Good afternoon, dear reader.

From September 5, 2021, a new Directive of the Bank of Russia “On insurance tariffs for compulsory civil liability insurance of vehicle owners” has been in force, which has made major changes to the rules for calculating the cost of compulsory motor third party liability insurance.

There are quite a few innovations, and the first part of them is discussed in the article “New tariffs for calculating the cost of compulsory motor liability insurance from September 5, 2021.” Today, in the second part, new coefficients for calculating the cost of insurance and new formulas used in the calculation will be discussed.

- New coefficients of age and length of service (ACS).

- Cancellation of the FAC for foreign vehicles.

- Increase in FAC for legal entities.

- Calculation of FAC for drivers who do not have a Russian license.

- Cancellation of the coefficient for driving a vehicle with a gearbox trailer.

- Cancellation of the CN violation coefficient.

- Selecting the KBM coefficient when there are several drivers.

- New formulas for calculating the cost of insurance.

Basic rates for compulsory motor liability insurance from January 9, 2021

Everything is quite simple here.

The insurer sets the basic rates within the minimum and maximum limits itself. The principle by which this is done remains unknown. More likely. The make and age of the car, region, as well as the insurance history of the car owner are taken into account. In practice, for such a short time (since January 9 of this year), for example, for passenger cars of category B owned by individuals, the maximum value of 4,942 rubles is used. This conclusion was made experimentally, namely when trying to buy an electronic MTPL policy from a number of popular insurance companies. Now it’s worth considering the basic tariffs.

The insurer must notify the Bank of Russia in writing about the established base rate within three working days from the date of its confirmation. He should also add this information to the official website.

Table of base rates 2021 by vehicle category

| № | Type (category) and purpose of the vehicle | Basic insurance rate (rubles) | |

| Minimum TB value | Maximum TB value | ||

| 1. | Motorcycles, mopeds and light quadricycles (vehicles of categories “A”, “M”) | 694 | 1 407 |

| 2. | Vehicles of categories “B”, “BE” | ||

| 2.1 | legal entities | 2 058 | 2 911 |

| 2.2 | individuals, individual entrepreneurs | 2 746 | 4 942 |

| 2.3 | used as a taxi | 4 110 | 7 399 |

| 3. | Vehicles of categories “C” and “CE” | ||

| 3.1 | with a permissible maximum weight of up to 16 tons. | 2 807 | 5 053 |

| 3.2 | with a permissible maximum weight of more than 16 tons. | 4 227 | 7 609 |

| 4. | Vehicles of categories “D” and “DE” | ||

| 4.1 | with a number of passenger seats up to 16 | 2 246 | 4 044 |

| 4.2 | with more than 16 passenger seats | 2 807 | 5 053 |

| 4.3 | used for regular transportation with pick-up and disembarkation of passengers both at established stopping points along the regular transportation route, and in any place not prohibited by traffic rules along the regular transportation route | 4 110 | 7 399 |

| 5. | Trolleybuses (vehicles of category “Tb”) | 2 246 | 4 044 |

| 6. | Trams (vehicles of category "Tm") | 1 401 | 2 521 |

| 7. | Tractors, self-propelled road-building and other machines, with the exception of vehicles that do not have wheeled propulsion systems | 899 | 1 895 |

To determine the category of a vehicle, the data noted in the document on its registration is used. This could be a vehicle passport, registration certificate, technical passport, technical certificate. The information provided by the policyholder when concluding the contract is also taken into account.

How to calculate the price of OSAGO

The system for determining car insurance rates is determined by Russian legislation. All calculations use the basic compulsory motor insurance price calculation. In addition, other factors also influence the final amount:

- Category and type of vehicle. The amount that must be paid for compulsory motor liability insurance is different for a car and a truck. Each type has different coefficients.

- Who owns the car - an institution, organization, company or individual.

- The belonging of the mobile object for which compulsory motor liability insurance is issued to a particular territory. In a large, densely populated city, the likelihood of an accident prevails, in contrast to a small town or village. The price is influenced by the territorial location of the vehicle.

- Driving experience of a MTPL holder. Driving experience is very important. It is clear that for people who know how to drive a car well, the likelihood of getting into an accident is much lower than for novice car enthusiasts.

Other indicators are also taken into account: technical characteristics of the vehicle, time of car insurance, and in the event of an accident, who was to blame for the incident.

Auto Insurance Pricing Equation

The formula below indicates which coefficients are directly applied when calculating compulsory motor liability insurance.

Spolisa OSAGO = TB x Kt x KBM x Kvs x Ko x Km x Ks x Kp x Kn, where

- TB – basic indicator;

- and below is a breakdown of other coefficients:

- Kt – regional, determined by the place of registration of the car or registration of the organization;

- KBM - bonus-malus - is determined for each applicant personally, depending on how many accidents the driver was involved in;

- Kvs is a value that regulates the age and driving experience of the MTPL purchaser;

- Ko – policy limits depend on the number of persons allowed to drive the vehicle;

- Km – a value depending on the amount of energy generated by the car’s motor;

- Кс – restrictions associated with the season of using equipment;

- Kp is an indicator of the period during which compulsory motor liability insurance has legal force;

- Kn – used for persistent traffic violators;

The formula shows that the cost is based on the tariff rate, which is multiplied by various coefficient values. Next, we will study them in detail and in detail.

Basic rates TB tariff corridor

The basic tariff is a value that depends on the type and category of car, and the legal status of the owner. Until 2015, this rate remained unchanged. And from April 12, 2015, amendments were made to the legislation. Now the base rate is a money corridor. This allows insurers to vary the price of the MTPL policy and interest car owners with a lower cost.

