approved drivers (all driver's licenses are required), not required when taking out an unlimited policy;

- period of operation of the machine (3-12 months);

- region of primary operation of transport (coincides with the address of permanent registration of the owner).

If you receive a new license during the year, then when calculating it is important to check the correct application of the KBM (the discount accumulated for accident-free driving should not be reset to zero).

If you make a calculation in your personal account on the insurer’s website, it is saved. In most cases, authorization on the site is required. Calculators are also presented on aggregator sites, on the RSA website and on specialized resources. You can do without registration, but the calculation is not always accurate. But you can compare the cost of the policy from different insurers.

OSAGO calculator online

Didn't find the answer to your question? Find out how to solve exactly your problem - call right now: +7 (Moscow) +7 (812) 309-53-42 (St. Petersburg) It's fast and free!

Free online consultation with a car lawyer

Didn't find the answer to your question? Find out how to solve exactly your problem - call right now: +7 (Moscow) +7 (812) 309-53-42 (St. Petersburg) It's fast and free!

Whose FIC is taken if several people are insured?

Recently, MTPL insurance policies, which include several people, have become quite common. For example, a husband purchases a car for his wife, who has just received a driver’s license, and when registering, he includes himself in the insurance so that he can legally drive the car during family trips.

How is the FIC calculated in this case, since the husband already has extensive experience in driving a car, and insurance for his wife will cost a “big sum”. Let's figure it out.

As a general rule, if several motorists are allowed to drive a vehicle, then a PIC is appointed, which correlates with the number of years and experience of the youngest and most inexperienced driver. Therefore, before taking out MTPL insurance, it is imperative to study the question of how to find out your FAC. And if there are several cars in the family, then it makes sense to allow the youngest car enthusiast to drive only one car.

How can PIC influence the cost of compulsory insurance?

KVS is reflected in the price of the MTPL policy as follows:

- For citizens who are between the ages of eighteen and twenty-two, insurance costs much more than for those people who are older than the specified limit (with the same driving experience).

- For motorists with less than and more than three years of driving experience, different rates apply, which also affects the amount of money that will have to be provided for the insurance policy.

It is important to note that for PICs there are certain age and experience restrictions, upon reaching which the coefficient turns out to be equal to one. Now let’s find out how to determine the indicator in question.

Additional calculation features

What is PIC in insurance when making additional calculations?

FAC is an indicator indicating the degree of risk of getting into an accident and damaging the vehicle if the motorist is an experienced person or, conversely, an inexperienced driver. Considering that the coefficient in question is of great importance when calculating the price, you need to know about some nuances that help to correctly determine the value:

- You should base your experience indicator on your driver’s license, which indicates the year the document was originally issued. If the license was issued more than two years ago, then it is necessary to accurately calculate the period, paying attention to the date, that is, the specific day the driver’s license was issued.

- You should be able to distinguish between the values of CBM (“bonus-malus”) and CBC. While the first indicator makes it possible to adjust the cost based on previous driving information, the second value remains unchanged, even despite the degree of caution and accuracy behind the wheel.

- If there are several drivers on the list of permission to drive a car, the PIC in the MTPL policy is awarded according to the maximum value of one of those who were mentioned in this list.

Young and inexperienced driver

Particular attention is paid to this indicator when the driver is quite young and inexperienced. As soon as his age exceeds twenty-two years, and his experience crosses the three-year mark, this value will no longer have a significant impact on the price of insurance. Such calculations, along with assigning a PIC, are applicable in situations where car owners limit the right of access to several persons (no more than five people).

In order to possibly reduce the price of insurance in the future, it is recommended to use policies with limited admission. This makes it possible to include a KBM reduction factor, provided that the driving has been accident-free for several years. When it is not possible to take out a policy with restrictions, you should learn about the nuances of unlimited use of the definition of PIC in insurance. Not everyone knew what it was, but we figured out these concepts.