CASCO - an abbreviation or not

With the advent of this type of insurance, auto experts and ordinary citizens had many questions related to the decoding of the term CASCO. In this case, deciphering the abbreviation is not required, since CASCO, in fact, is not such.

The word casco (Italian: “casco”), translated from Italian, means nothing more than “board”. Initially, Italian companies used this type of insurance exclusively for sea vessels. Marine board insurance implied compensation for damage caused to the structural elements of water transport.

There are several other possible versions of the origin of this term:

- Dutch casco is a body,

- Spanish casco means skull,

- English cascade is translated as practicing an imitation of a fall.

The exact decoding of this term is known, but the exact country of origin of this word causes a lot of controversy. At the moment, it is generally accepted that the term CASCO still comes from the Italian language, and other versions are erroneous.

Often you can even hear variants of the meaning of the abbreviation CASCO from Russian auto insurance companies and car owners.

The decryption (the most popular, but incorrect options) is named as follows:

- Comprehensive Automobile Insurance Excluding Liability (CASIO).

- Comprehensive Automobile Insurance Except Liability (CASCO).

To increase the client base and interest of drivers, agents of insurance organizations are trying to decipher the term more and more sophisticatedly.

If this is not an abbreviation, then why is it customary in Russia to write this term in capital letters?

The fact is that, by analogy with the compulsory type of OSAGO insurance, the name of this policy began to be prescribed exactly this way. This is most likely done due to the peculiarities of human perception. The correct spelling is CASCO.

What is the difference between CASCO and OSAGO?

Motorists often compare these two types of insurance. Where do they find differences?

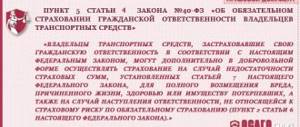

OSAGO is a mandatory type of car insurance. The driver has no right to operate a vehicle without a motor vehicle insurance policy. This document is necessary for compensation for damage to health and vehicle as a result of a car accident. In other words, if a car owner is at fault for a car accident, his insurance company is obliged to compensate for the damage.

The main advantage of OSAGO is its availability and relative cheapness compared to a CASCO policy. Tariffs for compulsory motor liability insurance are set by the government of the Russian Federation. One of the disadvantages of this type of auto insurance is limited payments. If the damage is significant, then insurance will only cover part of the losses.

CASCO insurance is voluntary. By taking out such a policy, the car owner can count on protection of his vehicle, but not on payments to third parties in the event of a traffic accident.

Unlike a compulsory motor liability insurance policy, it protects the vehicle and does not insure the driver’s liability. Not every driver can afford such a car policy. The policy does not have clearly established rates. Its cost, by and large, depends on the nature of the possible risks.

CASCO insurance in Russia

The insurance policy offers its owner the following benefits:

- The ability to take out insurance against “damage” risks - the company will fully cover the costs in the event of a road accident or natural disaster, regardless of whose fault it all happened. Moreover, the costs to the owner will be covered both under the heading of compensation for the actual damage and compensation for the costs of restoring the car to the second participant in the accident.

- A policy is provided against the risk of vehicle theft.

- The policy covers not only the body of the car, but also additional components.

- The amount of the insurance amount is fixed, specified in advance in the agreement and cannot change during the validity of the insurance.

- A person has the right to choose compensation options - repairs or money.

- Repayment of minor damage is possible without the involvement of police officers and the issuance of relevant certificates, which makes this service especially popular among drivers.

- Additional preferences on the roads - for example, calling a tow truck, technical assistance, settling insurance situations at a service center.

Let us immediately note that the price of the service in comparison with other available policies is quite high. It consists of the following aspects:

- Age of the car owner - for people who do not fall within the range of 20-65 years, the cost will be higher, since it is during these years that people most often get into accidents.

- The year of manufacture of the car - however, those vehicles that are more than 10 years old cannot be insured at all.

- General driving experience - the higher it is, the cheaper CASCO is, accordingly.

- Make and cost of the vehicle – official theft statistics for a specific model are taken into account.

In addition to the listed factors, the total amount of insurance depends on the form of payment, the presence or absence of anti-theft devices, as well as the specific company that completed the transaction - each of them may have its own prices for certain services.