Thanks to innovations, car enthusiasts have the opportunity to choose the best offer on the market. When choosing the minimum tariff corridor, you should be careful not to fall for the bait of scammers - fly-by-night companies.

Below are the TB (thousand rubles) of different vehicles.

| View | Category | TB |

| motor transport | A | 0,87-1,579 |

| passenger cars, privately owned | IN | 3,432-4,118 |

| passenger cars owned by the organization | IN | 2,573-3,087 |

| passenger taxis | IN | 5,138-6,166 |

| trucks (up to 16 tons) | WITH | 3,509-4,211 |

| trucks (over 16 tons) | WITH | 5,284-6,341 |

| buses with from 1 to 15 seats for transporting passengers | D | 2,808-3,370 |

| buses with 16 seats or more for transporting passengers | D | 3,509-4,211 |

| taxi buses | D | 5,138-6,166 |

OSAGO coefficients from January 9, 2021

Dear readers!

Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem, please contact the online consultant form

It's fast and free!

Or call us by phone (24/7):

If you want to find out how to solve your particular problem, call us by phone. It's fast and free!

What else to read:

- My car was scratched in the yard, what should I do?

- Europrotocol 2021

- How to get money instead of repairs under compulsory motor liability insurance: a detailed review

+7 (495) 980-97-90(ext.589) Moscow,

Moscow region

+8 (812) 449-45-96(ext.928) St. Petersburg,

Leningrad region

+8 (800) 700-99-56 (ext. 590) Regions

(free call for all regions of Russia)

The amount of the insurance premium that is payable in accordance with the contract (policy price) is calculated by multiplying different coefficients. For example, if you take cars from categories B and BE, the insurance price will include the following components:

- Basic tariff (TB).

- Territorial coefficient (CT). Determined based on the region in which the machine is primarily used.

- Bonus-malus ratio (BMR). This coefficient takes into account the presence or absence of insurance payments made by insurance companies previously.

- Age-experience coefficient (AEC). A coefficient determined taking into account the driver’s age and experience.

- Limiting factor (CL). Determined taking into account the availability of data on the number of drivers who can drive the car.

- Engine power factor (PM). It is calculated taking into account the engine power of the machine.

- Seasonality coefficient (SC). Takes into account the seasonality of vehicle operation.

- Violation rate (CN).

What is KBM

KBM is the bonus-malus coefficient, which is used when calculating the insurance premium. According to the tariff manual for compulsory motor liability insurance, there are 14 accident classes. At the same time, a motorist with class 13 is entitled to a maximum discount when calculating the insurance premium.

The operating principle of bonus-malus is very simple:

- for each year without emergency control a 5% discount is given, which is added up annually;

- If there are losses due to the driver’s fault, compulsory motor liability insurance provides for an increasing coefficient, which directly depends on the number of declared losses.

This is the only indicator that a traffic participant can change himself. Careful motorists, thanks to accident-free driving, can save on purchasing a policy.

It should also be taken into account that since 2003, the state has made amendments to the tariffs and changed all indicators, except for the table with bonuses. This is the only coefficient that has remained unchanged since the appearance of the mandatory product on the territory of the Russian Federation.

Territorial coefficient

This coefficient or the territory of primary use of the car is determined taking into account the place of residence of the car owner indicated in the car’s passport, vehicle registration certificate, and in the driver’s passport. For legal entities, it is determined by the direct location of the legal entity, its branch or representative office, noted in the constituent documentation.

If the car owner permanently lives abroad and temporarily operates the car in the Russian Federation, a CT size of 1,7.

Table

You can use filtering in the table. In the search field of the 2nd column (Territory of preferential use of transport proximity), enter your region to quickly find out the coefficient.

| № | Territory of primary use of vehicles | CT coefficient for vehicles, with the exception of tractors, self-propelled road construction and other machines | CT coefficient for tractors, self-propelled road-building and other machines, with the exception of vehicles that do not have wheel propulsors |

