OSAGO

The decoding of the abbreviation OSAGO sounds like Compulsory Auto Civil Liability Insurance. A car is a source of increased danger to others, so its owner insures his property against the possibility of damage. OSAGO is insurance that covers damage caused to someone while driving a car. Compulsory car insurance has existed in our country for more than 15 years and has been continuously improved all this time. Lawmakers, automobile experts, and ordinary drivers criticize the system, accusing insurers of trying to profit from ordinary citizens. On the contrary, companies talk about the unprofitability of this type of activity. In this article we will not discuss who is right. Let's look at the difference between CASCO and MTPL and tell you about the main features of each type of insurance.

What is the difference?

What is the difference between CASCO and OSAGO? The fundamental difference between CASCO and OSAGO is in the form of insurance .

A compulsory motor liability insurance policy is required for all drivers, and its absence is considered a violation of the law.

The difference with CASCO is that it is voluntary. You can get it for additional protection, but in the absence of this policy the car owner is not in danger.

CASCO and OSAGO, what is the difference?

Under the MTPL policy, damages to victims of road accidents are paid. If an accident occurs due to the fault of the policyholder, the company sends for repair the car that was damaged by the owner of the MTPL policy. In this case, he himself does not receive compensation and restores his vehicle at his own expense. Under the CASCO policy, the car owner is compensated for the repair of his damaged vehicle. This is precisely the difference between compulsory and voluntary types of insurance. It is wrong to discuss which is better OSAGO or CASCO? These are different types of insurance that do not replace, but complement each other.

What is the difference between OSAGO AND CASCO?

To understand the differences between these types of insurance, it is necessary to find out what MTPL is and what CASCO is.

- OSAGO is an agreement for compulsory motor third party liability insurance.

- CASCO is a voluntary vehicle insurance contract.

The main difference between them is the subject of insurance. When considering liability insurance, property liability is insured in the event of negative consequences in the form of a traffic accident. It is the material damage caused to third parties as a result of an accident that is the subject of insurance.

By taking out a voluntary insurance policy, the car is insured in case of damage or other material damage to it by anyone.

Moreover, in the event of an insured event under the auto insurance policy, payments will be made by the party at fault in the accident. When an insured event occurs under a motor vehicle insurance contract, it does not matter who is at fault, since the risk of the insured event itself is insured.

When taking out a policy

The difference between insurance contracts is expressed in the design of the policy:

OSAGO can be issued in one of three types, namely:

- for a specific car and an indefinite number of persons;

- for a specific driver and an unspecified vehicle;

- for a certain car and certain people allowed to drive it.

CASCO insurance is issued exclusively for a specific car.

Object of insurance

The differences between these types of contracts lie in the object of insurance. For a car insurance policy, such an object is motor liability, or rather the fact of its occurrence. When it occurs, the company providing insurance services assumes the responsibility to compensate for the damage caused to other persons.

Other persons include:

- other drivers moving on the roads;

- pedestrians and cyclists.

In the case of CASCO insurance, the object of insurance is a motor vehicle. At the same time, the point is that vehicles involved in an accident are restored using funds received as insurance payments. Receipt of which is possible only in the event of the occurrence of conditions that are an insured event and provided for in the contract.

Cost of OSAGO and CASCO

The cost of the policies is completely different. After all, companies providing insurance services set prices independently. At the same time, the company providing insurance services applies its own price calculation formulas.

It is also worth noting that depending on the region of the country, prices may differ significantly due to different coefficients applied to different regions.

It is also important that the calculation of the cost of a CASCO insurance policy is taken from the estimated value of the car. Typically, the cost is 5-8% of the estimated value of the car.

Factors influencing the cost of CASCO include:

- car age;

- estimated value of the car;

- number of selected additional options;

- the period for which the contract was concluded;

- its technical condition;

- frequency of theft of this type of vehicle in the region;

- and other factors taken into account by insurance companies.

The cost of compulsory motor insurance is influenced by the following factors:

- contract time;

- the number of persons to whom it applies;

- having a minimum of 3 years of experience;

- and others.

For CASCO and OSAGO payments

There are significant differences in payments under these types of contracts.

These include:

- payments under compulsory motor liability insurance are aimed at compensating for the damage caused and are not paid to the person who entered into the contract. The beneficiary of the policy will be the person who suffered the damage;

- in the case of CASCO, the person who entered into an insurance agreement and the person who will receive payments coincide. That is, the beneficiary will be the one who is insured. The only case when such persons do not coincide is the case when the CASCO agreement was concluded by a representative of the party and he acted on the basis of a power of attorney on behalf and in the interests of the person to whom the power of attorney was issued.