Table “Fees and payments for comprehensive insurance for 2021” (according to the Central Bank of the Russian Federation) [2]

| Subtype of property insurance | Bonuses, thousand rubles | Payments, thousand rubles | Payout level |

| Autocasco | 170 672 096 | 97 472 694 | 57,11% |

| Railway transport insurance | 1 430 042 | 552 031 | 38,60% |

| Air transport insurance | 8 700 507 | 3 169 634 | 36,43% |

| Water transport insurance | 5 433 425 | 4 075 903 | 75,02% |

Table “Fees and payments for comprehensive insurance for 2013” (according to the Federal Financial Markets Service)

| Subtype of property insurance | Bonuses, thousand rubles | Payments, thousand rubles | Payout level |

| Autocasco[2] | 212 300 490 | 155 797 448 | 73,39% |

| Railway transport insurance[3] | 1 428 162 | 531 415 | 37,21% |

| Air transport insurance[4] | 6 592 529 | 3 710 018 | 56,28% |

| Water transport insurance[5] | 3 779 512 | 2 587 858 | 68,47% |

Casco is a voluntary type of comprehensive insurance for cars or other means of transport (ships, planes, wagons, etc.). A comprehensive insurance contract protects the car owner from unexpected costs of repairing the vehicle after being involved in a road traffic accident (RTA), as well as damage from theft (theft), careless and unlawful actions of third parties (PDTL), and any objects falling on the car ( including snow and ice), fire (arson, spontaneous combustion), explosion.

The insurance policy also protects you from situations where the insured event occurs due to the fault of the policyholder himself or due to unforeseen situations or natural disasters (lightning, storm, hurricane, rain, hail, heavy snowfall, earthquake, landslide, flood , landslide).

Unlike a compulsory motor liability insurance policy, a comprehensive insurance agreement allows the car owner to cover the costs of repairing his own car, regardless of who was at fault for the accident.

The insurance company with which the car owner has entered into a comprehensive insurance contract, upon the occurrence of an event stipulated in the contract (insured event), compensates the car owner for losses caused within the limits of the amount specified in the contract (insurance amount).

Insurers often use the terms “full” and “partial” comprehensive insurance. “Full comprehensive insurance” includes car insurance against theft and damage, and “partial comprehensive insurance” only insurance against damage.

As a rule, a comprehensive insurance agreement is concluded for a year.

The cost of comprehensive insurance for the same car can vary significantly among different insurance companies. Along with this, each company offers its own insurance programs, which also differ significantly both in terms of the provision of services and in the list of specific insurance risks included in the comprehensive insurance agreement and which are insured events.

- car model;

- year of car manufacture;

- power and condition of the car;

- age, driving experience of the policyholder and persons entitled to drive a car;

- car storage and safety conditions (garage, parking lot, alarm system);

- nature of vehicle operation;

- the amount of the insured amount;

- additional insurance conditions;

- and many other factors.

Different insurance companies take into account a certain set of factors when calculating a comprehensive insurance policy.

To reduce the cost of insurance by 10-20%, you can apply for a deductible. This means that when an insured event occurs, you yourself pay a certain amount of money specified in the comprehensive insurance contract, and the remaining amount is paid by the insurance company.

Today, most companies providing comprehensive insurance have online calculators on their official websites to calculate the cost of the contract. Having specified all the necessary parameters related to your car, the calculator will automatically calculate the cost of the comprehensive insurance contract. But such calculators cannot guarantee 100% accuracy of the calculation, so it is much more correct to visit the office of the insurance company and ask the manager for an accurate calculation for your car in accordance with the chosen tariff.

Additional insurance is needed in the following insured events:

- car theft;

- damage (due to hooliganism, fire, natural disaster, other force majeure circumstances);

- vandalism or deliberate theft;

- complete destruction of transport.

Each insurance company

In any case, these do not include:

- intentional damage or theft;

- damage caused by a driver under the influence of alcohol or drugs;

- when driving a car without a license.

Payments will not be made if the incident occurred outside the policy area (for example, during a trip abroad).

When purchasing a policy, the following features are taken into account:

- term of the contract (from 6 months to 5 years);

- the age of the car (many companies refuse to issue insurance for cars older than 10 years);

READ MORE: Windshield under CASCO: what to do and how to replace

For partial CASCO insurance, the minimum insurance period is 1 month. There are restrictions on the age of the car depending on the place of production. For Russian cars, the maximum age is 5 years. For foreign cars this figure is 7 years. The cost of the policy is higher than for compulsory motor liability insurance. Because of this, novice drivers often purchase insurance for 6 months. The peculiarity is that the cost of such a policy is approximately 70% of the annual one.

Types of CASCO

As we found out, this type of insurance is exclusively voluntary. There are several policy options.

Any car owner can insure his vehicle with an auto policy, using several of its variations:

- Damage. This option is the most popular. The document covers damage resulting from a transport accident, natural disaster, or fire. In addition, such insurance involves compensation for damage received from people or animals.

- Hijacking. Not the most popular way of insurance. The problem is that almost all insurance companies, as a prerequisite, require the installation of a special satellite search system, blockers or other protective devices on vehicles. Not every organization is ready to issue such a policy option, since there is a risk that the owner of the vehicle will rush to get rid of such personal transport.

