The introduction of compulsory motor liability insurance into the insurance market has caused a lot of conflicting opinions, although it is successfully practiced all over the world. The subject of insurance in it was property interests related to the risk of liability of vehicle owners.

The introduction of compulsory motor liability insurance was dictated by the need for a social measure focused on the formation of financial guarantees to cover losses in the event of damage, and therefore is a financial instrument that increases road safety.

What it is

Compulsory motor third party liability insurance for vehicle owners is one of the types of insurance provided for citizens of the Russian Federation.

Upon its acquisition, the insurance company assumes obligations to compensate losses to injured persons as a result of the damage caused within the limits of the assigned insurance payment.

In this case, the amount of the insured amount is:

| for injury caused to the life and health of any victim | 160 thousand rubles |

| for damaged property under a policy purchased from the beginning of October 2014 | 400 thousand rubles |

The MTPL policy is stored together with transport documents and is presented to the traffic police inspector upon his first request. If the driver cannot present it to the road safety inspector for any reason, then he has the right to seize the car and send it to a impound parking lot.

The policy does not guarantee protection in case of vehicle theft or damage. Upon expiration of the policy, it is necessary to keep it for five years, as it will affect the cost of insurance under compulsory motor liability insurance in the future.

The essence of auto citizenship

Let's look at this in more detail. Why do you need auto liability insurance? What does it give? It is known that responsibility for damage caused usually lies with the person responsible for it. This is material civil liability. The defendant bears a loss that is equal to the damage he caused. As for compulsory motor liability insurance, we are talking only about financial liability. The motor vehicle has nothing to do with criminal law.

You may be interested in: OSAGO policy: how to get it, type of vehicle, rules for calculating the coefficient and insurance tariff rate

For all types of subjects there is a constant financial liability as a potential culprit to a potential victim. Under certain circumstances, any citizen can cause harm to another and must be held accountable for it.

What do insurance companies do? They insure risks associated with damage to property, and in the case of auto insurance, damage to a vehicle. In this case, it is not the possibility of causing harm that is insured, but the possibility of financial liability to the victim. This means that the harm caused to the victim does not cause material damage to the perpetrator of the incident. His liability is insured and will be paid by the insurance company. Many car enthusiasts understand this point very vaguely.

OSAGO refers to this type of insurance. Such a policy covers possible losses of the culprit of the accident that may arise when compensating the injured party. However, this only applies to cases where the damage was caused by a car. Now you have a rough idea of what OSAGO means. When this policy was introduced, how to properly issue it - we will consider further.

Law on compulsory motor liability insurance

The MTPL law and rules regulate the standards for assigning compensation to the party who suffered losses as a result of an insured event.

Insurance companies are obliged to comply with the rules and the law when concluding a contract for compulsory motor liability insurance, otherwise you may be subject to administrative penalties.

Every person who drives a vehicle is required to have an MTPL policy. If the driver does not have a compulsory motor liability insurance policy, then administrative liability is applied to him in the form of a fine, and the car is not registered with the traffic police.

The personal data of the driver of the vehicle is entered into the policy; if there are several of them, then the inscription “without restrictions” is affixed.

Current legislation provides for an increase in the amount of the insured amount through the conclusion of an agreement in the form of Voluntary Civil Liability Insurance, abbreviated as DSAGO.

This service is provided by many insurance companies. According to DSAGO, an additional payment is made, which allows you to increase the basic insurance amount.

The state regulates the cost of the MTPL policy, introduces restrictions on the amount of payments, which makes it possible to establish a guaranteed low cost of insurance and the obligation to make payments when an insured event occurs as a traffic accident.

Flaws

In what year was compulsory motor liability insurance introduced and when will the process of settling motor third party liability insurance be completed? Currently it is at the stage of active reform. After this, insurance should become a reliable guarantee of compensation for harm to victims in an accident and minimizing problems for the culprit. To date, the system has not yet been fully debugged and is susceptible to the construction of discreditable schemes.

Let's look at the main disadvantages:

- Artificially lowering the amount of insurance compensation: almost all insurance companies are prone to this behavior to one degree or another.