| 1 | Republic of Adygea | 1,3 | 1 |

| 2 | Altai Republic | ||

| 2.1 | Gorno-Altaisk | 1,3 | 0,8 |

| 2.2 | Other cities and towns | 0,7 | 0,5 |

| 3 | Republic of Bashkortostan | ||

| 3.1 | Blagoveshchensk, Oktyabrsky | 1,2 | 0,8 |

| 3.2 | Ishimbay, Kumertau, Salavat | 1,1 | 0,8 |

| 3.3 | Sterlitamak, Tuymazy | 1,3 | 0,8 |

| 3.4 | Ufa | 1,8 | 1 |

| 3.5 | Other cities and towns | 1 | 0,8 |

| 4 | The Republic of Buryatia | ||

| 4.1 | Ulan-Ude | 1,3 | 0,8 |

| 4.2 | Other cities and towns | 0,6 | 0,5 |

| 5 | The Republic of Dagestan | ||

| 5.1 | Buynaksk, Derbent, Kaspiysk, Makhachkala, Khasavyurt | 0,7 | 0,5 |

| 5.2 | Other cities and towns | 0,6 | 0,5 |

| 6 | The Republic of Ingushetia | ||

| 6.1 | Malgobek | 0,8 | 0,5 |

| 6.2 | Nazran | 0,6 | 0,5 |

| 6.3 | Other cities and towns | 0,6 | 0,5 |

| 7 | Kabardino-Balkarian Republic | ||

| 7.1 | Nalchik, Prokhladny | 1 | 0,8 |

| 7.2 | Other cities and towns | 0,7 | 0,5 |

| 8 | Republic of Kalmykia | ||

| 8.1 | Elista | 1,3 | 0,8 |

| 8.2 | Other cities and towns | 0,6 | 0,5 |

| 9 | Karachay-Cherkess Republic | 1 | 0,8 |

| 10 | Republic of Karelia | ||

| 10.1 | Petrozavodsk | 1,3 | 0,8 |

| 10.2 | Other cities and towns | 0,8 | 0,5 |

| 11 | Komi Republic | ||

| 11.1 | Syktyvkar | 1,6 | 1 |

| 11.2 | Ukhta | 1,3 | 0,8 |

| 11.3 | Other cities and towns | 1 | 0,8 |

| 12 | Republic of Crimea | ||

| 12.1 | Simferopol | 0,6 | 0,6 |

| 12.2 | Other cities and towns | 0,6 | 0,6 |

| 13 | Mari El Republic | ||

| 13.1 | Volzhsk | 1 | 0,8 |

| 13.2 | Yoshkar-Ola | 1,4 | 0,8 |

| 13.3 | Other cities and towns | 0,7 | 0,5 |

| 14 | The Republic of Mordovia | ||

| 14.1 | Ruzaevka | 1,2 | 1 |

| 14.2 | Saransk | 1,5 | 1 |

| 14.3 | Other cities and towns | 0,8 | 0,6 |

| 15 | The Republic of Sakha (Yakutia) | ||

| 15.1 | Neryungri | 0,8 | 0,5 |

| 15.2 | Yakutsk | 1,2 | 0,7 |

| 15.3 | Other cities and towns | 0,6 | 0,5 |

| 16 | Republic of North Ossetia-Alania | ||

| 16.1 | Vladikavkaz | 1 | 0,8 |

| 16.2 | Other cities and towns | 0,8 | 0,5 |

| 17 | Republic of Tatarstan | ||

| 17.1 | Almetyevsk, Zelenodolsk, Nizhnekamsk | 1,3 | 0,8 |

| 17.2 | Bugulma, Leninogorsk, Chistopol | 1 | 0,8 |

| 17.3 | Elabuga | 1,2 | 0,8 |

| 17.4 | Kazan | 2 | 1,2 |

| 17.5 | Naberezhnye Chelny | 1,7 | 1 |

| 17.6 | Other cities and towns | 1,1 | 0,8 |

| 18 | Tyva Republic | ||

| 18.1 | Kyzyl | 0,6 | 0,5 |

| 18.2 | Other cities and towns | 0,6 | 0,5 |

| 19 | Udmurt republic | ||

| 19.1 | Votkinsk | 1,1 | 0,8 |

| 19.2 | Glazov, Sarapul | 1 | 0,8 |

| 19.3 | Izhevsk | 1,6 | 1 |

| 19.4 | Other cities and towns | 0,8 | 0,5 |

| 20 | The Republic of Khakassia | ||

| 20.1 | Abakan, Sayanogorsk, Chernogorsk | 1 | 0,8 |

| 20.2 | Other cities and towns | 0,6 | 0,5 |

| 21 | Chechen Republic | 0,6 | 0,5 |

| 22 | Chuvash Republic | ||

| 22.1 | Kanash | 1,1 | 0,8 |

| 22.2 | Novocheboksarsk | 1,2 | 0,8 |

| 22.3 | Cheboksary | 1,7 | 1 |

| 22.4 | Other cities and towns | 0,8 | 0,5 |

| 23 | Altai region | ||

| 23.1 | Barnaul | 1,7 | 1 |

| 23.2 | Biysk | 1,2 | 0,8 |

| 23.3 | Zarinsk, Novoaltaisk, Rubtsovsk | 1,1 | 0,8 |

| 23.4 | Other cities and towns | 0,7 | 0,5 |

| 24 | Transbaikal region | ||

| 24.1 | Krasnokamensk | 0,6 | 0,5 |

| 24.2 | Chita | 0,7 | 0,5 |

| 24.3 | Other cities and towns | 0,6 | 0,5 |

| 25 | Kamchatka Krai | ||

| 25.1 | Petropavlovsk-Kamchatsky | 1,3 | 1 |

| 25.2 | Other cities and towns | 1 | 0,6 |

| 26 | Krasnodar region | ||

| 26.1 | Anapa, Gelendzhik | 1,3 | 0,8 |

| 26.2 | Armavir, Sochi, Tuapse | 1,2 | 0,8 |

| 26.3 | Belorechensk, Yeisk, Kropotkin, Krymsk, Kurganinsk, Labinsk, Slavyansk-on-Kuban, Timashevsk, Tikhoretsk | 1,1 | 0,8 |

| 26.4 | Krasnodar, Novorossiysk | 1,8 | 1 |

| 26.5 | Other cities and towns | 1 | 0,8 |

| 27 | Krasnoyarsk region | ||

| 27.1 | Achinsk, Zelenogorsk | 1,1 | 0,8 |

| 27.2 | Zheleznogorsk, Norilsk | 1,3 | 0,8 |

| 27.3 | Kansk, Lesosibirsk, Minusinsk, Nazarovo | 1 | 0,8 |

| 27.4 | Krasnoyarsk | 1,8 | 1 |

| 27.5 | Other cities and towns | 0,9 | 0,5 |

| 28 | Perm region | ||

| 28.1 | Berezniki, Krasnokamsk | 1,3 | 0,8 |

| 28.2 | Lysva, Tchaikovsky | 1 | 0,8 |

| 28.3 | Permian | 2 | 1,2 |

| 28.4 | Solikamsk | 1,2 | 0,8 |

| 28.5 | Other cities and towns | 1,1 | 0,8 |

| 29 | Primorsky Krai | ||

| 29.1 | Arsenyev, Artem, Nakhodka, Spassk-Dalniy, Ussuriysk | 1 | 0,8 |

| 29.2 | Vladivostok | 1,4 | 1 |

| 29.3 | Other cities and towns | 0,7 | 0,5 |

| 30 | Stavropol region | ||

| 30.1 | Budennovsk, Georgievsk, Essentuki, Mineralnye Vody, Nevinnomyssk, Pyatigorsk | 1 | 0,8 |