Payment terms

Agreements may have completely different payment terms. When signing them, you must carefully read the provisions of the contract regarding the timing of the transfer of payments in the event of an event that is insured.

The payment period under a liability insurance contract, upon the occurrence of an insured event, is fixed by law and is 30 days. In case of delay in insurance payment, payment of a penalty is guaranteed. It amounts to 1.3% of the refinancing fee for each day of delay.

Under a motor vehicle insurance contract, the payment period may be much shorter. For bona fide insurance companies, it does not exceed 10 days. If the damage is not significant - 2 days.

Limits of liability

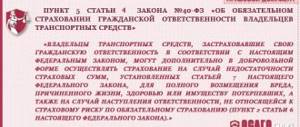

The MTPL law now provides liability limits: 500 thousand rubles. for compensation for damage caused to the life and health of the victim in an accident, and 400 thousand rubles. for compensation for damage to property. If several people or cars were injured in an accident, then these amounts apply to everyone.

In approximately 90% of cases, this money is enough to compensate for the damage. But if a serious accident occurs and expensive cars are involved, then the amount of damage may exceed the limits provided by law. In this case, the insurance company covers the costs within the agreed limits, and the person responsible for the accident pays the amount exceeding the limits.

It is possible to protect yourself from serious expenses in the event of major damage. To do this, you need to apply for an extension to your MTPL policy. The car owner receives an additional insurance policy. If an insured event occurs and the calculation of damage exceeds the limit under compulsory motor liability insurance, then part of the money will be paid within the framework of compulsory motor liability insurance, and the excess amount will be paid under an additional compulsory motor liability insurance extension policy.

Not all companies enter into OSAGO extension. Before completing a transaction, it is necessary to check the policyholder. This is a necessary measure, since many scammers have settled in the MTPL market.

Explanation of the abbreviation CASCO

money-trans.ruGAP insurance for comprehensive insurance

CASCO is voluntary insurance of vehicles (cars, air, sea, river, railway transport) against possible damage caused, theft or theft.

The main difference between CASCO is that the insurance company will repair your car in any case, even if you are the culprit of the accident or damaged the car not in an accident, and will also pay you the cost of the car if it is stolen or completely destroyed (if you have full CASCO). Such insurance has a high cost, but it relieves the owner from any worries and problems with the car.

The abbreviation CASCO, quite popular among motorists, stands for:

- K – Complex

- A – Automotive

- C – Insurance

- K – Except

- About – Responsibility

What does the cost of compulsory motor insurance depend on?

The price of the policy is influenced by many factors: region of registration, vehicle power, age and driving experience of people allowed to drive, accident-free driving rate. The risk group includes young people under the age of 22, beginners with less than three years of driving experience.

The accident-free driving rate decreases with each break-even year and increases sharply if the payment was due to the fault of the policyholder. If several people are included in the policy, then when calculating the final amount, they are equal to the worst. Therefore, it does not always make sense to include someone in the policy “just in case.”

The policy can be with a certain number of people allowed to manage it and without limiting them. In the second option, the price of the policy is as high as possible, since the highest coefficients of accident-free driving, length of service and age are taken. There is an important nuance: if a person regularly purchases an MTPL policy without restrictions on those allowed to drive and his data does not appear in the MTPL policy, then his accident-free driving ratio not only does not increase, but also returns to the base indicator after a few years. Thus, it turns out that a policy without restrictions on those admitted to management can be beneficial in one situation, but unjustifiably expensive in another.

From 2021, the so-called “tariff corridor” began to operate: insurers have the right to increase their tariffs by 20% up and down from the size of the basic prices. The age-experience coefficient is calculated more individually.

An insurance agent from FAVORIT MOTORS Group of Companies will help you choose the best option for purchasing a MTPL insurance policy. Our specialists undergo special training and are well versed in all the nuances of the insurance market.

So what should you choose?

So, let's take a closer look at all these subtleties and find out why and under what circumstances repairs or payment of Casco are more profitable and better than under compulsory motor liability insurance.