- Imposing additional services: often they are completely unnecessary for the driver, and the cost of the policy is significantly increased.

- Taking into account the wear of parts required for replacement: there is also a high probability of fraud here.

- Unreasonable underestimation of insurance points: affects the cost of insurance for the driver. Unfortunately, such cases are not uncommon.

- The issues of compensation for harm to life and health have not been sufficiently developed.

- Low payout limits compared to Western countries.

- High probability of purchasing counterfeit policies.

- Lack of strict control over insurers by the state. This allows insurance companies to exploit legal cases to make a profit.

Many car enthusiasts also consider the high cost of the policy to be a disadvantage. However, it is worth noting here that the reimbursement limits have also been increased.

Registration procedure

The execution of a compulsory motor liability insurance agreement is carried out in several ways, including:

- at the office of the relevant insurance company;

- in a car showroom, car market, mobile auto insurance points located in the traffic police area;

- on the official websites of insurance companies.

Often, insurance companies work without clear time limits. They deliver the policy to a place suitable for the client at the time appointed by them.

Insurance brokers strive to help clients; they select the best options that meet the client's requirements.

Registration is carried out in the following sequence:

- an application is filled out indicating the intention to conclude a compulsory motor liability insurance agreement;

- the required documents are submitted to the insurance company;

- the data specified in the application is verified;

- if desired, the policyholder checks the insurance policy;

- negotiations are carried out, on the basis of which an agreement is concluded, certified by the signatures of the parties;

- The policy is paid for and the receipt is presented to the company.

The package of documents is presented in person and sent by email. Payment for the policy is made in cash or by bank transfer, depending on the company’s conditions; there are no special requirements for filling out the application form.

Find out how to get an MTPL policy from VTB in the article: MTPL VTB.

You can sample the MTPL agreement.

What documents are needed

To conclude a compulsory motor liability insurance agreement, the owner of a vehicle needs to submit a package of documents to the insurance company, which includes:

- an application filled out on a unified form;

- passport or other document proving the identity of the policyholder;

- certificate of vehicle registration, that is, its technical passport;

- vehicle technical inspection certificate;

- driver's license or a copy thereof of persons entitled to drive a car;

- documents certifying the driver’s right to drive a vehicle, provided that certain persons are allowed to drive it;

- if you have a policy that has expired.

Each policyholder is responsible for the documents provided; they must be in full and contain reliable information.

It will cost more for a reckless driver

The main factors in determining the insurance rate are the driver’s experience and driving culture. Photo: Alexander Korolkov/RG

Simultaneously with the law, a directive from the Central Bank will come into force, according to which the tariff corridor within which insurance companies can set the cost of a policy will be expanded. The values of the coefficients are also clarified, including by age and length of service. Thanks to the latter, insurance will become cheaper for experienced drivers over 59 years of age. In general, car owners will begin a new life with personal tariffs.

Now, given the existing tariff corridor, insurers can set a tariff for the region as a whole. And it doesn’t matter how this or that car owner drives if he lives in this region.

RG experts discuss the practical application of legislation in the “Legal Consultation” section. You can ask your question here

If a region makes a loss, then all car owners living in it receive an increased price for an MTPL policy. From August 24, the situation will change. The tariff will be set personally for each car owner.

Auto insurers will use additional factors that they establish independently.

But these factors, which they will use when setting a rate, must be published on the insurance company's website. It can be anything: color, make of the car, its mileage, marital status of the car owner, presence of children of the driver, installation of telematic devices on the car... The main thing is that the influence of these factors is confirmed by the company’s actuarial calculations.

The draft instructions of the Central Bank establish factors that insurers will not be able to use to change the tariff. These include nationality, race, language, religion and official status.

Drivers whose licenses have been revoked will face the maximum tariff. We are talking about those who have been deprived of their license for driving while intoxicated, or who have refused a medical examination. And also for those who have been deprived of their rights for leaving the scene of an accident or causing an accident in which people were injured or died.