| 30.2 | Kislovodsk, Mikhailovsk, Stavropol | 1,2 | 0,8 |

| 30.3 | Other cities and towns | 0,7 | 0,5 |

| 31 | Khabarovsk region | ||

| 31.1 | Amursk | 1 | 0,8 |

| 31.2 | Komsomolsk-on-Amur | 1,3 | 0,8 |

| 31.3 | Khabarovsk | 1,7 | 1 |

| 31.4 | Other cities and towns | 0,8 | 0,5 |

| 32 | Amur region | ||

| 32.1 | Belogorsk, Svobodny | 1,1 | 0,9 |

| 32.2 | Blagoveshchensk | 1,6 | 0,9 |

| 32.3 | Other cities and towns | 1 | 0,6 |

| 33 | Arhangelsk region | ||

| 33.1 | Arkhangelsk | 1,8 | 1 |

| 33.2 | Kotlas | 1,6 | 1 |

| 33.3 | Severodvinsk | 1,7 | 1 |

| 33.4 | Other cities and towns | 0,85 | 0,5 |

| 34 | Astrakhan region | ||

| 34.1 | Astrakhan | 1,4 | 1 |

| 34.2 | Other cities and towns | 0,8 | 0,5 |

| 35 | Belgorod region | ||

| 35.1 | Belgorod | 1,3 | 0,8 |

| 35.2 | Gubkin, Stary Oskol | 1 | 0,8 |

| 35.3 | Other cities and towns | 0,8 | 0,5 |

| 36 | Bryansk region | ||

| 36.1 | Bryansk | 1,5 | 1 |

| 36.2 | Klintsy | 1 | 0,8 |

| 36.3 | Other cities and towns | 0,7 | 0,5 |

| 37 | Vladimir region | ||

| 37.1 | Vladimir | 1,6 | 1 |

| 37.2 | Gus-Khrustalny | 1,1 | 0,8 |

| 37.3 | Moore | 1,2 | 0,8 |

| 37.4 | Other cities and towns | 1 | 0,8 |

| 38 | Volgograd region | ||

| 38.1 | Volgograd | 1,3 | 0,8 |

| 38.2 | Volzhsky | 1,1 | 0,8 |

| 38.3 | Kamyshin, Mikhailovka | 1 | 0,8 |

| 38.4 | Other cities and towns | 0,7 | 0,5 |

| 39 | Vologda Region | ||

| 39.1 | Vologda | 1,7 | 1 |

| 39.2 | Cherepovets | 1,8 | 1 |

| 39.3 | Other cities and towns | 0,9 | 0,5 |

| 40 | Voronezh region | ||

| 40.1 | Borisoglebsk, Liski, Rossosh | 1,1 | 0,9 |

| 40.2 | Voronezh | 1,5 | 1,1 |

| 40.3 | Other cities and towns | 0,8 | 0,6 |

| 41 | Ivanovo region | ||

| 41.1 | Ivanovo | 1,8 | 1 |

| 41.2 | Kineshma | 1,1 | 0,8 |

| 41.3 | Shuya | 1 | 0,8 |

| 41.4 | Other cities and towns | 0,9 | 0,5 |

| 42 | Irkutsk region | ||

| 42.1 | Angarsk | 1,2 | 0,8 |

| 42.2 | Bratsk, Tulun, Ust-Ilimsk, Ust-Kut, Cheremkhovo | 1 | 0,8 |

| 42.3 | Irkutsk | 1,7 | 1 |

| 42.4 | Usolye-Sibirskoye | 1,1 | 0,8 |

| 42.5 | Shelekhov | 1,3 | 0,8 |

| 42.6 | Other cities and towns | 0,8 | 0,5 |

| 43 | Kaliningrad region | ||

| 43.1 | Kaliningrad | 1,1 | 0,8 |

| 43.2 | Other cities and towns | 0,8 | 0,5 |

| 44 | Kaluga region | ||

| 44.1 | Kaluga | 1,2 | 0,8 |

| 44.2 | Obninsk | 1,3 | 0,8 |

| 44.3 | Other cities and towns | 0,9 | 0,5 |

| 45 | Kemerovo region | ||

| 45.1 | Anzhero-Sudzhensk, Kiselevsk, Yurga | 1,2 | 0,8 |

| 45.2 | Belovo, Berezovsky, Mezhdurechensk, Osinniki, Prokopyevsk | 1,3 | 0,8 |

| 45.3 | Kemerovo | 1,9 | 1 |

| 45.4 | Novokuznetsk | 1,8 | 1 |