Increase in insurance prices for next year

This is the most important factor in the choice. The fact is that both types of insurance become more expensive the next year if there are insured events:

- if you applied for Casco in the current year, then next year an increased coefficient will be applied to you,

- the same thing with compulsory motor liability insurance, but, unlike Casco, here only an accident in which you are at fault is recognized as an insured event that increases the cost of insurance.

Thus, perhaps the main criterion for choosing – OSAGO or Casco, is the rise in price of the policy for the next year. But not all insurance companies increase the cost of voluntary insurance.

Conclusion : in many cases, applying under compulsory motor liability insurance rather than under Casco is better for the victim in terms of increasing the cost of insurance for the next year.

What if next year I take insurance from another company?

This is also the best option. But, again, not all companies will suit you. The fact is that many Casco insurers, as of 2021, offer discounts for breaking even in the first organization and, conversely, also increase the cost of the policy if insured events have been reported.

But your current insurer may not increase the price if, for example, you were not to blame for the accident (many companies have this condition), but other organizations simply will not look at this fact.

Conclusion : applying for Casco does not always lead to an increase in the cost of insurance, but manipulations with “running around” between companies can lead to this.

Depreciation calculation

This is rare in Casco contracts. But according to OSAGO, the calculation of compensation is always calculated taking into account wear and tear, which depends on the age of the car and can reach up to 50% for cars older than 5 years.

And, if in the case of sending for repairs, according to the law, you should not care about wear and tear (after all, it is forbidden to install used spare parts), then when you pay, you will receive less. And let’s be honest, very often, even when sent for repairs under compulsory motor liability insurance, you have to face the requirement of additional payment from a car service for new spare parts.

But the difference between what the insurance company calculated without wear and tear and what it paid taking it into account can be recovered directly from the person at fault for the accident. This is what the Constitutional Court of the Russian Federation ruled.

Conclusion : if your car is older than 2-4 years, and you don’t want unnecessary hassles to collect wear and tear or disputes with the insurer and service station, then Casco is better than OSAGO.

Documents for insurance and waiting for payment

OSAGO has a whole set of them:

- your passport, insurance policy, car ownership documents,

- statement,

- accident notification,

- a ruling on the guilt of the second participant or a ruling.

Please note that you can wait up to a year for the latest documents from the traffic police if the accident occurred with injuries or deaths.

In turn, the set of documents for applying under Casco is regulated not by law, but by agreement. But, as a rule, the set of documents is smaller. In addition, you can often apply for Casco without any documents at all, but the amount of compensation or the number of damaged items repaired in this case may be limited.

Conclusion : it is better to apply under Casco than under MTPL if you want to wait less time and collect fewer documents (but not always).

I don't want to contact the insurance company at fault

But under compulsory motor liability insurance you can also contact your insurance... Subject to 2 conditions:

- Only cars were damaged from road accidents.

- both have valid MTPL policies.

The conclusion is obvious.

I want a payment, not a repair

For several years now, compensation under compulsory motor liability insurance has been made in kind - that is, first of all, you are required to issue a referral for repairs. Not the choice of the insurance company, as many believe, but repair as a priority if all the conditions for this are met. But what are these conditions and how to get paid?

Under compulsory motor liability insurance, payment in lieu of repairs can be received in cases where:

- you indicated this desire in your application for compensation in case of an accident, and the insurer agreed (but most often they refuse),

- the nearest service station with which the insurer has an agreement is further than 50 km from the accident site or your address of residence, and transportation is not profitable for the insurance company,

- there are no suitable service stations with which the company has an agreement (including dealers, if your car is less than 2 years old),

- when applying under OSAGO they recognized the total loss of the car, while under Casco they offer repairs,

- if the victim died during an accident (and you receive compensation for him as a relative),

- damage according to insurance calculations exceeds 400,000 rubles,

- you have received moderate or severe injuries, or are disabled, and have chosen payment in your application.

All these points, according to the 2021 OSAGO law, require the insurer to make only payments.

Conclusion : if you want to receive a payment and fall under one of the conditions described above, then it is better to apply under MTPL than under Casco... All this if your Casco agreement only provides for repairs.

I only want to go to an official dealer

Here, too, in the case of Casco, everything depends only on the contract - the list of service centers for repairs should appear in it.

Repair under OSAGO is only possible at a dealer if your car is not older than 2 years.

Conclusion : it is better to apply for MTPL if your car is less than 2 years old.

With mutual guilt

Since Casco insures your property, and OSAGO insures liability in the event of guilt, if all participants in an accident are recognized as culprits, Casco is more profitable. Why?