Another new factor influencing the tariff increase is repeated gross violations of the rules during the year. Namely, driving through a prohibiting traffic light or a traffic controller’s gesture, exceeding the speed limit by more than 60 km/h, or driving into oncoming traffic. But provided that these violations were detected by a traffic police inspector on the road, and not by automatic photo and video recording cameras.

In order to provide careful drivers with a higher discount, and reckless drivers with maximum coverage of their risks, the Central Bank is expanding the tariff corridor. For different categories of car owners. And the expansion is different. For owners of passenger cars - individuals, the limits will be expanded by 10 percent. If now the base tariff for them is from 2746 to 4942 rubles, then it will become from 2476 to 5492. For owners of cars - legal entities, the tariff corridor will expand by 20 percent, both up and down. It will be just as much wider for truck owners. The corridor will be slightly changed for owners of buses, trolleybuses and trams: the lower limit will be lowered by 5 percent. The top one will remain the same as it is now. And for taxi owners, the upper limit will rise by 30 percent. The lower one will drop by the same amount.

The age-experience ratio will change in accordance with the instructions of the Central Bank. For drivers aged 22 to 24 with 3 to 4 years of driving experience, it will increase. Instead of today's 1.04, it will become 1.08. For drivers over 59 years of age with more than 3 years of driving experience, the coefficient will decrease. For those with more than 14 years of experience, the coefficient will become 0.90 instead of 0.93 today.

It is expected that insurance will become cheaper for almost 80 percent of motorists. But time will tell.

Photo: RG infographics/ Anton Perepletchikov/ Vladimir Barshev

Is it possible to extend the policy?

The MTPL agreement is extended for the coming year at the request of the policyholder. If he intends to terminate the contract, he must notify the insurance company of his intentions before the expiration of the contract, for which he is given two months.

A contract with an extended period cannot be terminated within 30 days due to late payment of the insurance premium for the next year.

When the contract is extended for a new term, its validity is paid in accordance with the tariffs established by the rules at that time.

History of the origins of car insurance

2021 marks the 120th anniversary of the first American auto insurance policy. Travelers Insurance Company, a well-known insurance company in the states, entered into a car insurance contract with Dr. T. Martin. The conditions were simple: for 12 and a quarter dollars, the policyholder was guaranteed a payment of 5 hundred dollars if his car was damaged in a collision with a horse-drawn vehicle. Since almost the entire population of America traveled on horses, and cars were purchased by wealthy citizens, a similar accident in 1898 was very likely.

At that time, victims of horseless carriages had already appeared, and one of the accidents, which ended in death, made it into all the newspapers. In the summer of 1896, a car at a speed of 6 km/h hit and killed a confused woman. The cause of the accident was not the speed of the car, but the limited visibility for the driver due to horse-drawn carriages and the shock of the lady who saw the carriage without a horse for the first time. After a long trial, the judges agreed that there was an accident, but many motorists thought about safety on the road.

The American's insurance was his own idea, as well as the result of simple calculations: in the USA, there were 4 thousand cars for every 20 million horses. The example of a resourceful doctor did not become contagious. It took about 30 years for mass production of cars to be established at Ford factories. In the 20s of the last century, the car ceased to be a rarity and turned from a luxury item into ordinary transport. Massachusetts authorities in 1925 legalized compulsory auto insurance, and compensation was received by the injured party, i.e. insured the motorist's liability to pedestrians and other road users. It was still possible to insure the car, but it was not necessary. The legislative initiative was accepted with enthusiasm by car owners, since cars were still expensive and drivers had little experience.

European countries followed the example of the United States, and by the middle of the last century, almost all Western European countries had laws on compulsory car insurance. Austria introduced civil liability insurance for motorists in 1929, and a year later a similar bill was approved in the UK.

The car became a means of transportation across borders, and there was a need to legalize a universal car license that would be valid throughout Europe. The Green Card has become an insurance policy that has guaranteed payments in any European country for more than 50 years. The policy got its name because of the light green color of the forms that are issued to drivers.

Repair according to the policy

According to the innovations in the norms of legislative acts, owners of vehicles that have lost their original appearance are offered, in exchange for monetary compensation, to carry out repair and restoration work at the expense of the insurance company.