| 45.5 | Other cities and towns | 1,1 | 0,8 |

| 46 | Kirov region | ||

| 46.1 | Kirov | 1,4 | 1 |

| 46.2 | Kirovo-Chepetsk | 1,2 | 0,8 |

| 46.3 | Other cities and towns | 0,8 | 0,5 |

| 47 | Kostroma region | ||

| 47.1 | Kostroma | 1,3 | 0,8 |

| 47.2 | Other cities and towns | 0,7 | 0,5 |

| 48 | Kurgan region | ||

| 48.1 | Mound | 1,4 | 0,8 |

| 48.2 | Shadrinsk | 1,1 | 0,8 |

| 48.3 | Other cities and towns | 0,6 | 0,5 |

| 49 | Kursk region | ||

| 49.1 | Zheleznogorsk | 1 | 0,8 |

| 49.2 | Kursk | 1,2 | 0,8 |

| 49.3 | Other cities and towns | 0,7 | 0,5 |

| 50 | Leningrad region | 1,3 | 0,8 |

| 51 | Lipetsk region | ||

| 51.1 | Dace | 1 | 0,8 |

| 51.2 | Lipetsk | 1,5 | 1 |

| 51.3 | Other cities and towns | 0,8 | 0,5 |

| 52 | Magadan Region | ||

| 52.1 | Magadan | 0,7 | 0,5 |

| 52.2 | Other cities and towns | 0,6 | 0,5 |

| 53 | Moscow region | 1,7 | 1 |

| 54 | Murmansk region | ||

| 54.1 | Apatity, Monchegorsk | 1,3 | 1 |

| 54.2 | Murmansk | 2,1 | 1,2 |

| 54.3 | Severomorsk | 1,6 | 1 |

| 54.4 | Other cities and towns | 1,2 | 1 |

| 55 | Nizhny Novgorod Region | ||

| 55.1 | Arzamas, Vyksa, Sarov | 1,1 | 0,8 |

| 55.2 | Balakhna, Bor, Dzerzhinsk | 1,3 | 0,8 |

| 55.3 | Kstovo | 1,2 | 0,8 |

| 55.4 | Nizhny Novgorod | 1,8 | 1 |

| 55.5 | Other cities and towns | 1 | 0,8 |

| 56 | Novgorod region | ||

| 56.1 | Borovichi | 1 | 0,8 |

| 56.2 | Velikiy Novgorod | 1,3 | 0,8 |

| 56.3 | Other cities and towns | 0,9 | 0,5 |

| 57 | Novosibirsk region | ||

| 57.1 | Berdsk | 1,3 | 0,8 |

| 57.2 | Iskitim | 1,2 | 0,8 |

| 57.3 | Kuibyshev | 1 | 0,8 |

| 57.4 | Novosibirsk | 1,7 | 1 |

| 57.5 | Other cities and towns | 0,9 | 0,5 |

| 58 | Omsk region | ||

| 58.1 | Omsk | 1,6 | 1 |

| 58.2 | Other cities and towns | 0,9 | 0,5 |

| 59 | Orenburg region | ||

| 59.1 | Buguruslan, Buzuluk, Novotroitsk | 1 | 0,8 |

| 59.2 | Orenburg | 1,7 | 1 |

| 59.3 | Orsk | 1,1 | 0,8 |

| 59.4 | Other cities and towns | 0,8 | 0,5 |

| 60 | Oryol Region | ||

| 60.1 | Livny, Mtsensk | 1 | 0,8 |

| 60.2 | Eagle | 1,2 | 0,8 |

| 60.3 | Other cities and towns | 0,7 | 0,5 |

| 61 | Penza region | ||

| 61.1 | Zarechny | 1,2 | 0,8 |

| 61.2 | Kuznetsk | 1 | 0,8 |

| 61.3 | Penza | 1,4 | 1 |

| 61.4 | Other cities and towns | 0,7 | 0,5 |

| 62 | Pskov region | ||

| 62.1 | Velikie Luki | 1 | 0,8 |

| 62.2 | Pskov | 1,2 | 0,8 |

| 62.3 | Other cities and towns | 0,7 | 0,5 |

| 63 | Rostov region | ||

| 63.1 | Azov | 1,2 | 0,8 |

| 63.2 | Bataysk | 1,3 | 0,8 |

| 63.3 | Volgodonsk, Gukovo, Kamensk-Shakhtinsky, Novocherkassk, Novoshakhtinsk, Salsk, Taganrog | 1 | 0,8 |