The point here is that if it is, for example, 50/50 fault, you will receive only 50% of the calculated amount of compensation under the auto insurance policy, because you are partly at fault. And for the Casco agreement, the degree of your guilt in terms of compensation does not matter at all. But please note, again, that the policy in this case may become more expensive for the next year of insurance.

Conclusion : if the fault is mutual, then you need to understand that Casco is better than compulsory motor liability insurance after such an accident.

Franchise

Look carefully at your agreement - often many car enthusiasts do not even suspect that they have entered into it with a franchise.

In our case, it means that the insurance company does not cover a certain fixed amount of damages.

Let's take another example. You were recognized as a victim in an accident, and the amount of damage to you was calculated at 50,000 rubles. At the same time, the deductible under your Casco insurance contract is 30,000 rubles. In this case, the company will reimburse you only 20,000 rubles for this insurance event under Casco. But according to compulsory motor liability insurance there must be a full amount - there are no franchises in compulsory motor liability insurance.

Conclusion : if your Casco agreement implies a franchise, then OSAGO is more profitable.

What is needed to apply for compulsory motor liability insurance?

It is enough to present documents for the car and indicate the details of the driver’s license of people allowed to drive. The MTPL rules stipulate that the insurer has the right to inspect the vehicle. In practice this is rarely done. This point exists to combat fraudsters who, without repairing the car, simulate fake accidents. Also, sometimes an inspection is required in order to find a reason and refuse to issue a policy. Often insurers do not like to issue compulsory motor vehicle liability insurance for motorcycles and ask to see it.

What is OSAGO?

OSAGO is popularly briefly called “motor citizen”, since this abbreviation stands for compulsory auto insurance of civil liability. In this case, it covers damage to other vehicles, road users and passengers. The person responsible for the accident does not receive compensation for damage. The driver has to repair the vehicle at his own expense. This is very inconvenient and unprofitable for most motorists.

Motor insurance is mandatory, so the driver simply does not have the right to refuse to take it out. A significant fine is imposed for the absence of compulsory motor insurance. The client cannot be refused to issue a compulsory insurance policy, regardless of driving experience and negative driving experience. If such a nuisance happens, the insurance company will face a large fine. This policy is valid only for motor vehicles.

Technical inspection

Cars that are three years old do not require a technical inspection when taking out a compulsory motor liability insurance policy. Older cars need to come to an inspection point, where specialists will assess the condition of the car. The diagnostic card for cars aged 3 years is valid for two years; older cars must be inspected annually.

At all FAVORIT MOTORS Group dealerships you can undergo a technical inspection. Moreover, our clients can receive the document required to purchase an MTPL policy after scheduled maintenance.

Refusal to pay damages

The Rules and the MTPL insurance contract list cases when the company refuses compensation for damage. The insurance company will not pay if the car was damaged during competitions, tests or training driving, cargo defects appeared during loading or unloading, money, antiques, works of art, and jewelry were damaged during the insured event.

There are also cases when the company compensates for the damage to the victim, but then has the right to demand that the culprit of the accident return the money spent:

- the harm was caused intentionally;

- the person responsible for the accident was intoxicated;

- the culprit of the accident did not have the right to drive a vehicle;

- the driver fled the scene of the accident;

- the driver is not included in the list of permitted persons (when using a compulsory motor liability insurance policy with a limited number of persons permitted to drive);

- the insured event occurred when using the vehicle during a period not provided for by the MTPL agreement;

- when filling out the documents independently, the insurer was not sent a copy of the accident form;

- the car was not provided for inspection;

- The diagnostic card has expired for taxis, buses, trucks intended for transporting people carrying dangerous goods;

- when concluding a contract, a person provided false information, which led to an unreasonable reduction in the amount of the insurance premium - for example, they try to save money by indicating their place of residence in a region where compulsory motor liability insurance is cheaper.

What are the differences between CASCO and OSAGO?