Owners have the right to choose their refund. If he accepts the offer, he is given a referral for 20 days to a service station with which the company has an agreement.

But in practice, some problems regarding payment often arise between the owner of the vehicle and the management of the service station.

Technical service centers charge a price significantly higher than the insured amount and the owners have to pay from their own funds.

In addition, there is no guarantee that the service station will be able to satisfy the requirements of the policyholder at the proper level by performing quality repairs. Owners should consider the offer before agreeing.

Dynamics of the MTPL market in Russia over five years

The table below shows statistics on the volume of premiums collected and payments made under MTPL for the last 5 years - from 2021 to 2020.

| Period | Volume of signed premiums, million rubles. | Volume of payments, million rubles. | Paid claims ratio |

| 1H 2016 | 113,755 | 77,464 | 68% |

| 2H 2016 | 120,614 | 95,181 | 79% |

| 1H 2017 | 109,192 | 103,581 | 95% |

| 2H 2017 | 112,884 | 71,935 | 64% |

| 1H 2018 | 107,302 | 66,550 | 62% |

| 2H 2018 | 118,663 | 71,352 | 60% |

| 1H 2019 | 101,588 | 71,341 | 70% |

| 2H 2019 | 113,361 | 71,038 | 63% |

| 1H 2020 | 102,961 | 67,999 | 66% |

The graph above shows that the maximum growth rate of insurance premiums traditionally occurs in the second half of the year, which is associated with a seasonal increase in the level of insurance sales in the fourth quarter during the most emergency period of the year.

For the period under review from 2021 to the 1st half of 2021, the highest collections by gross revenue in the insurance market for compulsory motor third party liability insurance were observed in the second half of 2021 (120.6 billion rubles), however, against the background of the expansion of the tariff corridor and the liberalization of tariffs, a downward trend has emerged from 2021 fees for compulsory motor vehicle registration. In the first half of 2021, the indicator traditionally returned to a lower level, but increased by 1% compared to the same period last year, reaching 102.9 billion rubles.

Payments show slightly different dynamics: until the 1st half of 2017 (inclusive) there was a significant increase in loss ratios and the volume of payments, however, from the 2nd half of 2021, the level of payments stabilized in absolute terms in the range of 67 - 72 billion rubles, which was partly due

- with correctly configured customer segmentation by insurance companies by region;

- the introduction of “in kind” payments under compulsory motor liability insurance in the form of sending victims of road accidents for repairs at a technical service station (STS) of the “insurer” (STS with whom the insurance company had an agreement to provide repair services), instead of paying money;

- creation of unified PCA tables on the average cost of standard hours in each region, recommended when calculating insurance payments for this mandatory type, and the average cost of spare parts for cars.

All these factors significantly influenced the improvement of the financial results by type, and also made it possible to reduce the risks of insurance fraud, legal costs with auto representatives, stabilized and even ensured a reduction in the average amount of payments, and ensured that the loss ratio in the market as a whole fluctuated in one understandable range.

Extended insurance

An addition to compulsory insurance is DSAGO, the amount of the insured amount of which is established by the owner of the vehicle. However, some insurance companies have restrictions on it.

To expand by registering a DSAGO, you must present a valid insurance policy, a vehicle registration certificate, and information about the number of people allowed to drive it.

Its cost varies; it is set by insurance companies, but usually it ranges from 0.15 to 0.5% of the basic sum insured.

When preparing it, the following are taken into account:

- driver age;

- number of persons driving a car;

- car model;

- year of car manufacture;

- engine power;

- basic amount of the insured amount.

When purchasing both forms of insurance, companies provide significant discounts. Concluding a DSAGO agreement is beneficial for young drivers with little driving experience and people who prefer high-speed driving.

Some insurance companies offer additional services to an extended MTPL policy, for example, car servicing by an emergency technician.

Pre-trial claim

The Law on Compulsory Motor Liability Insurance in its provisions provides, namely in Article 16.1, for the filing of a pre-trial claim against the insurer if disagreements arise regarding the implementation of payments or a refusal to make a payment is received from the insurance company. The measure came into force in September 2014.

