Subjects and rates of car insurance

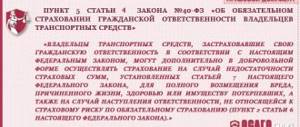

Thanks to the MTPL policy, the motorist has the opportunity to protect his property interests to the victim in the amount of no more than four hundred thousand rubles, in the event that the insured violates traffic rules, resulting in an accident.

The law of the Russian Federation establishes that all car owners must insure their civil liability to third parties. Insurance tariffs are regulated in accordance with the Federal Law, which establishes economically justified maximum tariff levels, as well as their structure and the procedure for implementation by insurance agents when determining the insurance premium.

When calculating tariffs, the share of the insurance premium to pay compensation to the victim must be equal to or exceed eighty percent of the premium amount. The established tariffs are valid for at least six months. Insurance statistics must be officially published annually. It is unacceptable to provide compensation to some categories by increasing the amount of insurance premiums to other categories of persons.

When tariffs increase, the insurance premium remains the same as at the time of signing the contract, according to the previous tariffs. The subjects of compulsory motor insurance are insurers providing insurance services on the basis of a license, intermediaries (various agencies), policyholders (purchasers of an insurance policy), and third parties (victims of road accidents). Compensations are issued through RSA, which is also a subject of OSAGO.

Advantages and disadvantages of the system

The civil liability system in relation to vehicle owners in the Republic of Kazakhstan has the following advantages:

- the mandatory nature of the said insurance, establishing the universal nature of providing protection and stimulating citizens to comply with safety measures while driving;

- the possibility of paying compensation to victims of road accidents and accidents during transport incidents;

- accessibility of pricing policy and the possibility of receiving discounts for low-income groups of the population;

- the dependence of the contract amount on the duration of the protection period and the discipline of the driver.

Article on the topic: OSAGO insurance for a truck and how to issue an insurance policy.

Disadvantages are associated with the presence of restrictions on the amount of deductions and the fact that, according to the provisions of the law, the culprit may not receive compensation as a result of recourse claims being presented to him by the insurer.

A mandatory civil liability insurance policy for car owners in KZ is the result of following international practice and a convenient way to protect road users. As a result of using this compulsory insurance method, victims can receive adequate compensation for damages incurred from an accident or road accident.

Responsibility for absence

Professional liability insurance is insurance of the policyholder's property interests associated with liability for harm caused to third parties as a result of errors or omissions committed in the performance of professional duties.

2 risk groups are insured:

- Risks associated with the possibility of causing bodily injury and harm to health to third parties. Risks associated with the activities of doctors, pharmacists and others.

- Risks associated with the possibility of causing material damage, including loss of the right to make claims. Risks associated with the activities of notaries, architects, auditors, civil engineers and others.

The risks of liability for harm caused intentionally, through deception, or crime are not compensated.

Insurance compensation for this type of insurance does not exceed a certain limit (deductible). The work of independent experts to determine the amount of loss is also deducted from the cost of damage.

The legislation also provides for certain penalties for the absence of a compulsory motor liability insurance policy. At the same time, the Code of Administrative Offenses of the Russian Federation provides for several articles at once.

If the driver has not purchased the document, he may be fined in the amount of 500-800 rubles. Also, the traffic police inspector has every right to detain and send the vehicle to a penalty area. The driver will be able to pick up his car only after presenting the insurance policy.

These are the main measures of liability for the absence of a compulsory motor liability insurance policy.

What is civil liability insurance?

Mandatory insurance of the civil consequences of liability of owners of transport equipment is understood as a set of measures aimed at compensating for losses caused to persons affected by road accidents by the insured vehicle owners.

The legislative framework

Issues of legislative regulation of this area of compulsory insurance of vehicle owners in the Republic of Kazakhstan are regulated by Law No. 446-M, which was adopted in 2003. The law is consistent with other regulatory documents affecting insurance issues related to the transport sector, and provides for the mandatory conclusion of a policy provided for by law by all owners of motor vehicles in the Republic.

Areas of insurance

Types of insurance in KZ, in relation to the field of transport relations, imply the possibility (and for some – mandatory) of concluding:

- civil liability agreements establishing the acquisition of insurance policies by transport owners, with this requirement established on a mandatory basis;

- CASCO contracts are contracts that are concluded voluntarily by vehicle owners and are aimed at compensating losses by the beneficiary in connection with damage or theft of the car.

This material describes the features of the mandatory scope of civil liability, prescribed by law, regarding the regulations in relation to vehicle owners on insuring their civil liability.

Article on the topic: How to reduce the KBM under compulsory motor liability insurance

Business insurance.