- Comprehensive insurance. Combines the two car policy variations presented above. This type of Auto and CASCO is recommended to be issued if the car owner bought the vehicle on credit or he is the owner of an exclusive car.

The ability to choose the type of insurance that is convenient for you is a great success. Definitely, of the presented options, the third one is the most reliable. However, the cost of such a car policy is high. What makes it so expensive and inaccessible? Let's consider what the cost of CASCO depends on.

What you need to know before applying for a CASCO policy

Every car owner should know as much information as possible about CASCO policies: what it is, what benefits it provides, how you can save money. Before concluding a contract, you should immediately ask the insurance company employees what to do in a given situation, how to notify the insurer about an insured event, what certificates are needed, etc.

Also, you will probably be interested to know which insurance is better to choose in case of an accident - CASCO or OSAGO?

There are a huge number of insurance companies that provide car insurance in our market. The leaders are Rosgosstrakh, Ingosstrakh, AlfaStrakhovanie, Reso, Soglasie. These insurance companies have been operating in the market for a long time, have large clients and a good reputation. Their prices are higher than those of small regional companies, but they offer excellent quality services.

Also, when choosing a CASCO program, you can seek the help of an insurance agent or a qualified broker, who will make calculations for several insurance companies at once. However, you should remember that you will have to pay for CASCO insurance out of your own pocket, so you need to decide where to insure the car yourself.

What determines the cost of the policy?

Insuring a car or other vehicle under CASCO is not a cheap pleasure. The price of insurance depends on many factors.

Moreover, the insurance organization has the right to refuse to issue a car policy if there are grounds for this:

- more than three years have passed since the vehicle was manufactured;

- The vehicle is parked in an unguarded parking lot.

Each company sets its own prices for the policy.

The price will depend on the following vehicle characteristics:

- type and model;

- year of issue;

- period and nature of insurance;

- wear;

- availability of a franchise.

Everything is more or less clear with the first five points. It is better to examine the concept of a franchise in more detail.

Calculate the cost of CASCO online

Calculating the cost of comprehensive insurance yourself is very difficult for two reasons - firstly, all companies use different formulas to calculate the cost, and secondly, the calculation formulas are usually quite complex and take into account many parameters, and even the smallest error can distort the calculation results. Fortunately, there are a large number of online calculators on the Internet that can be used to approximately calculate the cost of a comprehensive insurance policy. This usually takes into account:

- Age and place of registration of the driver.

- Data about the vehicle - car make, engine power, presence of an anti-theft system, and so on.

- Information about the insurance you want to buy (the number of people allowed to drive, a list of insured events, the presence of a deductible, and so on).

What is a franchise and who benefits from a car policy with a franchise?

Most motorists are very familiar with the types, conditions and prices of car insurance. However, in any type of insurance there are nuances that allow you to reduce the cost of the insurance policy. One of the options for reducing the price of car insurance is to have a deductible clause in the contract.

In simple terms, a franchise is an additional condition in an insurance contract, expressed in the obligation of the insured person to cover part of the losses caused to the vehicle at his own expense.

The amount of the franchise can be expressed in a specific fixed amount specified in the contract, or as a percentage of the insured value of the vehicle.

The type and amount of the deductible are discussed in advance by the insurance company and the car owner, and then reflected in the insurance contract.

The franchise has several types:

- Conditional. If the damage caused does not exceed the established deductible, the insurer will not compensate for such loss.

- Unconditional. Implies a portion of the loss deducted from the final amount of compensation.

- Dynamic. It is a type of unconditional franchise. It is applied from the second or third insured event.

In property insurance, an unconditional deductible is most often used. The main advantage of this type of auto policy is guaranteed financial protection as a result of serious car accidents, as well as lower insurance costs.

What may be the grounds for refusal of insurance payment?

Any car insurance contract contains a clause with possible reasons for refusing to compensate the client for damages or exemption from payments. There are a great many such reasons and there is no point in listing them.

Here are the most popular insurance claim denials:

- violation of traffic rules by the driver, including alcohol or drug intoxication;

- absence from the policy of the person driving the vehicle at the time of the accident;

- storing a vehicle in unguarded parking lots;

- absence or malfunction of the anti-theft system;

- repairing vehicles before they are inspected by a representative of the insurance company;

- violation of the period for filing an insurance claim.

To ensure that the car owner is not denied payments, it is necessary to carefully read the contract and study each clause. Not all insurance companies operate using legal methods. If a car enthusiast has such doubts, it is better to seek help from an experienced car lawyer.