A statement of claim containing a claim is filed with the court after 20 working days, which are allotted for making insurance payments, if:

- the company did not pay the due compensation within the time limits established by the regulations;

- violations were committed, for example, the insurance company refused to pay or underpaid the insured amount.

The application must describe the situation in detail, justifying the claim with references to regulations.

The result of the MTPL reform in 2014

Summing up, I would like to note that after the reforms of 2014, the MTPL policy became more expensive , but at the same time the amount of payments on it was increased. Also, the government decree changed the procedure for registering road accidents using video recorders to receive compensation, which applies to some regions of Russia for those who issued compulsory motor liability insurance after October 1, 2014.

According to the new Amendments, the requirements for policyholders have been tightened. The period for payment of compensation from September should not exceed twenty days, otherwise the company will be forced to pay a penalty. A penalty has been introduced for failure to indicate the reasons for refusal to pay compensation.

Trailer insurance

There is no clear answer to the question about the need to draw up an MTPL agreement for a trailer. On it, disagreements arise between traffic police officers and vehicle owners, despite the existing amendments introduced to the law on compulsory motor liability insurance since March 2008.

According to the introduced standards, there is no need to conclude an agreement for a trailer installed on a passenger car.

However, it must be issued mandatory for trailers that are attached to:

- passenger cars owned by legal entities;

- trucks with different load capacities;

- motorcycles, scooters.

The cost of a trailer policy is calculated taking into account coefficients - territorial and vehicle use.

In what year did it appear and become mandatory in the Russian Federation?

The history of OSAGO insurance dates back to the end of the 20th century, when it received the status of compulsory. In the 1920s, there were too few cars in Russia for a car insurance initiative to be considered and approved at the state level. Only in the late 60s the number of cars increased so much that the issue of insurance was discussed at the level of the Council of Ministers.

In 1984, the Resolution “On measures to further develop state insurance and improve the quality of work of insurance bodies” was legislatively approved, which became the basis for the creation of “auto-combi”.

This is an insurance contract drawn up by a citizen on a voluntary basis, and the object of insurance is not only the car, but also passengers and their belongings .

Further development of car insurance took place in Russia. In what year did the introduction of compulsory motor liability insurance policies begin and when were they actually introduced, that is, “automobile insurance” became mandatory?

In 1991, CASCO was introduced on a voluntary basis, but it was not widely used. Since 1993, draft laws on compulsory auto insurance began to be sent to the State Duma .

Employees of the Russian Insurance Supervision and the Department of Transport were preparing a draft of the corresponding legislative act. The period of consideration, study and integration of the law was quite long; the act came into force only in the summer of 2003, when compulsory car insurance was introduced, and implementation was carried out in several stages.

How is damage assessed?

If there has been a traffic accident, you must immediately call the traffic police service.

To receive compensation for damage caused to property, you must submit the following documents to the insurance company where the MTPL agreement was previously concluded by the culprit of the accident:

- a certificate received from a traffic police inspector confirming the accident;

- a certificate stating that no criminal case has been initiated;

- notification that a traffic accident has occurred.

The insurance company must commission a technical examination to determine the extent of the damage. An independent expert examines the car, collects information about the incident, draws up a report and submits it to the insurance company. 20 calendar days are allotted for drawing up the act.

The victim provides a car, the required documents, and bank details where the insurance amount will be transferred upon completion of all procedures for its intended purpose.

As a result of the examination, it is established:

- the exact amount of money spent on repair and restoration work to bring the car into a state of serviceability;

- the cost of spare parts and materials required for replacement;

- deciding on the feasibility of carrying out repair work;

- full assessment of defects received by the car as a result of an accident;

- calculation of damage for loss of marketable value in accordance with the rules on compulsory motor liability insurance.

An independent examination must be carried out within five working days from the date of receipt of the package of documents. It is carried out with the participation of persons who were involved in an accident and an agent of the insurance company.

Advantages

Let's take a closer look at them. What has changed with the introduction of OSAGO? When a compulsory auto liability insurance policy was introduced, the process of resolving controversial situations in the event of road accidents was significantly simplified. What are the main advantages of such a system:

- The insurer pays the blame for the policyholder. Having a car license gives the driver a guarantee of the safety of funds in the event of an accident due to his fault. This is an indisputable plus that makes life much easier for the policy owner.