- Entrepreneurial risk and its types.

- Commercial risk insurance.

- Technical risk insurance.

- Insurance against losses due to business interruptions.

- Financial risk insurance.

I. Entrepreneurial risk and its types.

Business insurance means “the risk of losses from business activities due to violation of their obligations by the entrepreneur’s counterparties or changes in the conditions of this activity due to circumstances beyond the entrepreneur’s control, including the risk of not receiving expected income” (Article 929 of the Civil Code of the Russian Federation).

1. Disruption of the production process in the event of natural disasters, accidents and other similar events;

2. Changes in market conditions, failure to fulfill contracts on the part of suppliers or consumers of products (services), etc.

The most common types of this insurance are:

- Commercial risk insurance.

- Insurance against loss of profit due to interruptions in production.

- Insurance against the risks of introducing new technology.

- Financial risk insurance.

- Insurance of exchange and currency risks.

II. Commercial risk insurance.

The purpose of this insurance is to compensate the policyholder for possible losses if, after a certain period, the insured operations do not provide the payback stipulated by the contract. They are compensated for losses arising as a result of unfavorable unpredictable changes in market conditions, failure to fulfill contracts or other unforeseen circumstances.

Insurance does not cover losses caused by:

- intermediary activities;

- gambling and speculative transactions;

- decision of the currency authorities;

- changes in currencies;

- political upheavals;

- bank refusal to lend.

- intentional actions of the policyholder, partners or beneficiary to disrupt the insured activity or their violation of the law.

The insured amount for this insurance is established:

- When insuring investments - within the limits of the policyholder's capital investments in the insured operations.

- When insuring income - within the limits of all commercial investments and expected profits.

This insurance is carried out using a minimum deductible of 3-5% and establishing a maximum amount of compensation.

Insurance payment rates depend on the type of activity, insurance period, degree of stability of market relations, and interest rates on loans.

Reinsurance Basics

- The essence and main functions of reinsurance.

- Facultative and obligatory reinsurance.

- Proportional and non-proportional reinsurance.

Reinsurance is insurance by one insurer (reinsurer) under the conditions specified in the contract for the risk of fulfillment of all or part of its obligations to the insured by another insurer (reinsurer).

The risk transferred is called reinsurance risk. The process associated with the transfer of risk - risk assignment or reinsurance cession.

The reinsurer is called the cedant, and the reinsurer is called the assignee.

The risk accepted by the reinsurer from the reinsurer may be subject to subsequent transfer in whole or in part to another reinsurer. The subsequent transfer of the reinsured risk is called retrocession. An insurance company that transfers the risk to reinsurance to a third party is called a retrocedent, and one that accepts the risk is called a retrocessionary.

1. Ensuring the financial stability of the insurer.

It is achieved by fragmenting the risk and distributing it among a large number of insurance companies.

When transferring risk to reinsurance, it is important to determine the amount within which the insurance company retains its share of the insured risks - the company’s own retention.

If the deductible limit is underestimated, the insurance company will lose part of its income, because will transfer the excess portion of the insurance premium to reinsurance.

If the limit is too high, this may adversely affect the results of one’s own financial activities.

2. Protection of property interests of policyholders.

Ensures that the insurer fulfills its payment obligations to the policyholder.

H ≤ A – O, where

A – the size of the insurer’s assets;

O – the volume of the insurer’s obligations (amount of insurance reserves).

N – the minimum permissible amount of excess of the insurer's assets over its liabilities.

N = 5% of the insurance reserve.

N = 16% of the amount of insurance premiums received for the year.

Thus, the essence of reinsurance lies in “secondary” insurance of insurers against risks exceeding the solvency of the insurance company.

By transferring risks to reinsurance, the reinsurer receives the right to a bonus, i.e. commission on the profit that the reinsurer can receive when implementing the contract.

In practice there are:

- Active reinsurance.

It involves transferring risk.

- Passive reinsurance.

It is about taking risks.

Active and passive reinsurance can be carried out simultaneously by the same insurance company. In this case it will act as:

- insurer;

- reinsurer;

- reinsurer.

In accordance with current legislation, vehicles are sources of increased danger. Accordingly, their owners must compensate for the damage caused to third parties.

To purchase an MTPL policy, you must enter into an appropriate agreement with the insurance company. It is the agreement concluded between the vehicle owner and the insurance company that is the basis for covering losses caused to third parties.

Of course, only those companies that have the appropriate permit (license) can act as insurers. You also need to know that the law establishes the main points that must be included in the insurance contract.