As mentioned above, CASCO is not the only vehicle insurance option. A more common question when choosing an insurance policy is: “Which should I choose CASCO or OSAGO?”

| CASCO | OSAGO |

| Voluntary type of insurance. | Mandatory insurance when purchasing a car. |

| More flexible insurance, it can be tailored to your needs. | All conditions are already determined by the insurance contract. |

| The insurance payment will be equal to the estimated amount at the time of conclusion of the contract. | Coverage of damage up to 400 thousand rubles. |

| CASCO insurance insures theft and damage to the car, with the exception of self-inflicted damage. | Driver civil liability insurance for road accidents. The policy is only for the car |

| You can independently determine the validity period of the insurance contract. | The insurance period is one year. |

| An insured event is all events that can happen to a car. | An insured event is an accident in which the driver of the car was involved. |

Consequently, you cannot choose between CASCO and MTPL, since you are obliged to insure your car under the MTPL policy. But for greater security, you have the right to buy CASCO insurance and not worry that if your car is damaged or stolen, you will incur huge costs.

Compensation form for compulsory motor liability insurance

Many scammers have appeared on the MTPL market. Various frauds: false accidents, incorrect assessment of damage, provoking penalties. Therefore, in 2018, “direct settlement of losses” was introduced under OSAGO: the victim’s car is sent for repairs to a technical center with which an agreement was concluded. Direct insurance does not apply to motorcycles and in cases where insurers are unable to send the vehicle for repairs. For example, a damaged car is located in such a remote area that there is not a single service station nearby. Or the car is rare and there are no spare parts for it. In this case, the damage is compensated in money, and the assessment takes into account wear and tear. For example, for an 8-year-old car, the body part will be valued at about half the cost of a new one.

When restoring a car under compulsory motor liability insurance, the damage is calculated in accordance with special reference books updated every 6 months. There are no restrictions on the manufacturer of spare parts, so we install both original parts and products from third-party manufacturers.

The difference between CASCO and OSAGO?

- OSAGO (“motor citizen”) is compulsory insurance, and CASCO is voluntary. For the absence of an MTPL policy, the law provides for a fine of 8 minimum wages. In addition, if as a result of an accident the person at fault does not have a mandatory insurance policy, the Motor Transport Insurance Bureau seeks compensation from the driver in court to cover the damage caused to the injured party.

- Tariffs for compulsory MTPL motor insurance are approved by the Resolution of the Russian Federation. For CASCO, tariffs are not regulated by law, but depend on the general situation in the insurance market and the existing national pricing policy.

- The amount of insurance payments under compulsory motor liability insurance is also clearly fixed. Under CASCO insurance compensation depends on the amount of the insurance contract, but cannot exceed the full cost of the insured vehicle.

- Significant differences between CASCO and OSAGO lie in the process of paying insurance compensation itself. Payment under compulsory insurance is made only after a court decision. Some insurance companies provide compensation based on a detailed traffic police certificate, which contains comprehensive information about the accident. But this is only in the case when there are no victims and the culprit is clearly identified. As for CASCO insurance, insurance payment is made according to the decision of the insurance company. The only exception is when fraud is proven in court.

Summarizing the above, we can conclude that the main difference between the two policies lies in the pursuit of different interests: OSAGO performs an important social role, taking care of order and compensation for damage to injured innocent persons. CASCO stands guard over the personal interests of car owners, protecting and protecting their property rights.

E-OSAGO

Now you can insure a car under MTPL directly at the insurer’s office, use the services of a broker, or purchase a policy remotely. The algorithm is simple: you need to go directly to the website of the company you are interested in or the Russian Union of Auto Insurers, enter data (vehicle approved for driving, technical inspection, etc.), pay the bill and receive a policy.

It is enough to have a printout of the policy with you. If necessary, the traffic police inspector can check the car using the database.

Penalty for lack of insurance

Responsibility for the absence of a policy is stipulated by Art. 12.37 Code of Administrative Offences. If the driver is a person who is not included in the policy, they will be fined 500 rubles. If there is no policy at all, then the amount increases to 800 rubles.

The issue of a significant increase in the fine is being discussed. In addition, it is planned to introduce automatic policy availability control. Photo-video recording cameras will send data to be checked against the database for the presence of a compulsory motor liability insurance policy, and if there is no such policy, the owner will receive a “letter of happiness.”

Differences between CASCO and OSAGO

There are a number of differences between these two types of insurance, which can be summarized as follows:

- Insurance form. If “car insurance” is mandatory, then CASCO insurance can be issued on a voluntary basis. Fines are provided only for the absence of the first policy, while the registration of the second requires the voluntariness of the motorist.

- Price. If the payment for compulsory motor liability insurance is fixed by the state, then other types of insurance completely depend on the regulations of the insurer.