| 63.4 | Rostov-on-Don | 1,8 | 1 |

| 63.5 | Mines | 1,1 | 0,8 |

| 63.6 | Other cities and towns | 0,8 | 0,5 |

| 64 | Ryazan Oblast | ||

| 64.1 | Ryazan | 1,4 | 1 |

| 64.2 | Other cities and towns | 0,9 | 0,5 |

| 65 | Samara Region | ||

| 65.1 | Novokuybyshevsk, Syzran | 1,1 | 0,8 |

| 65.2 | Samara | 1,6 | 1 |

| 65.3 | Tolyatti | 1,5 | 1 |

| 65.4 | Chapaevsk | 1,2 | 0,8 |

| 65.5 | Other cities and towns | 0,9 | 0,5 |

| 66 | Saratov region | ||

| 66.1 | Balakovo, Balashov, Volsk | 1 | 0,8 |

| 66.2 | Saratov | 1,6 | 1 |

| 66.3 | Engels | 1,2 | 0,8 |

| 66.4 | Other cities and towns | 0,7 | 0,5 |

| 67 | Sakhalin region | ||

| 67.1 | Yuzhno-Sakhalinsk | 1,5 | 1 |

| 67.2 | Other cities and towns | 0,9 | 0,5 |

| 68 | Sverdlovsk region | ||

| 68.1 | Asbest, Revda | 1,1 | 0,8 |

| 68.2 | Berezovsky, Verkhnyaya Pyshma, Novouralsk, Pervouralsk | 1,3 | 0,8 |

| 68.3 | Verkhnyaya Salda, Polevskoy | 1,2 | 0,8 |

| 68.4 | Ekaterinburg | 1,8 | 1 |

| 68.5 | Other cities and towns | 1 | 0,8 |

| 69 | Smolensk region | ||

| 69.1 | Vyazma, Roslavl, Safonovo, Yartsevo | 1 | 0,8 |

| 69.2 | Smolensk | 1,2 | 0,8 |

| 69.3 | Other cities and towns | 0,7 | 0,5 |

| 70 | Tambov Region | ||

| 70.1 | Michurinsk | 1 | 0,8 |

| 70.2 | Tambov | 1,2 | 0,8 |

| 70.3 | Other cities and towns | 0,8 | 0,5 |

| 71 | Tver region | ||

| 71.1 | Vyshny Volochek, Kimry, Rzhev | 1 | 0,8 |

| 71.2 | Tver | 1,5 | 1 |

| 71.3 | Other cities and towns | 0,8 | 0,5 |

| 72 | Tomsk region | ||

| 72.1 | Seversk | 1,2 | 0,8 |

| 72.2 | Tomsk | 1,6 | 1 |

| 72.3 | Other cities and towns | 0,9 | 0,5 |

| 73 | Tula region | ||

| 73.1 | Aleksin, Efremov, Novomoskovsk | 1 | 0,8 |

| 73.2 | Tula | 1,5 | 1 |

| 73.3 | Uzlovaya, Shchekino | 1,2 | 0,8 |

| 73.4 | Other cities and towns | 0,9 | 0,5 |

| 74 | Tyumen region | ||

| 74.1 | Tobolsk | 1,3 | 0,8 |

| 74.2 | Tyumen | 2 | 1,2 |

| 74.3 | Other cities and towns | 1,1 | 0,8 |

| 75 | Ulyanovsk region | ||

| 75.1 | Dimitrovgrad | 1,2 | 0,9 |

| 75.2 | Ulyanovsk | 1,5 | 1,1 |

| 75.3 | Other cities and towns | 0,9 | 0,6 |

| 76 | Chelyabinsk region | ||

| 76.1 | Zlatoust, Miass | 1,4 | 0,8 |

| 76.2 | Kopeisk | 1,6 | 1 |

| 76.3 | Magnitogorsk | 1,8 | 1 |

| 76.4 | Satka, Chebarkul | 1,2 | 0,8 |

| 76.5 | Chelyabinsk | 2,1 | 1,3 |

| 76.6 | Other cities and towns | 1 | 0,8 |

| 77 | Yaroslavl region | ||

| 77.1 | Yaroslavl | 1,5 | 1 |

| 77.2 | Other cities and towns | 0,9 | 0,5 |

| 78 | Moscow | 2 | 1,2 |

| 79 | Saint Petersburg | 1,8 | 1 |

| 80 | Sevastopol | 0,6 | 0,6 |

| 81 | Jewish Autonomous Region | ||

| 81.1 | Birobidzhan | 0,6 | 0,5 |

| 81.2 | Other cities and towns | 0,6 | 0,5 |

| 82 | Nenets Autonomous Okrug | 0,8 | 0,5 |

| 83 | Khanty-Mansiysk Autonomous Okrug - Ugra | ||

| 83.1 | Kogalym | 1 | 0,8 |

| 83.2 | Nefteyugansk, Nyagan | 1,3 | 0,8 |

| 83.3 | Surgut | 2 | 1,2 |

| 83.4 | Nizhnevartovsk | 1,8 | 1 |

| 83.5 | Khanty-Mansiysk | 1,5 | 1 |

| 83.6 | Other cities and towns | 1,1 | 0,8 |

| 84 | Chukotka Autonomous Okrug | 0,6 | 0,5 |

| 85 | Yamalo-Nenets Autonomous Okrug | ||

| 85.1 | New Urengoy | 1 | 0,8 |

| 85.2 | Noyabrsk | 1,7 | 1 |

| 85.3 | Other cities and towns | 1,1 | 0,8 |

| 86 | Baikonur | 0,6 | 0,5 |

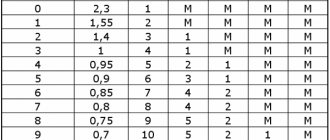

Bonus-malus coefficient

KBM is an insurance tariff coefficient, which is determined taking into account whether payments were made by insurers in the period from April 1 of the previous year to March 31 of the next year. Simply put, its size will depend on whether the policyholder was at fault for the accident or not.

For example, this year the BMR is 1. Next year it will be equal to 0.95, provided that the driver is not the culprit of the traffic accident. Accordingly, the policy will be cheap. If the driver causes one accident, in the next year this coefficient for him will be equal to 1.55, if two accidents, then 2.45, etc. This will make insurance more expensive.