The object of insurance is the property interests of the owner of the vehicle, which are associated with his obligation to compensate for losses caused to third parties.

Our official partners:

ic_keyboard_arrow_left_24px ic_keyboard_arrow_right_24px

A striking example is compulsory motor liability insurance. At first, not everyone liked MTPL. But we gradually got used to it, because insurance has more than once saved drivers from having to compensate the damage to the injured party.

The cost of the policy depends on various parameters:

- Age and experience of the driver.

- Vehicle type and engine power.

- Accident-free driving.

- Insurance history.

- Territory of registration, etc.

Popular questions

Why is it profitable to issue a policy on elemins.ru?

- First of all, we are professionals in our field with really extensive experience in insurance and provide constant support to our clients in any situation:

- consultations in case of road accidents;

- assistance in resolving unusual situations with insurance companies;

- timely notification of the upcoming contract extension;

- Flexible system of discounts and special offers and promotions for our regular customers

- We select the best deals on the market, as we work directly with all the top and reliable insurance companies in the country.

- And finally, we keep up with the times and make communication with us as convenient and efficient as possible - all types of communication and even the ability to issue an electronic policy online directly on our website.

What discounts do you provide?

Our offers on the cost of insurance are always more profitable than in the branded offices of insurance companies, due to a significant discount from our commission, which we provide to all our clients. We have direct contracts with insurance companies, so we have a maximum commission amount. For regular customers, we have a flexible system of additional discounts, which makes the cost of their policies even more attractive.

How much does delivery cost?

At the moment, the cost of delivering the policy depends on the client’s location. We often deliver completely free of charge. Although the delivery of policies is now slowly but surely becoming an unnecessary atavism due to the fact that paper policies have been replaced by electronic ones and the registration process is moving online.

How can I place an order?

We tried to make communication with us as convenient as possible. You can place an order in any way.

- You can simply call us to order a policy by phone +74993224749 or on our mobile +79164648861, which is also connected to all kinds of instant messengers. (WhatsApp, Telegram, Viber).

- You can fill out and submit an application on any of the pages on our website. There are very simple forms where you just need to write your phone number or more detailed application forms where you can provide more details so that we can get up to speed as quickly as possible.

- Well, for the most advanced, we have the opportunity to issue an electronic MTPL policy online, by ourselves, without our help.

- We also accept applications and provide consultations via online chat on our website, as well as through social networks on our personal pages.

Do I need a diagnostic card for a new car?

A diagnostic card is not required for a new car. Passing the technical inspection procedure and receiving a diagnostic card upon completion is required for vehicles that have reached 3 years of age (counting starts from the year of production of the vehicle and the month of production is not taken into account). A diagnostic card is issued for a period of 2 years for vehicles aged from 3 years to 7 years inclusive, then a technical inspection must be completed every year.

What documents are required for registration of compulsory motor liability insurance?

To issue an MTPL policy, data from the following documents is required:

- Russian passport - main page with photo, place of issue and full name, as well as a page with registration;

- vehicle registration certificate (STS, also known as SRTS) or vehicle passport (PTS), if the vehicle is not yet registered with the traffic police or the owner will change;

- driver's licenses of persons authorized to drive a vehicle;

- a diagnostic card is required if 3 years have passed since the vehicle was manufactured

What is an electronic policy?

For several years now, everyone has only heard about electronic policies. What can I say? Already 90% of policyholders sign up for and use them. So, let's briefly explain what it is. Electronic policies have replaced paper ones. Modern technologies and almost complete coverage of the entire country by the Internet now allow the use of electronic document management, and, accordingly, allow the use of electronic documents in insurance. You don’t have to go to get electronic policies, you don’t have to wait for a courier - the policy is sent to your email instantly after payment, it’s easier to restore it if the file is lost, and finally, the production of paper policies is not environmentally friendly and uneconomical. An electronic policy, in our opinion, is superior to a paper policy in all respects.

What is KBM?

BMC is an abbreviation for Bonus Malus Ratio. To put it simply, this is the break-even coefficient, which is assigned to each driver, information about which is stored in the RSA database. The MSC can be either lowered or increased, depending on the presence or absence of accidents in which the driver is found to be the guilty party. The maximum is the lowest BMC - 0.5, which gives a 50% discount on the policy, and the minimum coefficient is equal to one. An increasing one is called a KBM that is higher than one and can reach a value of 2.45. You can view the KBM table, as well as check your KBM online, on our website page https://elemins.ru/kalkulyator/kbm

What to do if an insured event occurs under MTPL?