- Guarantee of receipt of insurance payment. In many cases, after an accident, the victim is spared the problems associated with collecting compensation from the culprit. The money comes in pretty quickly. Damage under compulsory motor liability insurance is paid even to an uninsured person. The main thing is that the person responsible for the accident has an insurance policy.

- Increased security level. Auto liability insurance encourages drivers to follow traffic rules. This saves people nerves, money and effort, and also helps preserve health and life.

It is also worth noting that with the introduction of compulsory motor liability insurance, it was possible to significantly relieve the workload of the courts and other government agencies involved in the settlement of disputes regarding road accidents. The bulk of compensation is now regulated only within the framework of compulsory motor liability insurance. In addition, despite the rapid increase in the number of cars, the number of accidents is under control.

What is Direct Claims Settlement?

In the event of an insured event, the injured party has the right to contact the insurance company where he has a valid policy.

The possibility of direct settlement of losses is provided exclusively:

- in case of damage to property as a result of an accident, there are no victims;

- There are two vehicles in a traffic accident, the owners of which have compulsory motor liability insurance policies.

However, there are restrictions related to the guilt of both drivers; the accident did not involve a collision of vehicles.

Rating of insurance companies

Independent examination of insurance companies is carried out by the following organizations:

- The RA expert makes an assessment taking into account the location, amount of capital, client base, percentage of positive and negative phenomena;

- NRA, the National Rating Agency, uses information on the economic activities of companies in its assessment and pays special attention to the fulfillment of their obligations towards clients.

They compile a rating of companies in the insurance market and enter information into a database. As for the client base, their assessment is based on:

- prompt payment processing;

- quality of service, attitude towards the client;

- number of reviews on the Internet;

- reviews from acquaintances, friends, colleagues;

- number of clientele.

At the same time, the main criterion for assessing the rating is reliability, expressed by financial indicators.

The rating of the most popular insurance companies is given in the table:

| Company name | Number of applications | Number of failures | % failure | Degree of reliability |

| Allianz-ROSNO | 8 483 | 2 877 | 34% | A++ |

| National Insurance Group | 1 385 | 175 | 13% | A+ (III) |

| Russian insurance transport company | 3 134 | 336 | 11% | A++ |

| Liberty Insurance | 1 231 | 80 | 6% | A+ (II) |

| Rosgosstrakh | 220 813 | 13 097 | 6% | A++ |

| SOGAZ | 5 555 | 310 | 6% | A++ |

| Agreement | 29 619 | 1 623 | 5% | A++ |

| Surgutneftegaz | 1 720 | 90 | 5% | A+ (III) |

| Energy guarantor | 8 852 | 403 | 5% | A++ |

| MSK | 69 968 | 2 963 | 4% | A+ (III) |

| Renaissance Insurance | 11 248 | 387 | 3% | A++ |

| UralSib | 22 629 | 730 | 3% | A++ |

| RESO Guarantee | 53 327 | 1 580 | 3% | A++ |

| Ingosstrakh | 50 628 | 1 309 | 3% | A++ |

| VSK-Insurance | 47 177 | 1 213 | 3% | A+ |

| MAX Insurance | 27 006 | 549 | 2% | A++ |

| VTB Insurance | 1 398 | 16 | 1% | A+ (III) |

And in conclusion, it should be noted that the emergence of the MTPL insurance form in the insurance market makes it possible to avoid traffic conflicts, protect and protect drivers from disputes due to road accidents.

Not every insurance company meets legal requirements, so you need to take a closer look at their activities before choosing the right one.

How to calculate the loss of marketable value of a car, see the article: Loss of marketable value of a car under compulsory motor liability insurance. Find out how to calculate the cost of MTPL here.

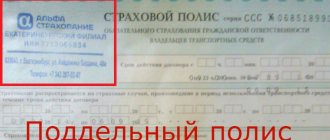

OSAGO in the Alfastrakhovanie company is discussed in this article.