Table

| Class when taking out annual insurance | Coefficient | Class at the end of the annual insurance, taking into account all insurance situations for the entire period of validity of the MTPL contracts | Year | Price | ||||

| 0 payouts | 1 payment | 2 payments | 3 payments | more than 3 payments | ||||

| M | 2,45 | 0 | M | M | M | M | ||

| 0 | 2,3 | 1 | M | M | M | M | ||

| 1 | 1,55 | 2 | M | M | M | M | ||

| 2 | 1,4 | 3 | 1 | M | M | M | ||

| 3 | 1 | 4 | 1 | M | M | M | ||

| 4 | 0.95 | 5 | 2 | 1 | M | M | ||

| 5 | 0.9 | 6 | 3 | 1 | M | M | ||

| 6 | 0.85 | 7 | 4 | 2 | M | M | ||

| 7 | 0.8 | 8 | 4 | 2 | M | M | ||

| 8 | 0.75 | 9 | 5 | 2 | M | M | ||

| 9 | 0.7 | 10 | 5 | 2 | 1 | M | ||

| 10 | 0.65 | 11 | 6 | 3 | 1 | M | ||

| 11 | 0.6 | 12 | 6 | 3 | 1 | M | ||

| 12 | 0.55 | 13 | 6 | 3 | 1 | M | ||

| 13 | 0.5 | 13 | 7 | 3 | 1 | M | ||

How to remove the multiplying factor

Careful driving is a guarantee that the indicator will not be increased. However, situations are different, and therefore many are interested in how to remove the increasing coefficient. There are several options in which it is possible to prevent an increase in the indicator and drivers should know this.

This way the multiplier will not increase:

- If the insured is recognized as the injured party in the incident, that is, the incident did not happen through his fault. In such a situation, there will be no reduction in driving class and no increase in performance.

- If, when applying for a new MTPL policy, the driver whose fault the traffic accident was committed is removed from the contract. The increase in the indicator will not be applied to the remaining parties to the agreement.

Related article: How to terminate an MTPL insurance policy and return funds

ATTENTION! Changing the insurance company will not help to avoid increasing the multiplier if there was an accident, since all insurance companies work with a single database of car owners. This means that the fact of an insured event cannot be hidden.

There is another way to prevent an increase - after an accident, negotiate with the other party and resolve the conflict situation without involving the traffic police. This, of course, depends on the severity of the damage caused. It is better to carry out repairs of a vehicle, which will require large expenses, at the expense of the insurance company.

You can find out more about how to reduce the KBM under compulsory motor liability insurance here.

Age-experience coefficient

This coefficient determines insurance rates taking into account how old the driver is and how long a driving experience he has. As already mentioned, from January 9 the number of steps increased from 4 to 58.

Table

| № | Experience, years\Age, years | 0 | 1 | 2 | 3-4 | 5-6 | 7-9 | 10-14 | 14+ |

| 1 | 16 — 21 | 1,87 | 1,87 | 1,87 | 1,66 | 1,66 | |||

| 2 | 22 — 24 | 1,77 | 1,77 | 1,77 | 1,04 | 1,04 | 1,04 | ||

| 3 | 25 — 29 | 1,77 | 1,69 | 1,63 | 1,04 | 1,04 | 1,04 | 1,01 | |

| 4 | 30 — 34 | 1,63 | 1,63 | 1,63 | 1,04 | 1,04 | 1,01 | 0,96 | 0,96 |

| 5 | 35 — 39 | 1,63 | 1,63 | 1,63 | 0,99 | 0,96 | 0,96 | 0,96 | 0,96 |

| 6 | 40 — 49 | 1,63 | 1,63 | 1,63 | 0,96 | 0,96 | 0,96 | 0,96 | 0,96 |

| 7 | 50 — 59 | 1,63 | 1,63 | 1,63 | 0,96 | 0,96 | 0,96 | 0,96 | 0,96 |

| 8 | over 59 | 1,6 | 1,6 | 1,6 | 0,93 | 0,93 | 0,93 | 0,93 | 0,93 |

If the car is registered in another country and is temporarily used in the Russian Federation, then the FAC is determined in the following dimensions:

- 1.7 – for a car owned by an individual;

- 1 – for a car that is the property of a legal entity.

Limiting factor

The CO is determined taking into account the number of persons allowed to drive in accordance with the policy. That is, whether the control of the car is entrusted to a limited or an unlimited number of drivers.

Table

| № | Information on the number of persons allowed to drive a vehicle owned by an individual | KO coefficient |

| 1 | The compulsory insurance contract provides for a limitation on the number of persons allowed to drive a vehicle | 1 |

| 2 | The compulsory insurance contract does not provide for a limitation on the number of persons allowed to drive a vehicle | 1,87 |

For legal entities this indicator is 1.8

General formula for calculating compulsory motor liability insurance

When calculating insurance, tariffs take into account the established base rates. There is a set form of calculation that includes this data. The basic data is influenced by the technical characteristics of the vehicle, design features, as well as the purpose of the vehicle and its possibility of participating in an accident and causing harm to other road users.

A detailed description and established sizes of these indicators are described in Appendix No. 1 to Directive of the Central Bank of the Russian Federation No. 3384.

Federal Law of the Russian Federation No. 40, clause 2, article 9 establishes the coefficients used in calculating insurance premiums. The size of these indicators is influenced by:

- The territory where the machine will be operated (place of registration). For example, in large cities the probability of an accident will be much higher than in rural areas, and accordingly the coefficient increases.

- Engine power.

- Service life of the vehicle.

- Ability to operate a trailer.

- The number of persons who can be allowed to drive a given vehicle and their driving experience.

- Duration of the policy.

All of the above is what makes up the cost of compulsory motor liability insurance.

IMPORTANT: the price of insurance is influenced by many factors. The maximum amount you will have to pay when insuring a powerful car that will be driven in a large populated metropolis by several drivers with minimal driving experience and who have previously been involved in an accident.

Engine power factor

To obtain data on the engine power of a car, STS or PTS is used. If these papers do not contain this data, information is taken from manufacturers’ catalogs and other official sources. If the PTS indicator is indicated in kilowatts, the ratio 1 kW/hour = 1.35962 hp is used to convert into horsepower.