When an insured event occurs, you must:

- Make sure that no one is hurt, and if you are, call an ambulance and the police by calling the short number 112

- Do not remove the vehicle from the accident scene, and if it interferes with the movement of public transport, then first take video and photos of the accident site from different angles so that road markings, the position of the vehicles relative to each other and the road, as well as relative to the adjacent infrastructure are visible.

- Call the short number 112, inform the operator about the incident and call traffic police officers or other authorized services to the scene of the accident.

- If there are two participants in an accident and one of you admits his guilt, and the damage does not exceed 100,000 rubles (4,400,000 if the vehicle is equipped with DVRs and has a GLONASS system), then you do not need to call the traffic police officers, but use the EUROPROTOCOL.

- Obtain from traffic police officers or another authorized service a protocol or resolution on an administrative offense or a refusal to initiate a case. It is this document that is now the main one for the insurance company; a certificate of an accident is no longer issued.

- Call your insurance company and notify about the occurrence of an insured event. The insurance company operator will also advise on further actions.

What is EUROPROTOCOL?

EUROPROTOCOL is a procedure that allows participants to register an accident in a simplified form and without the presence of employees of the competent authorities. There are conditions for the possibility of applying the Europrotocol:

- There were two participants in the accident and no harm was caused to the life or health of the participants;

- One of the participants fully admits his guilt in the accident;

- The damage to the victim, according to the preliminary and subjective assessment of the participants, does not exceed 100,000 rubles (400,000 if the vehicle is equipped with DVRs and has a GLONASS system);

The European protocol is drawn up by filling out a special form - notification of an accident - by both participants in the accident.

Next, the injured party contacts their insurance company. It is important to note that both participants in the accident must notify their insurance company within 5 working days from the date of the insured event and, most importantly, not only the injured party, who plans to receive insurance compensation, but also the guilty party, who must contact their company and inform about the details of the insured event and send your copy of the accident notice. Otherwise, the insurance company, with one hundred percent probability, after settling the insured event, will present a claim for compensation for the culprit of the accident who failed to notify them. The amount of insurance compensation is 400 thousand rubles. (if only the car was damaged) and 500 thousand rubles. (if people were injured).

The procedure for making insurance compensation and monitoring its compliance

From the first of July 2014, the payment limit for compulsory motor liability insurance concluded after October 1, 2014 is four hundred thousand rubles in case of compensation for damage to a car. Previously, the maximum payment amount was one hundred twenty thousand rubles. It is also planned in 2015, no earlier than April, to increase the amount of payments for compensation for health and life.

To receive compensation, the victim can contact not only the insurer of the person responsible for the accident, but also directly to his insurance company if all participants in the accident have a compulsory motor liability insurance policy.

If you purchased another policy

Compulsory motor liability insurance is mandatory and, based on the law, the driver is required to purchase a compulsory insurance policy. Since CASCO is voluntary, the question of purchasing it is at the discretion of the driver.

CASCO is a more expensive insurance, and has more possibilities for insurance cases, but CASCO is voluntary insurance and is taken out at the discretion of the driver.

Insurance of property of citizens is very diverse and can concern relatively independent types of insurance. The objects of property insurance are:

- means of transport (personal transport). The most common type of property insurance for citizens is insurance of vehicles - against theft, damage, intentional actions of third parties, etc.;

- residential premises (including apartments and individual rooms within the city) and their component structures (various types of floors, dividing partitions, etc.), as well as finishing elements that can be repaired and improved (wall, ceiling, floor coverings) , individual elements and equipment of heating (autonomous) and sewerage (toilets, sinks, baths), - insurance against damage, destruction: due to flooding with water, as well as the actions of third parties;

- three buildings (residential houses, cottages, cottages, outbuildings, bathhouses) and their component structures (roofing, floors, foundations) - insurance of household property: against fire, landslides, groundwater, earthquakes, soil subsidence, water penetration from rainfall, hail, etc.;

- other household property (household items, documents and securities, precious and semi-precious metals and a fireplace) - insurance against fire (fire insurance), water penetration, theft, damage, etc. It should be said that such insurance objects can be insured for special conditions - in the form of an addition to the main agreement;

- pets – animal life insurance, theft, loss, etc.

Among the many types of property insurance for citizens, the following property insurance objects are distinguished:

- the object is a variety of material values;

- personal insurance, where the objects of insurance are events in the lives of individuals;

- liability insurance, the subject of which is compensation for the insured's obligation to compensate for damage (harm) to third parties.

As mentioned above, property insurance can be:

- voluntary, the procedure is determined on the basis of the agreement of the parties (the policyholder and the insurance organization) regarding the terms of insurance;

- mandatory when such insurance is required by law.