- Determination of the amount of damage. “Avtograzhdanka” is more demanding in determining the amount of damage to third parties. To make calculations, it is necessary to conduct an independent examination of the condition of the car and the injured persons. Under CASCO insurance, the amount of compensation is determined by any representative of the company.

- Compensation for damage. Each situation has a precisely fixed amount of payments in the case of compulsory motor liability insurance, but with other types of insurance there are no clear boundaries of payments. The only limit on payment is the total value of the insured car. The amount of payments cannot exceed this figure.

IMPORTANT !!! Payments for motor insurance can be made taking into account depreciation or without taking this indicator into account. This item depends on the terms of the contract. When applying for compulsory motor liability insurance, the law only provides for compensation for damage, taking into account depreciation. The payment terms also differ significantly, since with compulsory motor liability insurance it is 30 days, and with CASCO it depends on the specific terms of the contract.

- Insurer bankruptcy. RSA is responsible to each client who has issued compulsory motor liability insurance, but there is no guarantee of payments for drivers who have issued CASCO insurance. In this case, all responsibility for choosing an insurer falls entirely on the car owner, but he can defend his rights in court.

- Possibility of registration. If the insurer cannot refuse to issue a client a “car insurance”, then CASCO insurance is not so easy to obtain.

- Payout limit. In the “autocitizen” system, compensation of up to 400,000 rubles is paid in case of damage to the property of third parties, and in case of damage to people – up to 500,000 rubles. CASCO pays only compensation for damage caused to a personal car, and the amount of payments depends entirely on the terms of the contract.

CASCO can also act as compulsory insurance if the car was purchased on credit. In this case, the insurer must cooperate with the bank issuing the loans.

There are 2 types of policies:

- having an aggregate amount, each time decreasing by the amount of compensation already paid,

- having a non-aggregate amount, the payment of compensation for which does not depend on the money paid previously.

Of course, the second option will cost the driver much more, but it will be much more convenient for those motorists who are frequent participants in road accidents.

CASCO

Contrary to popular belief, CASCO is not an acronym. From a grammatical point of view, it is correct to write the word in ordinary letters, since the term comes from the Spanish casco, that is, “helmet,” or the Dutch casco, which means “body.” The capital letters appeared due to a misunderstanding; they began to write them this way to resemble the abbreviation OSAGO. Therefore, various attempts at decoding (for example, Comprehensive Auto Insurance) are, by definition, incorrect. But let's get back to the main thing.

CASCO is a bet between the insurance company and the car owner. If the car is damaged, the company will pay for the damage. If the entire period passes without incident, then the money paid becomes the company’s net profit.

What is the difference between OSAGO and CASCO? The main difference between CASCO and OSAGO is that with CASCO the car itself is insured, and with OSAGO the driver’s civil liability is insured.

CASCO insurance is voluntary, but in some cases it may become mandatory. For example, when buying a car at a car dealership with bank money, the bank requires a CASCO policy. In this way, the credit institution ensures the return of its money. There is no need to go to the bank specifically to draw up the document.

What is CASCO?

How to decipher the term and how is it translated? CASCO is an additional insurance that is not mandatory. There is an opinion that it stands for comprehensive automobile insurance except liability. But this is a myth, since in fact there is no abbreviation for this term motor insurance.

The name is translated from Italian as the word “board”. From this it is clear that it is the car that is subject to insurance, and not the people who are in it. Insurance allows the owner to protect himself from a wide range of problems . Payments in this case are expected, even if the culprit is the policy owner himself.

Registration of CASCO insurance is not mandatory. The only exception is when buying a car on credit, when the lender requires insurance.

We invite you to watch a video about what CASCO is:

Policy cost

The price of a CASCO policy is influenced by the cost of the car, its attractiveness to car thieves, and the profile of people allowed to drive: age, length of service, data on participation in accidents. Each insurance company has its own statistics, based on which employees calculate the cost of the policy. Therefore, the price of a policy for the same model varies from company to company. The insured amount should not exceed the cost of the car.

Most often, the insurance line is one year, but by agreement of the parties it can change. Insurers do not like short terms, so insurance for a year and 6 months can cost almost the same.

Differences in the decoding and rules of CASCO and OSAGO

So, the interpretation of CASCO and OSAGO has significant differences. As well as types of insurance. In the first case, the object is your own car, in the second case, the vehicle that was injured due to the fault of the client. Under CASCO, all damage is compensated; under OSAGO, there is a limit established by law. OSAGO implies compensation for harm caused to the health and life of victims, but CASCO does not. And finally, every car owner must apply for MTPL, and CASCO - on a voluntary basis.