Table

| № | Engine power (horsepower) | KM coefficient |

| 1 | Up to 50 inclusive | 0,6 |

| 2 | Over 50 to 70 inclusive | 1 |

| 3 | Over 70 to 100 inclusive | 1,1 |

| 4 | Over 100 to 120 inclusive | 1,2 |

| 5 | Over 120 to 150 inclusive | 1,4 |

| 6 | Over 150 | 1,6 |

Seasonality factor

This indicator depends on how many months out of 12 the driver will use the car.

Table

| № | Period of use of the vehicle | KS coefficient |

| 1 | 3 months | 0,5 |

| 2 | 4 months | 0,6 |

| 3 | 5 months | 0,65 |

| 4 | 6 months | 0,7 |

| 5 | 7 months | 0,8 |

| 6 | 8 months | 0,9 |

| 7 | 9 months | 0,95 |

| 8 | 10 months or more | 1 |

Examples of calculations

As an example, we can calculate the cost of compulsory motor liability insurance for a category B passenger car for an individual aged 22 years and with 2 years of driving experience. The transport was registered in Belgorod, insurance claims were not paid, the car was used by other people. The power of this transport was 80 horsepower, it was used for 6 months. There were no violations.

Calculations, let us remind you, occur according to the following formula: T = TB multiplied by CT multiplied by KBM multiplied by KVS multiplied by KO multiplied by KM multiplied by KS multiplied by KN.

Now you need to substitute the necessary values:

T = 3432 multiplied by 1.3 multiplied by 0.95 multiplied by 1.87 multiplied by 1 multiplied by 1.1 multiplied by 0.7.

As a result, the cost of compulsory motor liability insurance in this case will be equal to 6103.05 Russian rubles.

This may seem quite complicated and intimidating to an inexperienced person, but in reality it is quite simple. First, there are online calculators that streamline many of the verification and calculation processes. Secondly, there are even videos that clearly show how to independently calculate compulsory motor liability insurance, such as, for example, this video from Artyom Alymov:

You can watch it and participate in the discussion with everyone, and there are also links to useful online calculators right there.

Violation rate

This coefficient is used in the presence of action or inaction of the car owner, provided for in clause 3 of article 9 of the Federal Law “On Compulsory Motor Liability Insurance”.

This coefficient will be used and amount to 1.5 if the owner of the car:

- Provided the insurance company with deliberately untrue information about the requested circumstances affecting the amount of the insurance premium under the contract, due to which it was paid in a lesser amount than what should have been paid if the truthful information was provided.

- Knowingly contributed to the occurrence of an insured event or the associated losses to increase, or deliberately distorted the circumstances of its occurrence in order to increase the amount of compensation.

- Provoked harm under circumstances that are the basis for a claim of recourse.

What to do if you have increased your compulsory motor liability insurance ratio without an accident

There are situations when, for the purpose of profit and taking advantage of the driver’s inexperience, insurance companies increase the coefficient, even if there was not a single risky incident. You can avoid this if you compare the indicators when applying for a new policy. In order not to get into such a situation and not to purchase insurance at an inflated cost, you need to remember that when you switch to another insurance company, all data on the car owner is saved. Including the bonus-malus coefficient. Therefore, when switching, pay attention to what class is assigned to the new insurance company.

If the insurance company assigns category 3 to a new client, citing the fact that there is no information on the driver in the auto insurer’s unified database, the following actions must be taken:

- Independently send a request to the RSA database for information.

- In parallel, you can send a request with the same requirement to the union of insurers.

- Contact the previous IC with a request to issue a certificate with information about the driver.

It is important to remember that all these actions will only bring results if there really is no reason to improve performance.

Trailer availability factor

The CPR is determined depending on whether the contract contains information that makes it possible to operate the car together with its trailer.

Table

| № | Trailer depending on the type and purpose of the vehicle | KPR coefficient |

| 1 | Trailers for cars owned by legal entities, motorcycles and scooters | 1,16 |

| 2 | Trailers for trucks with a permissible maximum weight of 16 tons or less, semi-trailers, trailers | 1,4 |

| 3 | Trailers for trucks with a permissible maximum weight of more than 16 tons, semi-trailers, trailers | 1,25 |

| 3 | Trailers for tractors, self-propelled road construction and other machines, with the exception of vehicles that do not have wheeled propulsion devices | 1,24 |

| 4 | Trailers for other types (categories) and purpose of vehicles | 1 |

Insurance period or term coefficient

This coefficient (CP) depends on the duration of the insurance.

Table

| № | Insurance period for compulsory civil liability insurance of owners of vehicles registered in foreign countries and temporarily used on the territory of the Russian Federation | KP coefficient |

| 1 | From 5 to 15 days | 0,2 |

| 2 | From 16 days to 1 month | 0,3 |

| 3 | 2 months | 0,4 |

| 4 | 3 months | 0,5 |

| 5 | 4 months | 0,6 |

| 6 | 5 months | 0,65 |

| 7 | 6 months | 0,7 |

| 8 | 7 months | 0,8 |

| 9 | 8 months | 0,9 |

| 10 | 9 months | 0,95 |

| 11 | 10 months or more | 1 |

Video on the topic: OSAGO 2021

Catalog of insurance companies in Russia

By following the link , you can familiarize yourself with the catalog of insurance companies in the Russian Federation offering compulsory motor vehicle insurance services. Description of organizations, current financial indicators, ratings, reviews and other information. If you have already had a positive or negative experience with compulsory motor liability insurance of any insurance company, leave your feedback. Thank you!

Link again. Also, be sure to write your comment below. What do you think about the topic of this material? Or maybe you have questions? Ask!