Special types of property insurance are reinsurance and coinsurance. These types of insurance allow you to distribute and redistribute large risks between different insurance companies.

In addition to the common types of property insurance, there are others, namely:

- insurance against non-receipt of expected income from various transactions and turnover;

- insurance of banking risks from the purchase of currency, issuance (non-repayment) of loans, etc.;

- commercial risk insurance (may include the two previous types of property insurance);

- insurance of construction risks (simple construction against shortages of building materials, facing materials by partners of the construction company).

In any type of property insurance, the insurance contract stipulates the amount and procedure for payment of insurance compensation; all this must be reflected in the property insurance policy.

Insurance is a necessary necessity. Now you know what applies to property insurance, and “in which direction” you need to move in order, if not to protect yourself completely, then at least to minimize material losses from unforeseen events that can happen to any of us.

What does MTPL provide in case of an accident?

OSAGO is the main auto insurance document used in Russia. Its presence is a prerequisite for going on the road (and this applies to any car and special transport, as well as motorcycles). It provides car owners with the opportunity to compensate for damage caused (or received) to someone after a traffic accident.

Previously (before compulsory car insurance was introduced), a driver, having had an accident and found himself at fault (and not having voluntary insurance), was obliged to pay all the damage to the victim at his own expense, and these amounts could sometimes be very large . Currently, a compulsory car insurance policy protects motorists from such situations - the required amount is now paid not by the culprit himself, but by the insurance company with which he entered into an agreement.

Information : compensation for damage occurs not only in case of a traffic accident involving cars, but also in case of damage to pedestrians or real estate (for example, road fences, signs, poles, and so on).

What is the difference between voluntary and compulsory property insurance?

Voluntary property insurance is nothing more than the need of individuals and legal entities to protect their property interests, if they (needs) do not run counter to the law and are confirmed by the client’s finances (his ability to pay for certain types of insurance) and his desire to pay ( precisely a desire, not an obligation).

Voluntary insurance is a kind of commodity-money relationship, which in principle it is. Everything is fair here, because no one forces you into this relationship - the demand of the buyer (the policyholder) and the offer of the seller (insurance organization), only the terms of insurance are negotiated. Everything is very clear - if they do not suit you (some conditions), you simply look for another insurer. No one owes nothing to nobody.

Compulsory insurance of property of individuals and legal entities is based on legislation that does not take into account the financial condition of those individuals who may suffer or suffer losses from insurance events that may occur as a result of the actions (inaction) of civil and legal entities.

At the same time, the state cannot fail to take into account the solvency of civil and legal entities when developing laws on compulsory insurance, so that later problems do not arise in matters of the size of insurance premiums and tariffs. Financing of compulsory property insurance comes from two sources:

- own funds and funds of interested parties - sponsors, shareholders, shareholders, etc. Such insurance is subject to the property of enterprises invested by foreigners, temporarily exported cultural property, geological installations and structures, property pledged in a pawnshop, etc.;

- funds from the relevant budgets - property of enterprises, property of individuals (from a man-made disaster or natural disaster, accidents), property of judges, contract military personnel, tax police, etc.

MTPL reform 2014

Summing up, I would like to note that after the reforms of 2014, the MTPL policy became more expensive, but at the same time the amount of payments on it was increased. Also, the government decree changed the procedure for registering road accidents using video recorders to receive compensation, which applies to some regions of Russia for those who issued compulsory motor liability insurance after October 1, 2014.

According to the new Amendments, the requirements for policyholders have been tightened. The period for payment of compensation from September should not exceed twenty days, otherwise the company will be forced to pay a penalty. A penalty has been introduced for failure to indicate the reasons for refusal to pay compensation.

What is OSAGO?

OSAGO is compulsory motor third party liability insurance, which is the most common motor insurance in Russia. According to current legislation, any type of civil liability involves compensation for damage caused to the injured party. This rule also applies to motor vehicle liability, according to which each driver undertakes to compensate for any possible harm on the road.

For example, if a car owner crashes into another car, he covers vehicle repairs, or if he hits a pedestrian, he pays for the treatment of the victim. The Law “On Compulsory Motor Liability Insurance” was developed to ensure that the injured party was guaranteed to receive compensation for the damage caused, which was previously quite problematic: each of the participants in the accident had his own opinion about who was right and who was wrong, and what amount of compensation to demand from the culprit of the road accident. incidents.

Consequently, in order to avoid the creation of additional conflict situations as a result of an accident and to cover the damage caused, the MTPL insurance policy was legalized. After the approval of this law, compensation for damage that occurs on the road is assumed by the insurer.