Explanation of CASCO and OSAGO

OSAGO does not take into account the costs associated with the restoration and repair of their car, so many drivers choose CASCO to have a guarantee of a refund in case of damage or loss of the car. In addition, due to the limits on compulsory motor liability insurance, this amount is often not enough to compensate in full and the client is forced to pay the balance himself.

If you take out a DSAGO (voluntary motor third party liability insurance) policy, which does not provide for a limit on the sum insured, you can receive full compensation from the insurer if someone else’s car is damaged.

Company bankruptcy

If the policyholder goes bankrupt, the policy expires. In this case, it is possible to demand compensation through the court. Perhaps the bankrupt still has some assets left.

Bankruptcy should not be confused with license revocation. In the first case, the company has no funds; in the second, it simply does not have the right to engage in insurance. Although deprivation of a license is a bad sign. Very often this is followed by bankruptcy. Therefore, if information appears about the deprivation of a license, demand a refund of part of the policy and enter into an agreement with another company.

What is the difference between CASCO and OSAGO?

Motorists often compare these two types of insurance. Where do they find differences?

OSAGO is a mandatory type of car insurance. The driver has no right to operate a vehicle without a motor vehicle insurance policy. This document is necessary for compensation for damage to health and vehicle as a result of a car accident. In other words, if a car owner is at fault for a car accident, his insurance company is obliged to compensate for the damage.

The main advantage of OSAGO is its availability and relative cheapness compared to a CASCO policy. Tariffs for compulsory motor liability insurance are set by the government of the Russian Federation. One of the disadvantages of this type of auto insurance is limited payments. If the damage is significant, then insurance will only cover part of the losses.

CASCO insurance is voluntary. By taking out such a policy, the car owner can count on protection of his vehicle, but not on payments to third parties in the event of a traffic accident.

Unlike a compulsory motor liability insurance policy, it protects the vehicle and does not insure the driver’s liability. Not every driver can afford such a car policy. The policy does not have clearly established rates. Its cost, by and large, depends on the nature of the possible risks.

Franchise

This is the obligation of the insured person to bear part of the losses at his own expense. In this way, companies try to avoid paying for minor damage and subsequent minor repairs. The higher the deductible, the cheaper the cost of the policy.

A franchise can be catchy or unconditional. With a conditional franchise, the company is not liable if the loss does not exceed a certain amount. The insurer only pays for major damage.

With an unconditional deductible, a specified amount is always deducted from the damage. For example, the damage amounted to 300 thousand rubles. If the contract states that the franchise is 10 thousand, then they will pay 290 thousand, and 10 thousand will have to be paid at their own expense.

What is a franchise and who benefits from a car policy with a franchise?

Most motorists are very familiar with the types, conditions and prices of car insurance. However, in any type of insurance there are nuances that allow you to reduce the cost of the insurance policy. One of the options for reducing the price of car insurance is to have a deductible clause in the contract.

In simple terms, a franchise is an additional condition in an insurance contract, expressed in the obligation of the insured person to cover part of the losses caused to the vehicle at his own expense.

The amount of the franchise can be expressed in a specific fixed amount specified in the contract, or as a percentage of the insured value of the vehicle.

The type and amount of the deductible are discussed in advance by the insurance company and the car owner, and then reflected in the insurance contract.

The franchise has several types:

- Conditional. If the damage caused does not exceed the established deductible, the insurer will not compensate for such loss.

- Unconditional. Implies a portion of the loss deducted from the final amount of compensation.

- Dynamic. It is a type of unconditional franchise. It is applied from the second or third insured event.

In property insurance, an unconditional deductible is most often used. The main advantage of this type of auto policy is guaranteed financial protection as a result of serious car accidents, as well as lower insurance costs.

Refusal of compensation under CASCO

In the voluntary insurance system, the rules may differ, so you need to read them carefully.

Most companies will refuse if the driver was drunk or someone who is not on the list of those allowed to drive. There is a certain period within which an incident must be reported. Risk requirements for theft may be specified. For example, you need to return all the keys to your car. Previously, there were requirements for the mandatory presence of a car at night in a guarded parking lot, but now such clauses have already become an anachronism. Car insurance Catalog of new cars Catalog of used carsAsk a question